METRICS / NUMBERING

MANAGING

BETTER METRICS ARE FUNDAMENTAL TO SUCCESS ... YOU MANAGE WHAT YOU MEASURE

CHANGING THE WAY THE GAME IS SCORED WILL CHANGE THE WAY THE GAME IS PLAYED

ESSENTIAL TO MEASURE WHAT REALLY MATTERS

|

|

|

|

Measure Change in State and you Measure Progress

|

|

|

|

|

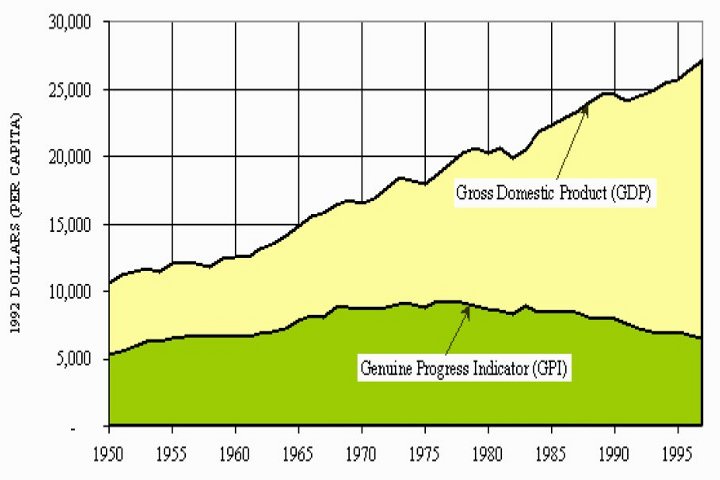

Most financial metrics show growth and are therefore considered better

|

Stock market

|

Intangible value

|

Money supply

|

World GDP growth

|

US GDP growth

|

GDP v GPI

|

|

... while metrics for social and environmental impacts trending dangerously worse

