|

|

TVM CORE CONCEPTS

PROCESSES

EFFICIENT PROCESSES ARE FOUNDATION FOR SOCIO-ENVIRO-ECONOMIC EFFICIENCY

|

PROCESS IS EVERYWHERE

The efficiency of PROCESS will determine how well the WORLD works

|

|

|

PROCESS IS EVERYWHERE ...

NOTE: The PROCESS is equivalent to the NODE in context / entity / relationship diagrams. PROCESS is the NODE that is at the center of all person built activities

PROCESS uses inputs (labor, materials, energy, knowhow, natural resources, etc.) and in the process degrades the environment;

PROCESS produces PRODUCTS (goods and services) ... outputs ... that enable good quality of life and living standards.

|

|

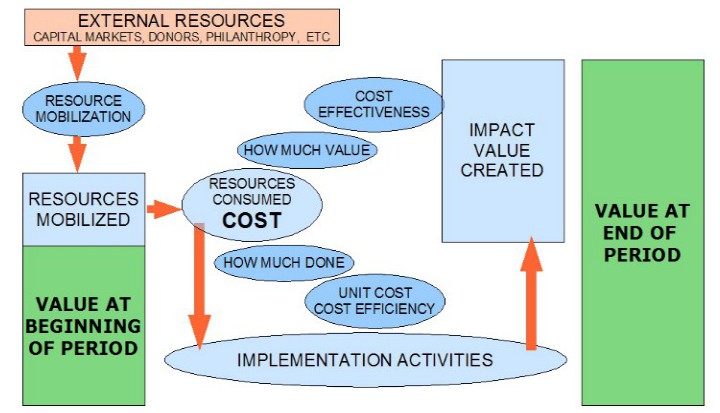

EFFICIENCY AND EFFECTIVENESS OF A PROCESS

This is more than PROFIT ... it incorporates also impact on PEOPLE and PLANET

|

EFFICIENCY is not only the PROFITABILTY of the PROCESS …

… but also how much GOOD IMPACT there is for PEOPLE and SOCIETY…

… and how little BAD IMPACT for SOCIETY and the ENVIRONMENT.

|

|

.

|

FRAMING THE PROCESS

This is more than PROFIT ... it incorporates also impact on PEOPLE and PLANET

|

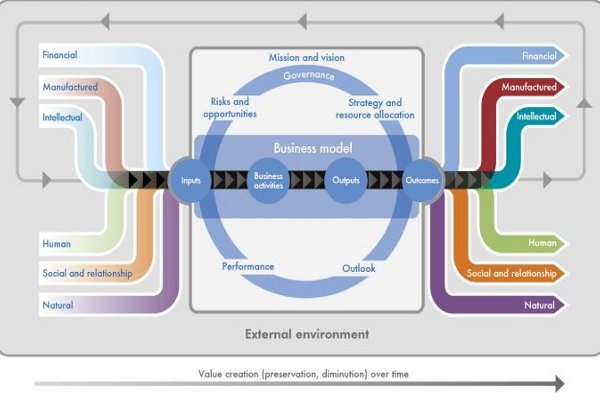

The IIRC Analysis Framework

|

IIRC Value Creation Process

This is a representation of PROCESS promulgated by IIRC (International Integrated Reporting Council) as the foundational construct for Integrated Reporting (IR).

Both TVM and IIRC / IR embrace the idea that ALL the capitals should be brought into account.

The six (6) capitals used by IIRC are have some similarity to the 3 capital top level segmentation used by TVM

|

The Framing of the Capitals

|

|

IIRC

|

IIRC / TVM

|

TVM

|

A. Financial

B. Manufacturing

C. Intellectual

D. Human

E. Social and Relationship

F. Natural

|

SOCIAL CAPITAL

D. Human

E. Social and Relationship

NATURAL CAPITAL

F. Natural Capital

ECONOMIC CAPITAL

A. Financial

B. Manufacturing

C. Intellectual

|

SOCIAL CAPITAL

Human Capital

Relationship Capital

Locational Capital

NATURAL CAPITAL

Land

Water

Air

Resources

Biodiversity

Ecosystems

ECONOMIC CAPITAL

Financial

Physical

Intangible

|

With IIRC the 'Value Creation Process' is centered on the business organization. While this is important, it is not sufficient. What goes on outside the business organization is arguably more important than what happens inside the organization.

