TRUEVALUEMETRICS - CORE CONCEPTS

COST, PRICE and VALUE

|

|

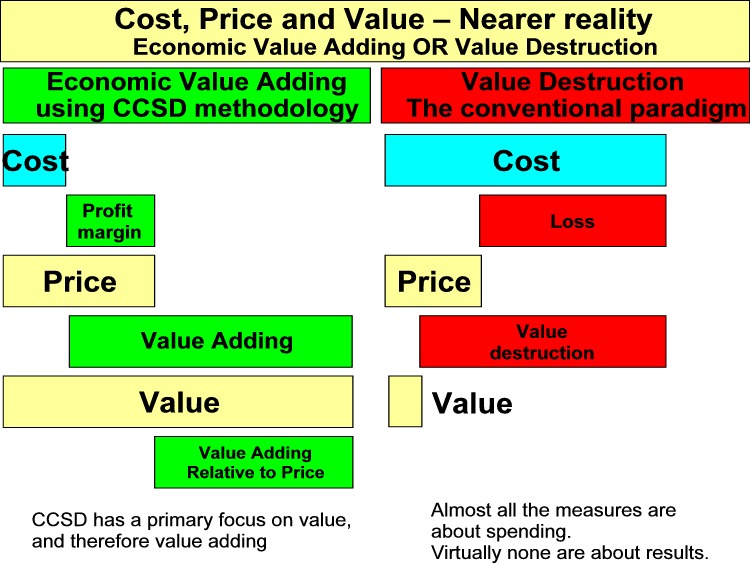

Cost Price and Value

|

|

A thorough understanding of cost, price and value makes the analysis of economic performance much more useful.

Most managers in business understand cost and price because this results in understanding profit ... but few managers have anything like the same understanding of cost and value.

|

More text about the graphic

|

|

Value Destroying Projects

|

|

|

More text about the graphic

|

|

Value Add versus Value Destruction

|

A thorough understanding of cost, price and value makes the analysis of economic performance much more useful.

Most managers in business understand cost and price because this results in understanding profit ... but few managers have anything like the same understanding of cost and value.

This problem is even more serious in the public sector and especially in the international relief and development sector which lack even the discipline of profit performance.

Journalists and the general public in conversation ofter use price and cost interchangably, showing a serious lack of understanding of the economics in all aspects of life.

An example of this is the idea that the cost of the healthcare in the USA is high. While there are examples of very high cost procedures, many medical procedures are very efficient and low cost. In general in the USA, the price of everything in the health sector is very very high. Of course, the difference between price and cost is profit ... and in the USA profits in the health sector are high. There is also the obscene reality in the USA health sector, that price is determined as much as anything by the ability of someone to pay and the high value associated with keeping a loved one alive!. Pricing is not much related to the cost and a reasonable profit, but optimized for maximum profit. All of this is enabled by the complexity of the arrangements within the system and a lack of transparency.

|

|

Cost, Price and Value ... three key numbers

|

Cost, price and value are very key numbers about any economic activity. Though modern society is founded on economic activity, and though there are massive datasets about prices. ... that is what a buyer pays for a product or services, and what prices stocks and other financial interests are trading at, what prices commodities are trading at, etc. etc. there is a surprising lack of information about cost and value.

The explanation why there is little information about costs may well be that those that make decisions would be embarrassed at the internal value chain within their organizations.

Corporate accountancy is only about money cost and money price. TrueValueMetrics (TVM) uses cost, price and value. The value derivatives of cost, price and value are key numbers that describe economic activity. The relationship between these numbers determines the performance of almost any economic activity. All of these measures are important ... any one missing and the understanding of the dynamic of societal progress is compromised.

|

What is the cost?

Performance is both efficiency and effectiveness. The profit and loss account summarizes the activities of the organization in money terms showing the revenues and the expenditures. The profit and loss account that is presented to outsiders tends to show the least amount of information allowed by law, while the internal profit and loss accounts will show all the information needed to facilitate good management.

|

Cost and value

Cost and value make it possible to calculate value adding ... something that is very important for society. For this to be of greatest use, the calculation of cost must include not only the money cost but also the value consumed associated with the activity.