|

Value of $ down

|

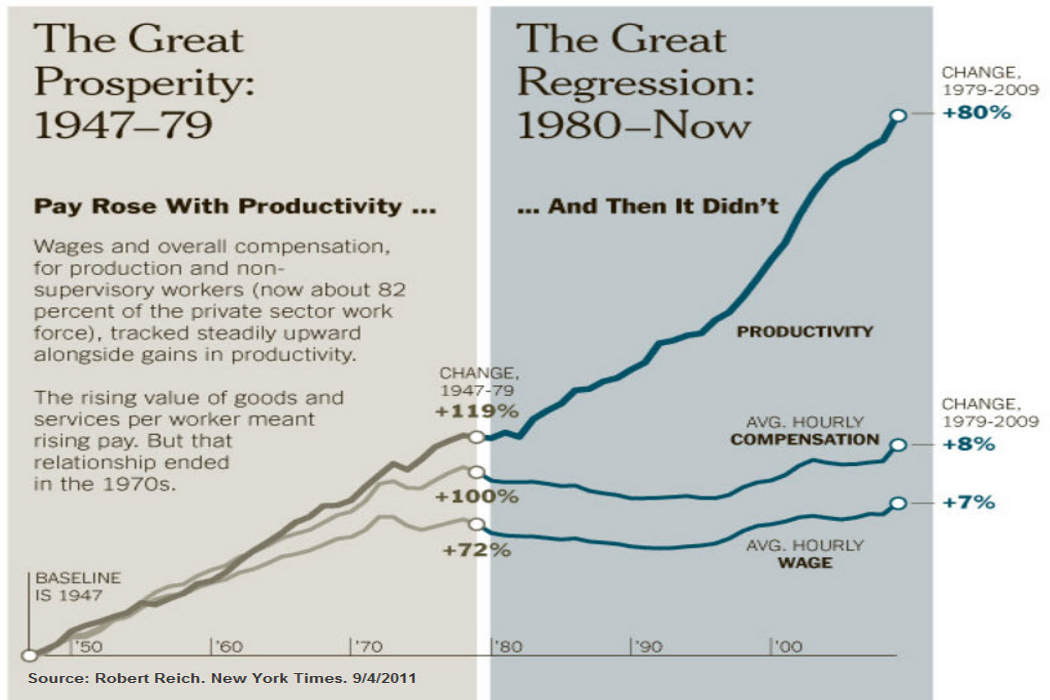

Wages flat

|

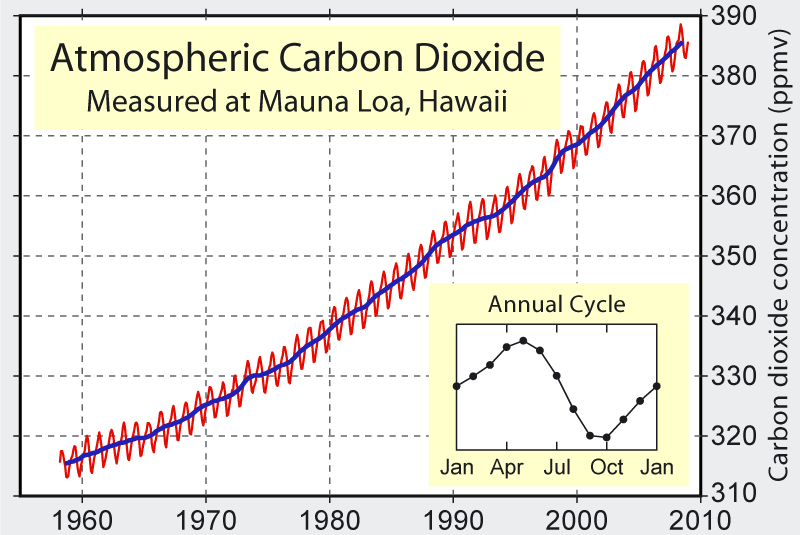

CO2 concentration

CO2 concentration

|

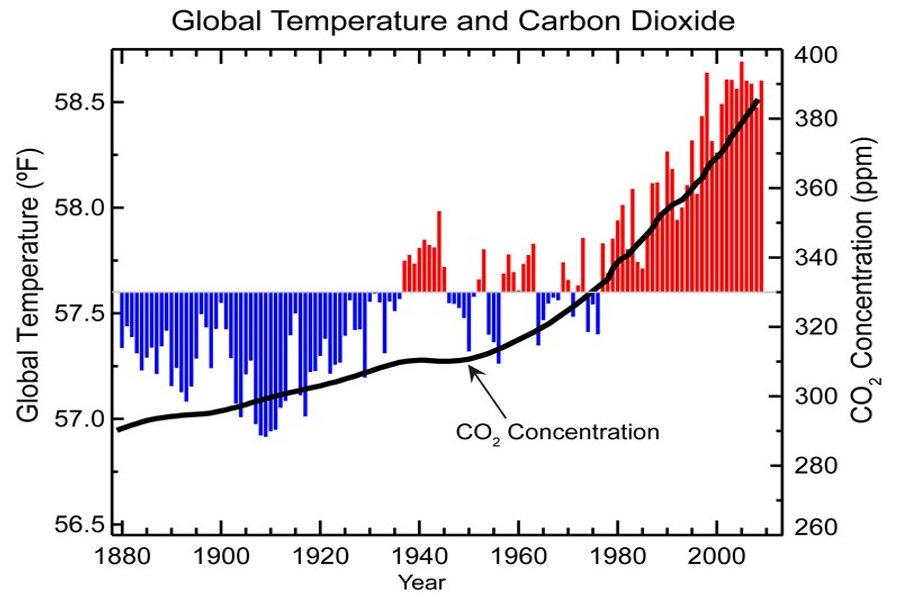

Temp v CO2

|

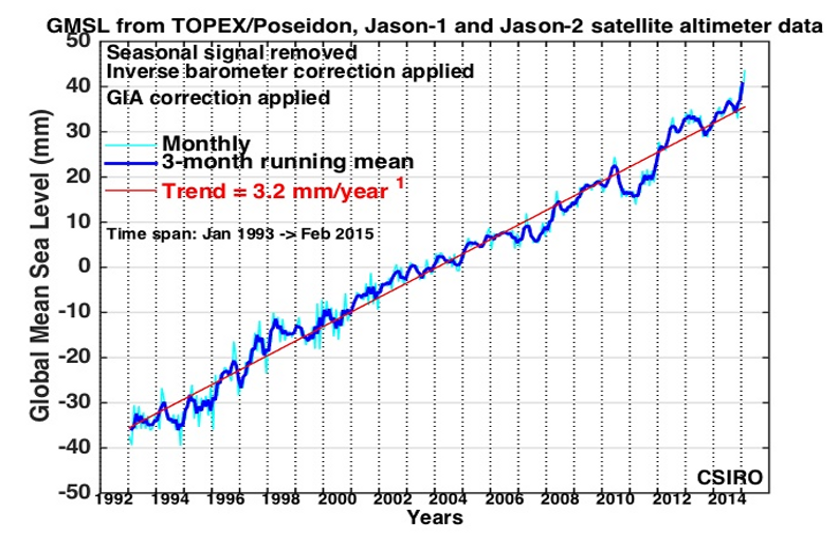

Sea level rise

|

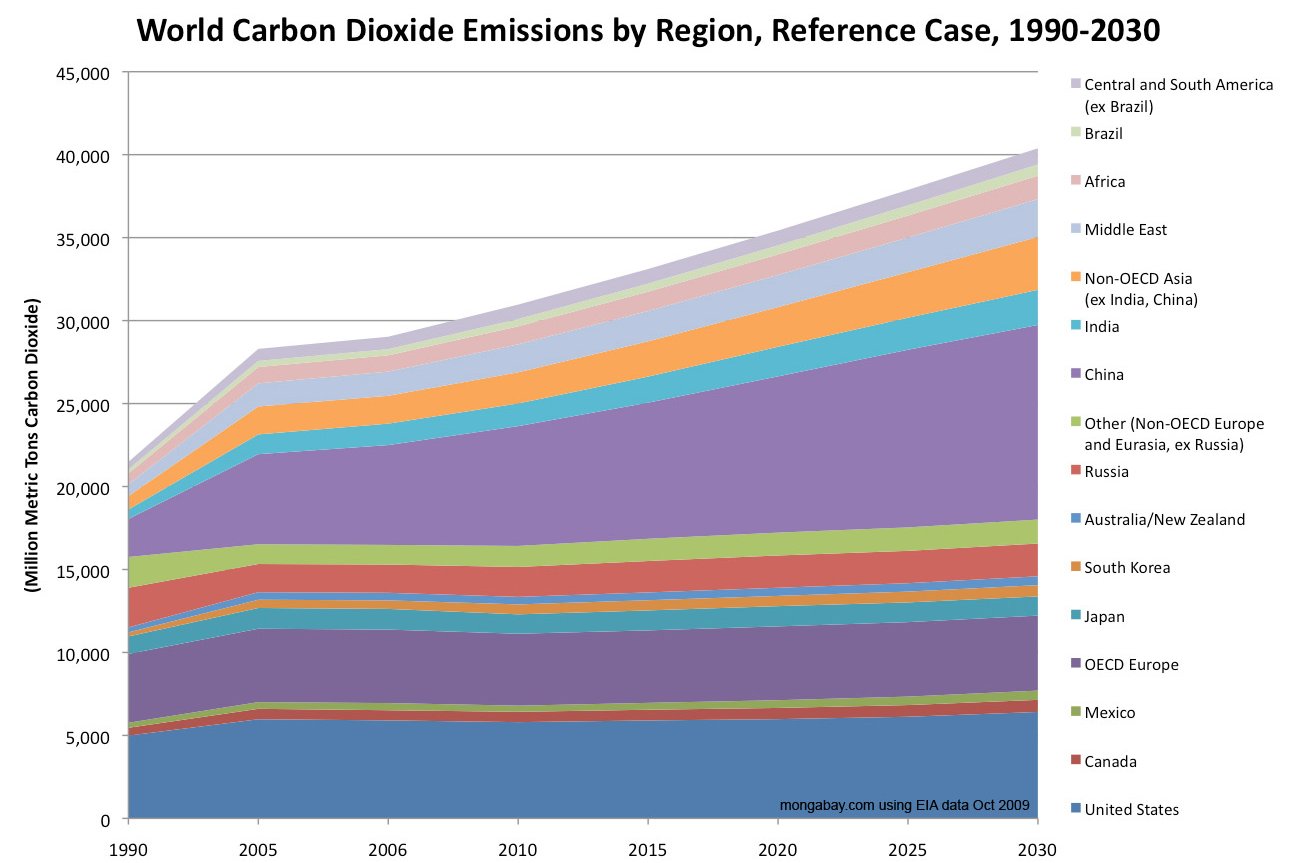

CO2 emissions

|

|

|

THE MODERN WORLD IS UNSUSTAINABLE

THERE IS AN UNGENT NEED FOR RAPID, SIGNIFICANT CHANGE TO AVOID AN EXISTENTIAL CRISIS

|

|

|

|

MEASURE WHAT MATTERS

MODERN METRICS ARE DANGEROUSLY DYSFUNCTIONAL

|

GO TOP

|

|

Peter Drucker famously said 'You cannot manage what you don't measure'

This is undounbtedly true ... in the corporate world, the components that go into making profit are measured intensely in order to improve profit performance ... and it works!

Unfortunately, we don't do anything like the same amount of measuring in order to improve society and avoid degrading the environment ... and we don't have any easy way of talking about social performance and environmental performance in the same way that we are able to talk about corporate performance and investment portfolio performance. This has to change

|

|

CONVENTIONAL FINANCIAL ACCOUNTING

CONVENTIONAL CORPORATE MANAGEMENT METRICS

|

GO TOP

|

CONVENTIONAL CORPORATE MANAGEMENT METRICS

It is widely accepted that you manage what you measure. The modern world has impressive data about corporate profit performance and the growth of financial wealth. These metrics dominate the conversation in the media, and important decisions being made in politics and business.

The measures for social performance and environmental performance are intellectually and methodologically weak compared to the data systems deployed for accounting for, managing and reporting profit.

The dysfunction of modern metrics is one of the key reasons why so much in the modern world is wrong ... but by no means the only thing that is wrong!

|

CONVENTIONAL FINANCIAL ACCOUNTING AND RELATED MANAGEMENT SYSTEMS ARE VERY POWERFUL ... BUT ONLY ABOUT PROFIT PERFORMANCE AND FINANCIAL CAPITAL ... THEY COMPLETELY IGNORE EXTERNALITIES AND SO MUCH ELSE THAT IS IMPORTANT

Corporate financial management and management information enables rapid decision making about everythiong associated with corporate profit performance.

There is nothing like it for the impact on society and the impact on the environment ... the externalities are ignored.

The concepts of double entry accounting are ancient, but they are the key to the effectiveness of accountancy as an analytical tool.

|

|

... this is what True Value Impact Accounting (TVIA) is all about ... When numbers about progress and performance are missing, then there is no conversation that is grounded in reality and it becomes easy to promulgate 'fake news' and the appearance of good performance without much reality.

|

|

|

TRUE VALUE IMPACT ACCOUNTING

ACCOUNTABILITY FOR EVERYTHING USING DOUBLE ENTRY ACCOUNTING FOR EVERYTHING

|

GO TOP

|

|

Navigation to everything about True Value Impact Accounting (TVIA)

|

Open L070-TVIA

|

Conventional financial accounting uses money as its unit of account, and concerns itself mainly with money revenues, costs and profits without taking into account the 'externalities' which impact society, natural resources and the environment.

The True Value Impact Accounting (TVIA) initiative builds on the powerful well-established double entry accounting construct to account for everything, giving accountability for ALL of CAPITAL (i.e. HUMAN CAPITAL, NATURAL CAPITAL and CREATED PHSYICAL AND INTANGIBLE CAPITALS) and not just FINANCIAL CAPITAL.

TVIA uses multiple UNITS OF ACCOUNT rather than only money and STANDARD VALUE PROFILES for the PRODUCTS that flow through the system

TVIA has a comprehensive architecture that enables coherent progress and performance reporting for ORGANIZATIONS, PEOPLE (Individuals and families), PLACES, PROCESSES, PRODUCTS and STREAMS.

The purpose of TVIA is to enable better decision making to build better societies and a sustainable world. An important part of the initiative is to facilitate better timely decisions by individual people.

|

THE CASE FOR BETTER WAYS OF NUMBERING

from PAGE 18 of Sustainable-Food-Trust-The-Cost-of-American-Food-Report-2016

We are currently paying three times for the food we eat. Firstly, in agricultural subsidy payments which largely promote intensive crop production. Secondly, we pay for the food at its retail value when we buy it in the shop. Finally, we pay for a third time to cover the costs of healthcare, as well as the costs of measures to tackle poverty and environmental degradation.

A case in point is the $250 million in subsidies paid annually to maize producers that results in producing cheap high fructose corn syrup for a booming soft drink industry. This leads to increasing incidence of obesity and diabetes, the costs of which are paid for by society.

Another example is the cost of the restaurant system that denies a living wage and benefits to workers, resulting in billions of dollars worth of tips by consumers, and an additional $16.5 billion annually in public subsidies for food stamps and medication. Increasing the federal minimum worker wage to $12 per hour would be equivalent to an average household increase in daily food cost of just 10 cents a day.

Responsible investment strategies are growing in the US but investors are dissatisfied with current environmental, social and governance disclosures. Profit-and-loss accounts must include societal costs in order to enhance market efficiency and manage risks related to resource scarcity, climate change or eventual regulations on product or consumer safety. True cost accounting brings all environmental, social and economic strands into a uniform strategic approach, allowing decisions that safeguard soils, plants, animals and people, while simultaneously producing positive business results.

|

Open PDF

http://www.truevaluemetrics.org/DBpdfs/Food/SustainableFood/Sustainable-Food-Trust-The-Cost-of-American-Food-Report-2016.pdf

|

Open PDF ...

Sustainable-Food-Trust-The-Cost-of-American-Food-Report-2016

|

|

|

|

|

|

REPORTING ENTITIES

REPORTING FOR ORGANIZATIONS, PEOPLE, PLACES, PROCESSES, PRODUCTS, STREAMS

Also PROJECTS, PROGRAMS and POLICIES

In conventional accounting there are established rules for reporting for the reporting entity. For example, all corporate business organizations report financial performance including the transactions that relate to the organization but excluding transactions that are outsie the 'reporting envelope'. Rules have been established to handle complex corporate structures involving subsidiaries that are both wholly owned, and those with outside stockholders. In TVIA these ideas are expanded to enable coherent reporting not only for the business organization but for all the various entities that make up the complete socio-enviro-economic system.