What is this? In the case of the oil industry, the costs of crude oil production include payments made for royalties, licenses, etc, as well as the costs of exploration, drilling and extracting the oil from the oilfield, and shipping the product to refineries and to market ... but the costs do not take into account in any financial metric the depletion of the resource, and what it would take to replace this resource. This is a huge problem, because the resource being depleted has taken many millions of years to accumulate, and the cost of this

There are other examples ... see ????

|

Price and value

In some cases price and value are the same. In this situation the value chain through delivery to the final consumer is extracting from the consumer a price that is equivalent to the value. The consumer does not get anything of the added value. In fact the typical business model is one that aims to extract as much revenue from the market as possible.

The use of resources does not automatically mean that there is either going to be efficient or effective use of resources.

|

Cost efficiency … how much actual was relative to standard

Cost efficiency is how much the actual cost was relative to what the cost should have been … often expressed as a standard cost. There are many ways to evaluate cost performance including also comparison with activities undertaken in other places or with activities undertaken by other organizations.

Well designed data systems makes it possible to compare how much something actually cost with what it should have cost.

Cost efficiency is a measure of how well something is done. Cost efficiency answers the question about whether or not resources used are more or less than would normally be expected? Comparative cost efficiency answers the question about cost relative to other similar works at another time or in another place.

|

Cost effectiveness … How much value for the cost?

Well designed data also makes it possible to measure the relationship between the cost and the impact … that is the change in value arising for the community. Cost effectiveness is a measure of how well doing something results in getting the desired impact. Did the use of resources solve the problem that is being addressed or not. Did the use of resources have a favorable impact on the community and quality of life … and was the impact what should have been achieved.

Cost effectiveness is the more complex idea of relating cost to the value of the accomplishment. The idea is simple in theory, but becomes more difficult as the problems being addressed are more complex. TVM uses techniques to get an overall idea of cost effectiveness, and then goes into more detail to assess the way different initiatives contribute to progress. This may require multi-variate analysis of the datasets where there are multiple interventions being used.

TVM accounts for value with as much rigor as possible even though value is perceived differently depending on many subjective elements. TVM uses a system of standard values which makes it possible to compare cost with value on a uniform basis.

Standard costs and standard values facilitate analysis and avoid data overload. Separately TVM allows for the analysis of standard values and the use of this set of metrics to understand differences between societies and to help with the determination of priorities.

External resources complicate analysis. The performance of the community is a function of the amount of external resources needed to maintain a good quality of life. A low performing community is unable to maintain its quality of life without getting external resources. A high performing community needs no external resources to maintain and improve its quality of life.

There are organizations that use large numbers of unpaid volunteers. The labor resource is money free to the organization, but the “opportunity cost” for the volunteers is not zero, and the optimum opportunity for the organization should be bigger than the value of just “stuffing envelopes”!

|

Disbursement is no way to measure performance

The World Bank did a disservice to itself and to the whole process of development by using the amount of loan disbursed as a proxy measure for how much development progress was being made. It was a stupid idea and went on for years.

In the current global malaria control programs, the amount being disbursed is a more prevalent measure than the amount of malaria disease reduction. The idea of effectiveness measurement is missing!

|

|

Derivatives of Cost, Price and Value

|

Profit ... derivative of money cost and money price.

The simple definition of profit is based on money cost and money price. In financial accounting and reporting to corporate stakeholders, profit is the key measure that drives everything. Cost and price make it possible to calculate margins and profits ... and this is what is done in normal corporate accountancy and financial reporting. As we shall see later, in modern financial reporting both cost and price are capable of being distorted so that the most favorable margins and profits are being reported ... something that is allowed by self-serving accounting rules (think FASB) but would not be tolerated where professional accountants embrace the fundamental core principles of accountancy.