|

Open L070-RE-REPORTING-ENTITIES

|

ORGANIZATIONS

PURPOSE SHOULD BE MORE THAN JUST MAXIMIZING PROFIT

|

Open L0700-RE-ORGANIZATIONS

|

PEOPLE

THE MAIN PURPOSE OF EVERYTHING IS TO IMPROVE QUALITY OF LIFE FOR PEOPLE

|

Open L0700-RE-PEOPLE

|

PLACES

WHERE EVERYTHING COMES TOGETHER ... THE PEOPLE LIVE. ORGANIZATIONS PRODUCE AND POLLUTE

|

Open L0700-RE-PLACES

|

PROCESSES

WHERE AMAZING TECHNOLOGY SHOULD BE APPLIED FOR COMPREHENSIVE EFFICIENCY

|

Open L0700-RE-PROCESSES

|

PRODUCTS

PRODUCTS FLOW THROUGH THE SYSTEM, AND THROUGH USE DELIVER VALUE TO PEOPLE AND SOCIETY

|

Open L0700-RE-PRODUCTS

|

STRANDS

EVERYTHING HAS AN IMPACT ON EVERYTHING ELSE

|

|

PORTFOLIOS

Investor decisions are critical for better business ESG performance

|

Open L0700-RE-PORTFOLIOS

|

PROJECTS

Appropriate for activities that are time limited

|

|

PROGRAMS

Needed for program accountability

|

Open L0700-RE-PROGRAMS

|

POLICY

Needed for accountability with respect to policy

|

Open L0700-RE-POLICY

|

|

|

|

UNITS OF ACCOUNT

MORE POWERFUL THAN MONETIZING IMPACT

Conventional financial accounting uses money as its unit of account, and there are established methods for the use of multiple currencies when this is needed because of the nature of the business.

With TVIA, multiple UNITS OF ACCOUNT are used in a similar way to account for the way in which different activities impact ALL the CAPITALS that make up the SOCIO-ENVIRO-ECONOMIC SYSTEM. This is more powerful and more flexible than the idea of valuing everything using money and markets

|

Open L070-UA-UNITS-OF-ACCOUNT

|

MONEY

Long history as the foundation for ALL economic measurement ... but in need of complementary metrics to address all issues

|

Open L0700-UA-MONEY

|

A UNIT OF ACCOUNT FOR LIFE AND QUALITY OF LIFE

LIFE and QUALITY OF LIFE are the most important measure of PROGRESS and PERFORMANCE

|

Open L0700-UA-HUMAN-CAPITAL

|

A UNIT OF ACCOUNT FOR NATURAL CAPITAL - LAND

LAND IS LIMITED and there are many alternative uses that are required in a sustainable system.

|

Open L0700-UA-LAND

|

A UNIT OF ACCOUNT FOR NATURAL CAPITAL - WATER

WATER is vital for human life as well as for production in both people built systems and in natural systems

|

Open L0700-UA-WATER

|

A UNIT OF ACCOUNT FOR NATURAL CAPITAL - AIR

Degradation of CLEAN AIR has consequences including deterioration of human health

|

Open L0700-UA-AIR

|

A UNIT OF ACCOUNT FOR NATURAL CAPITAL - CLIMATE / GHG

Changes in the ATMOSPHERE as a result of Green-House-Gas (GHG) emissions are changing climate behavior with huge existential implications.

|

Open L0700-UA-CLIMATE-GHG

|

A UNIT OF ACCOUNT FOR NATURAL CAPITAL - BIODIVERSITY

Changes in the ATMOSPHERE as a result of Green-House-Gas (GHG) emissions are changing climate behavior with huge existential implications.

|

Open L0700-UA-BIODIVERSITY

|

A UNIT OF ACCOUNT FOR NATURAL CAPITAL - ECO-SYSTEM SERVICES

Changes in the ATMOSPHERE as a result of Green-House-Gas (GHG) emissions are changing climate behavior with huge existential implications.

|

Open L0700-UA-ECOSYSTEM-SERVICES

|

A UNIT OF ACCOUNT FOR NATURAL CAPITAL - NATURAL RESOURCE DEPLETION

Changes in the ATMOSPHERE as a result of Green-House-Gas (GHG) emissions are changing climate behavior with huge existential implications.

|

Open L0700-UA-NATURAL-RESOURCE-DEPLETION

|

|

|

|

STANDARD VALUE PROFILES

AN OPEN ACCESS DATABASE FOR STANDARD VALUE PROFILES FOR EVERYTHING

|

Open L070-SV-STANDARD-VALUE-PROFILES

|

STANDARD VALUE PROFILE DATABASE

CRITICAL DATA ABOUT THE TRUE COSTS AND VALUE OF EVERY PRODUCT ON THE PLANET

Well managed companies know a lot about every product that is flowing into their organizations and being produced for sale. There is nothing like this level of knowedgle about the products that are flowing through society and having impact on people and the environment.

In companies one technique for documenting knowledge about products is the idea of Standard Costs which is powerful and relatively low cost. In the TVIA data architecture, the equivalent are STANDARD VALUE PROFILES.

|

|

|

METRICS

WITHOUT MEASURES, THERE IS NO MANAGEMENT / MEASURES FOR EVERYTHING ... NOT MERELY MONEY

How we talk about progress and performance ... or not? When numbers about state, progress and performance are missing, then there is no conversation that is grounded in reality and it becomes easy to promulgate 'fake news' and the appearance of good performance without much reality.

|

|

|

TRUE VALUE IMPACT ACCOUNTING (TVIA)

ABOUT TRUE VALUE IMPACT ACCOUNTING ... STATE, PROGRESS AND PERFORMANCE FOR EVERYTHING

|

GO TOP

|

|

|

INITIATIVES DEVELOPING METRICS

SEVERAL HUNDRED ORGANIZATIONS INVOLDED IN DEVELOPING / APPLYING METRICS

|

GO TOP

|

|

|

THE MONEY METRIC

How we talk about progress and performance ... or not. When numbers about progress and performance are missing, then there is no conversation that is grounded in reality and it becomes easy to promulgate 'fake news' and the appearance of good performance without much reality.

|

GO TOP

|

|

What is money?

When money serves as both a medium of exchange and a store of value it cannot also serve as a measure of the value and have much measurement meaning.

Money is efficient as a medium of exchange.

Money also works as a store of value as long as the idea of money is trusted to have value. The importance of this trust cannot be overstated.

In order to measure the value of intangibles of all sorts, the solution is to use UNIT OF ACCOUNT specific to the characteristic of the intangible element and what it does.

|

|

|

|

SPECIALIZED SYSTEMS FOR ACCOUNTING AND REPORTING

Examples of many different types of accounting and reporting

|

GO TOP

|

|

|

WORLD BANK / UNITED NATIONS / OECD METRICS

A huge amount of data at the country level ... rather little below this level

|

GO TOP

|

OVERVIEW

EARLY HISTORY OF THINKING ABOUT BETTER METRICS

A recognition that conventoinal money based financial accounting could not do accountability for a complex system

|

|

|

OVERVIEW / HISTORY

|

|

|

|

OVERVIEW HISTORY

OVERVIEW-HISTORY-0

|

Open L070-OVERVIEW-HISTORY-0

|

|

|

STOCK MARKET METRICS

The business media reports on movements in stock markets every 15 minutes ... there is nothing remotely like it for the performance of people, society or the environment

|

GO TOP

|

|

New York Stock Exchange (NYSE)

|

|

Dow from 1998 to 2016

An impressive increase in the index ... but what does it really mean?

In large part the profits of business increased while the wealth of society as a whole was diminishing.

This is the behavior that one must expect when the only management measure that is used everywhere is money profit performance for organizations, and money income and financial wealth for individuals.

|

|

Open exernal link

|

|

Dow from 1927 to 2017 adjusted for consumer prices (CPI)

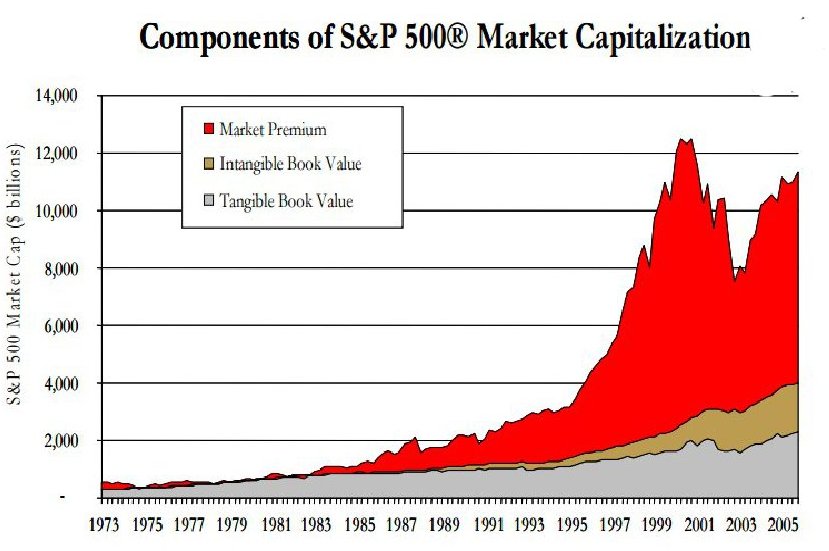

The Dow index has increased by an impressive amount over the long term ... but it hardly represents any significant reality. There are only a very few large cap stocks and these are changed from time to time in a way that eliminates the failing companies. The S&P 500 is a singificantly more represeantative index.

The Dow ... We’re Already at Dow 30000, You Just Don’t Know It

The blue-chip index is a poor measure of what investors are doing

By JAMES MACKINTOSH Updated Jan. 25, 2017 2:06 p.m. ET

It’s time to ditch the Dow. After 120 years, the venerable Dow Jones Industrial Average is an embarrassing anachronism, abandoned by professionals and beloved only by a media ...

'https://www.wsj.com/articles/were-already-at-dow-30000-you-just-dont-know-it-1485362316'