But profit is more complex in modern financial accounting. Money profit is no longer just the delta between price and profit but might be something else. The accounts may not simply record assets at their cost but on some other basis ... including “mark to market”! This is a wonderful device for taking into account unrealized profit ... simply by recording their value in the balance sheet at a price that the assets could be sold for based on the present market. Fifty years ago, a practice like this would have been banned absolutely based on the prevailing accounting principles ... but lobbying and legislation has overturned old principles and replaced them with laws and rules that are convenient ... in a rising market ... and very dangerous at any other time! Convenience is not a good principle of accounting.

Profit is at the center of the capitalist economic construct ... and is a useful metric as it relates money revenue with money costs, and serves as a useful and practical proxy for performance and productivity. But profit is is not a good proxy for socio-economic performance and the way quality of life in a community changes ... nor the sustainability of the community. In fact, thoughtless optimizing or maximizing of profit is a fairly certain way of creating an unsustainable future.

|

Value adding ... derivative of value and cost.

If, rather than just money, the metric of performance is value adding ... that is the increment of value from an activity, then there is a very much better measure of progress and performance. Value ... that is value to society ... is almost totally excluded from modern financial and economic metrics. The reasons are many including (1) it has a subjective dimension that makes valuation difficult; and, (2) it has a devastating impact on the norms of financial valuation of corporate activity.

|

Cash flow ... derivative of money cost and money inflows.

Cash flow is a metric that relates to sustainability in a world where money is the medium of exchange. Cash is used to pay bills. Money inflows may come from revenues which are a function of price, or they come from financing or some change in the balance sheet like sale of assets. Activities that result in a persistent cash deficit will fail in due course, simply because the money runs out. The timing of the demise of the activities may be delayed by borrowing ... but that also will fail in due course.

|

Sustainability.

Activities that have value adding positive and cash flow being positive are sustainable ... and desirable. Activities that are cash flow positive and profitable are money sustainable but maybe not socio-economically sustainable ... and these activities have come to dominate rich developed economies in the post World War II period. By ignoring critical issues of value destruction society had the impression of wealth being created ... but much was mere puffery and the balloons were bound to break. But worse, society built the appearance of wealth while setting the stage for potentially catastrophic global disasters in the future.

|

|

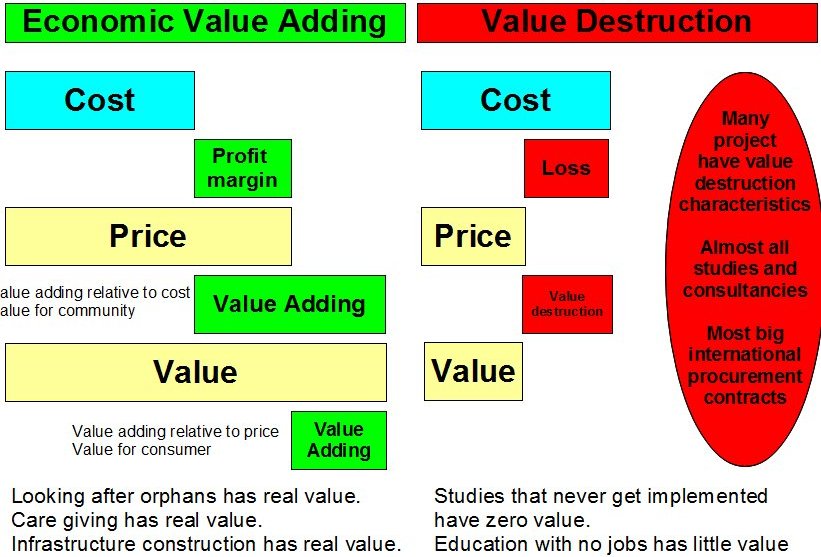

The Value Destroying Project

|

|

|

This graphic atttempts to show the huge potential for value add when a project does important work like:

- Looking after orphans

- Care giving

- Infrastructure

and also shows the almost total waste that is associated with work that involves:

- Studies with no action

- Education with no job opportunity

The international development assistance community has been badly managed for a very long time. While many of the people actually doing the work are highly motivated and good people, the system they are working with has huge deficiencies.

|

|