|

|

Open exernal link

|

|

|

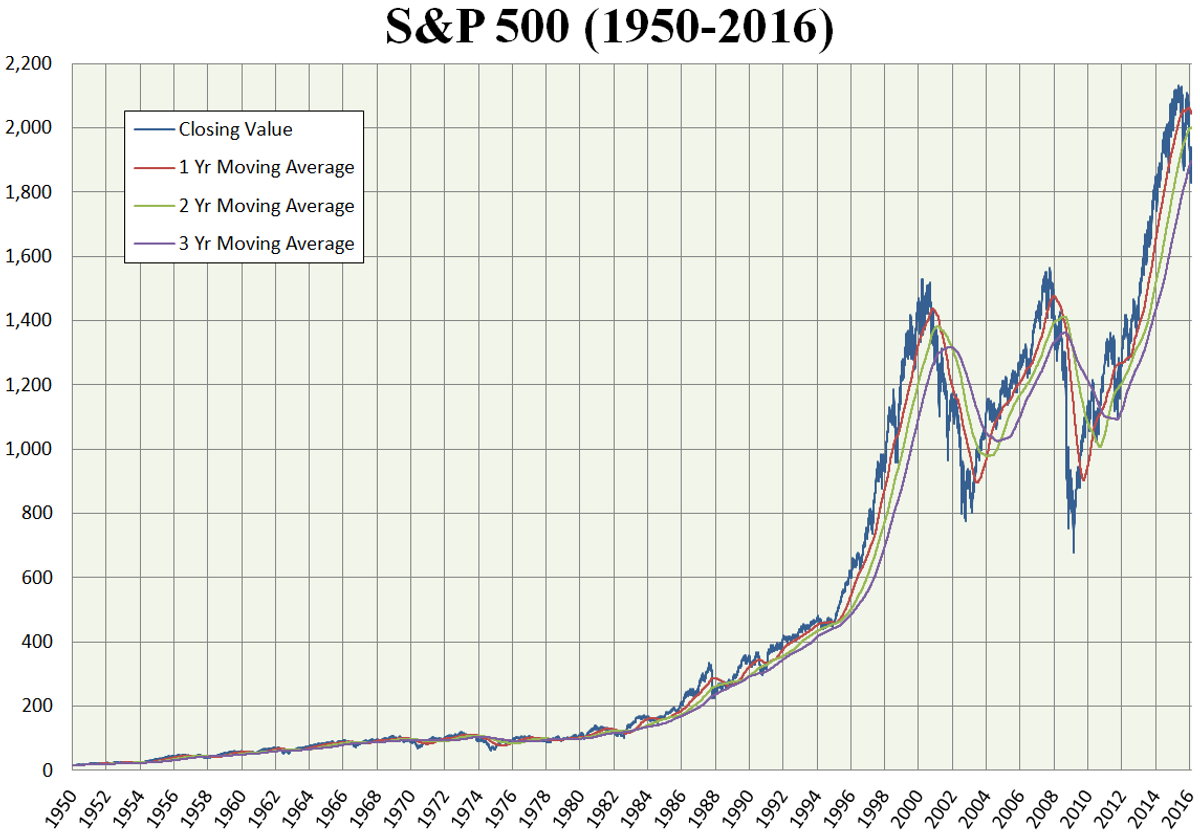

The S&P Index from 1956 to 2017

|

|

|

|

|

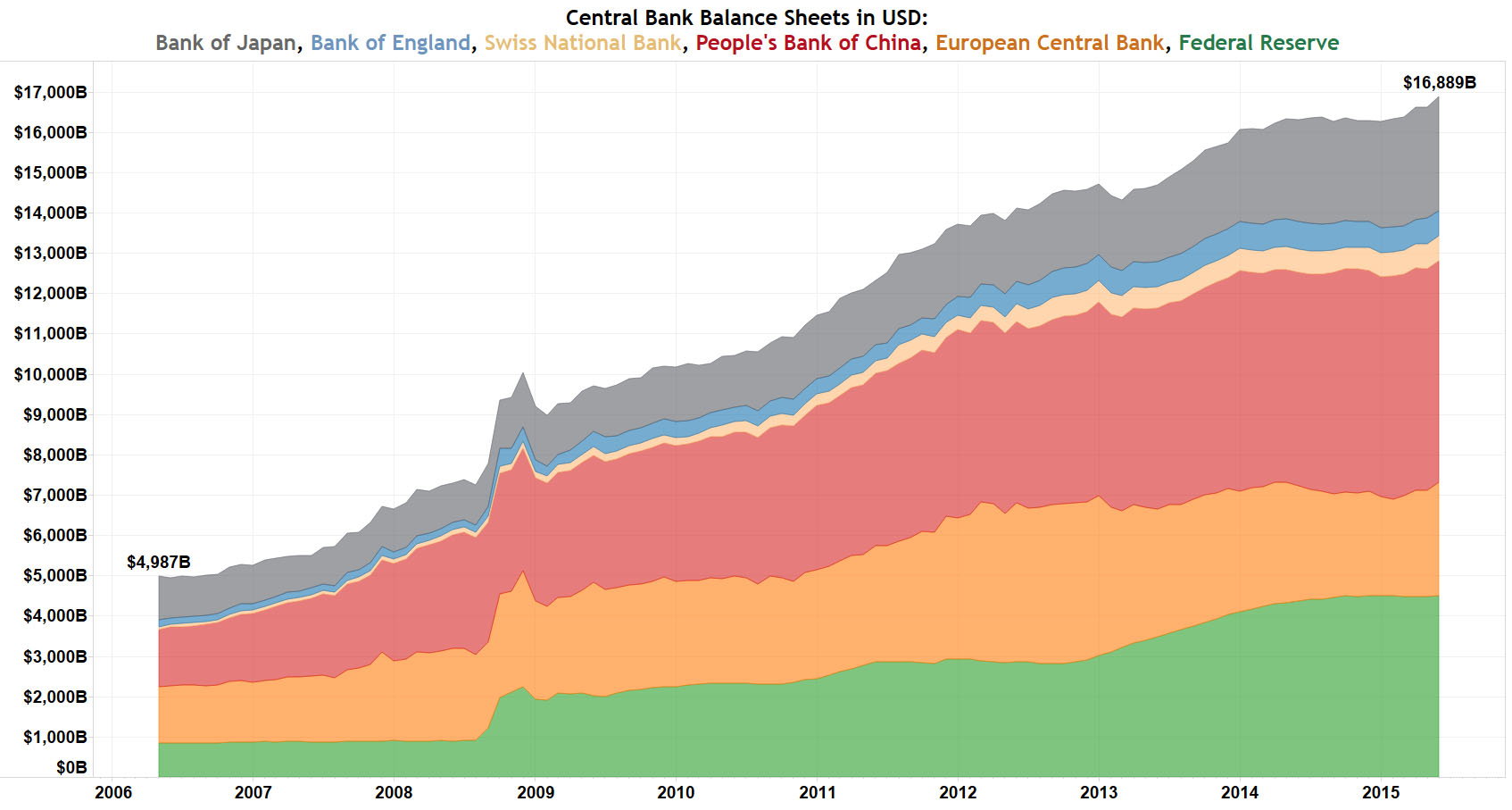

THE FINANCING OF THE BANKING SECTOR

The financing of the banking sector is underwritten by the unusual arrangements that are Central Banks

|

GO TOP

|

|

Central Bank asset growth from 2006 to 2016

'http://inflation.us/central-bank-balance-sheet-assets-hit-record-high/'

|

|

Open exernal link

|

|

|

THE FINANCING OF INTERNATIONAL DEVELOPMENT ASSISTANCE

The financing of international development assistance has been both rather modest and also quite ineffective. More and better are both needed.

|

GO TOP

|

|

Segmentation of FDI fund flows

The financing of international development assistance has been both rather modest and also quite ineffective. More and better are both needed.

Remittances are one of the most important area of growth and likely one of the most efficient in terms of delivering poverty reduction at a low cost. It can also be noted that the banking sector and financial services industry charges very high prices for a service that is vital but low cost for the banks!

|

|

|

|

|

BANK LENDING BY SECTOR

Bank lending by sector is more about credit worthyness than impactfulness

|

GO TOP

|

|

|

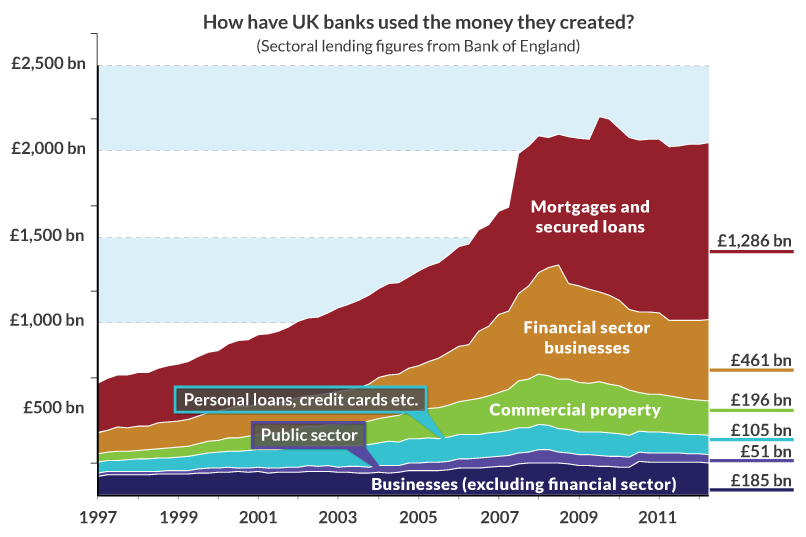

UK Bank Lending by Sector

|

|

|

|

|

UNITED NATIONS and MANAGEMENT METRICS

The United Nations does a lot of 'big picture' metrics ... but much less about management metrics suited to making better decisions

|

GO TOP

|

|

SDGs - SUSTAINABLE DEVELOPMENT GOALS

|

|

SDGs - SUSTAINABLE DEVELOPMENT GOALS

The 17 Sustainable Development Goals were launched by the United Nations in 2015 together with more than 120 indicators of progress as a replacement fore the NDGs. An important criticism of the SDGs is that they represent discontinuity from the MDGS to the SDGs and too much of an opportunity to lose much of the momentum that was in place for the MDGs. For more on this, see the link ... |

| Open L0M00-SDGs

|

|

MDGs - MILLENNIUM DEVELOPMENT GOALS

|

|

|

|