With IIRC the business organization draws from the 6 capitals (inputs to the process) and impacts the 6 capitals (outcomes of the process).

With the business organization there are business activities ... which are similar to PROCESS in TVM.

In addition the IIRC graphic has reference to these ideas:

- Mission and Vision:

- Risks and Opportunities,

- Governance, Strategy and Resource Allocation;

- Performance and Outlook.

In the TVM framing, there are tighter links between the activities of the business as they are recorded in the financial accounting system and the activities and flows that have impacts on all the capitals, both those owned by the company (reporting entity) and the world outside the company and its reporting envelope.

This is reflected in the following graphic.

|

|

|

|

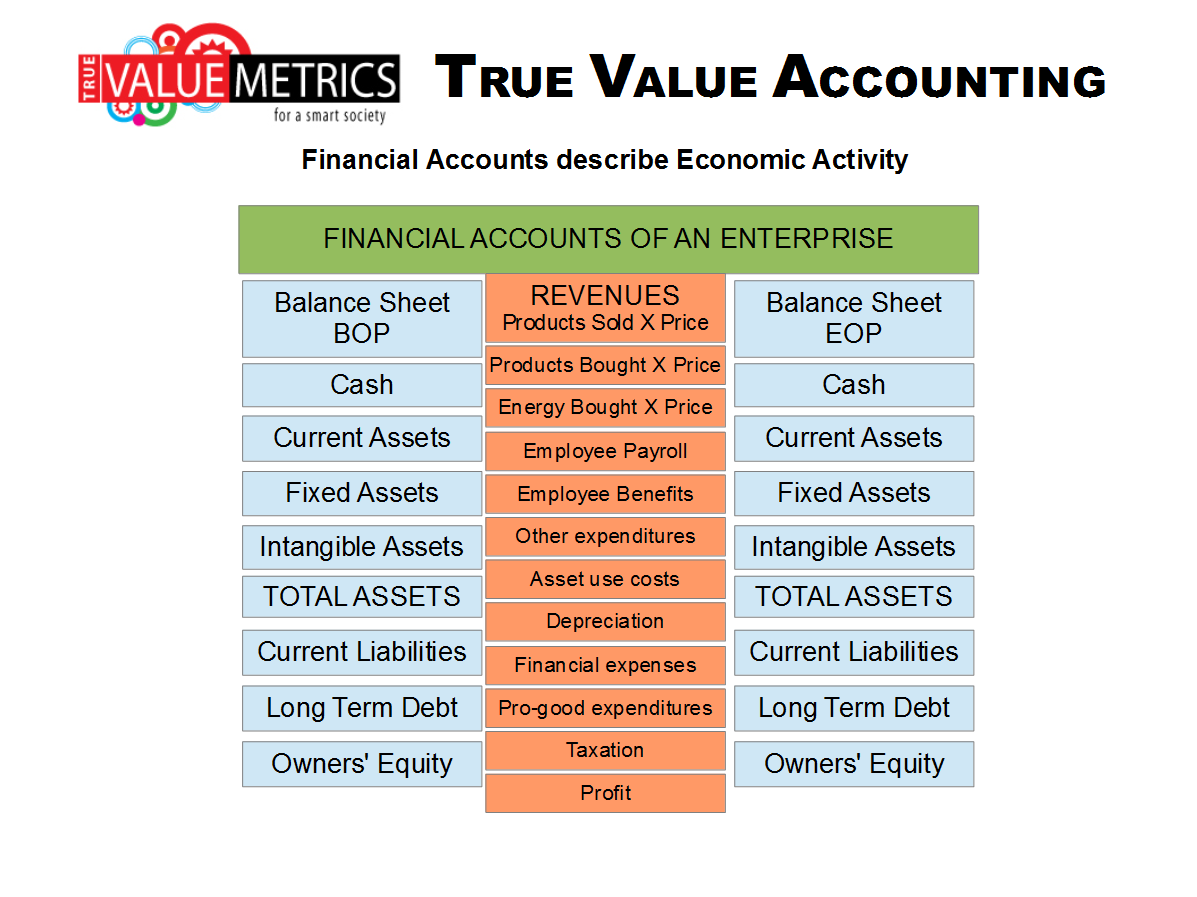

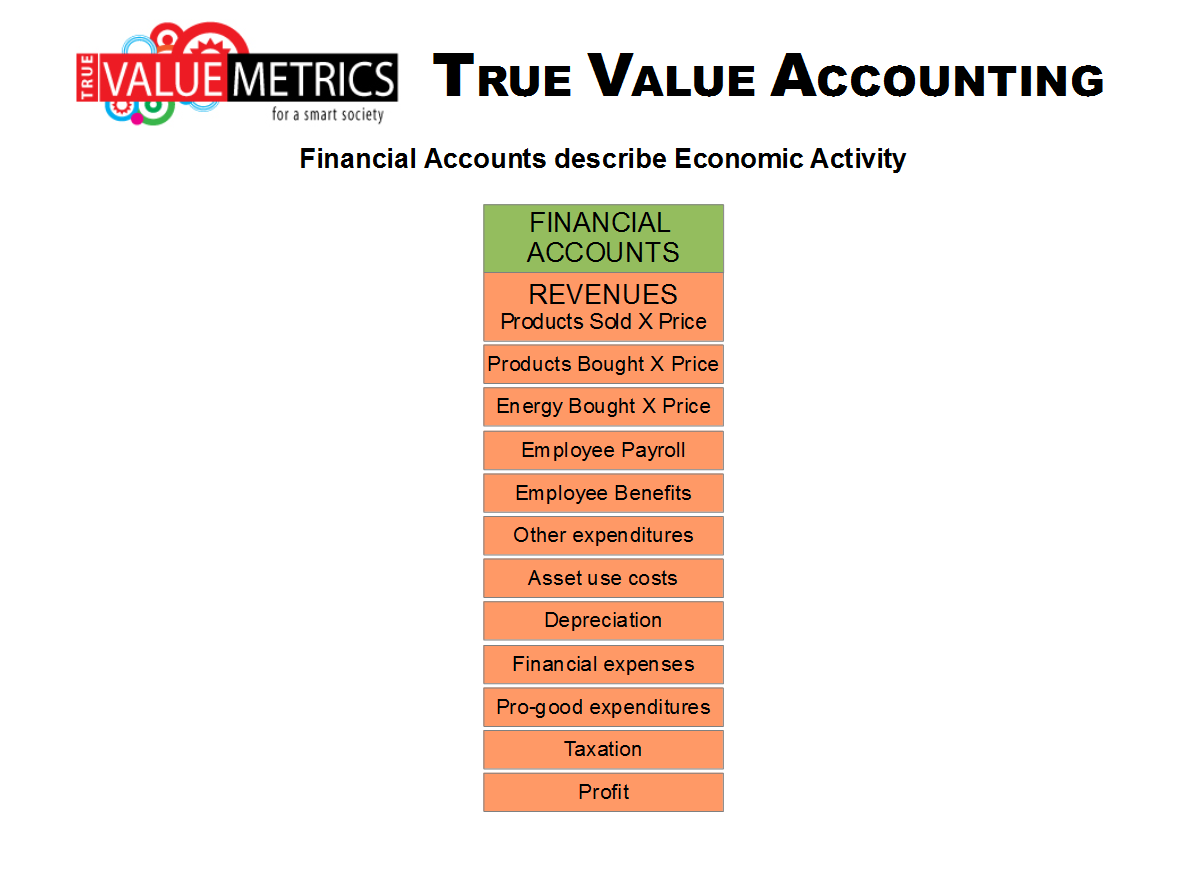

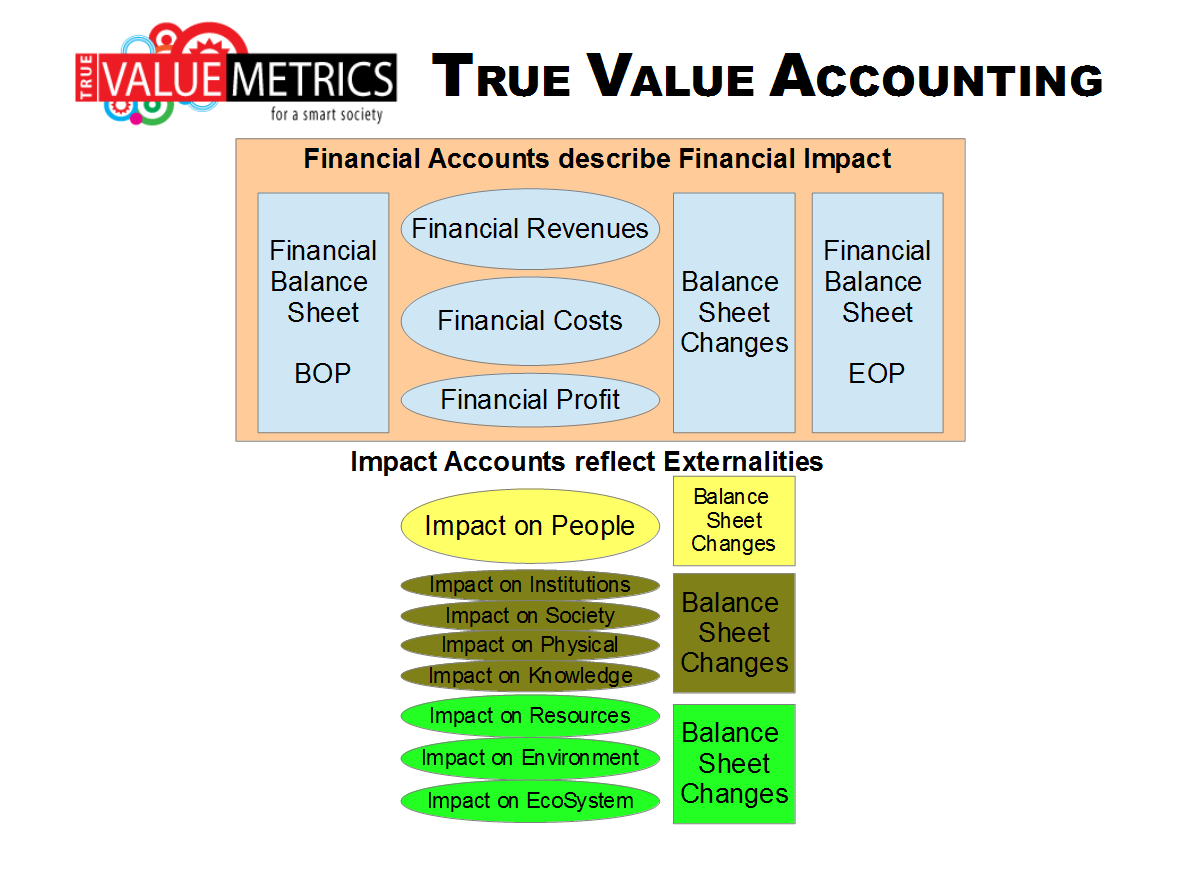

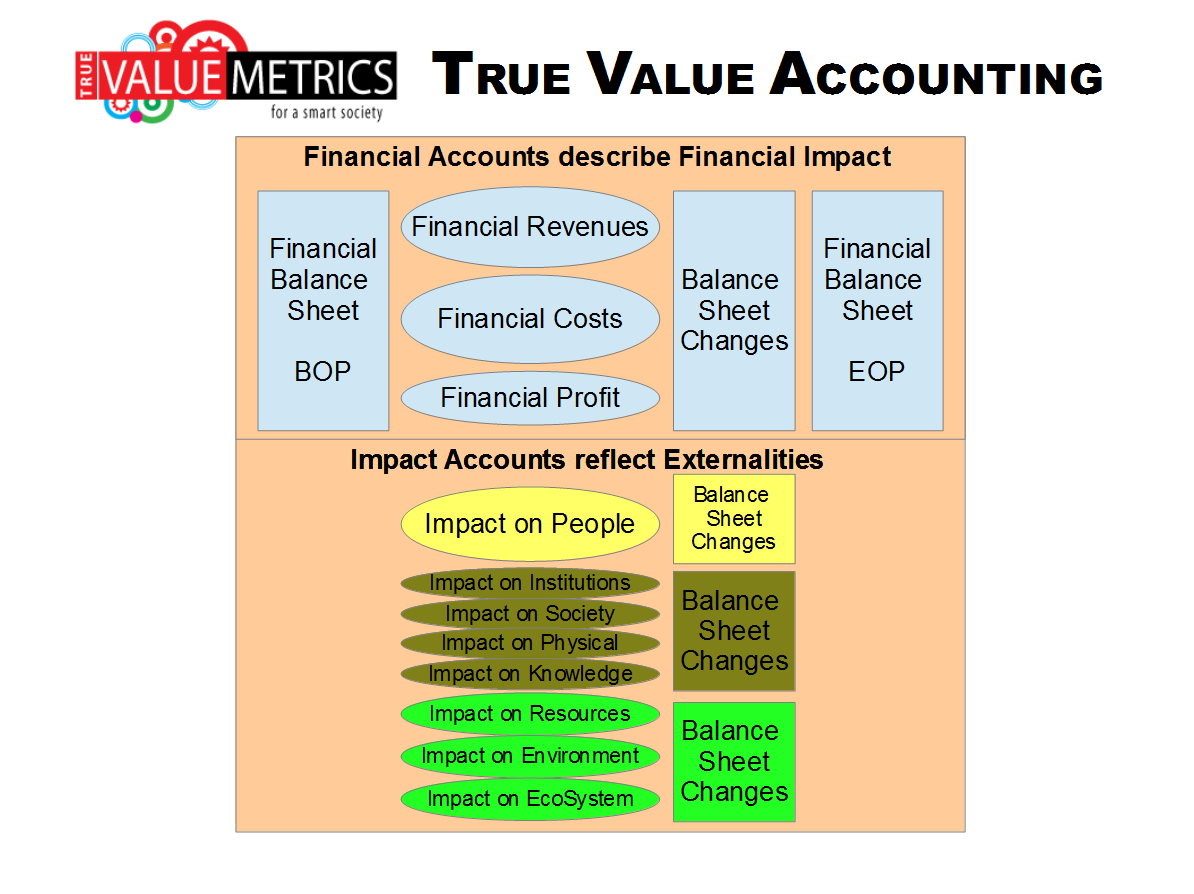

CONVENTIONAL MONEY ACCOUNTING IS VERY POWERFUL

HOWEVER ... these accounts ONLY describe economic activity in financial or money terms while completely ignoring impact on everything else.

|

|

This graphic shows the relationship between the Balance Sheet at the beginning of the period (BOP) and the Balance Sheet at the end of the period (EOP) and the Profit and Loss Account (P&L Account) for the peiod.

A core feature of double entry accounting is that the change in the balance sheet from the BOP to the EOP is the same as the profit for the period shown by the P&L Account

|

|

|

|

|

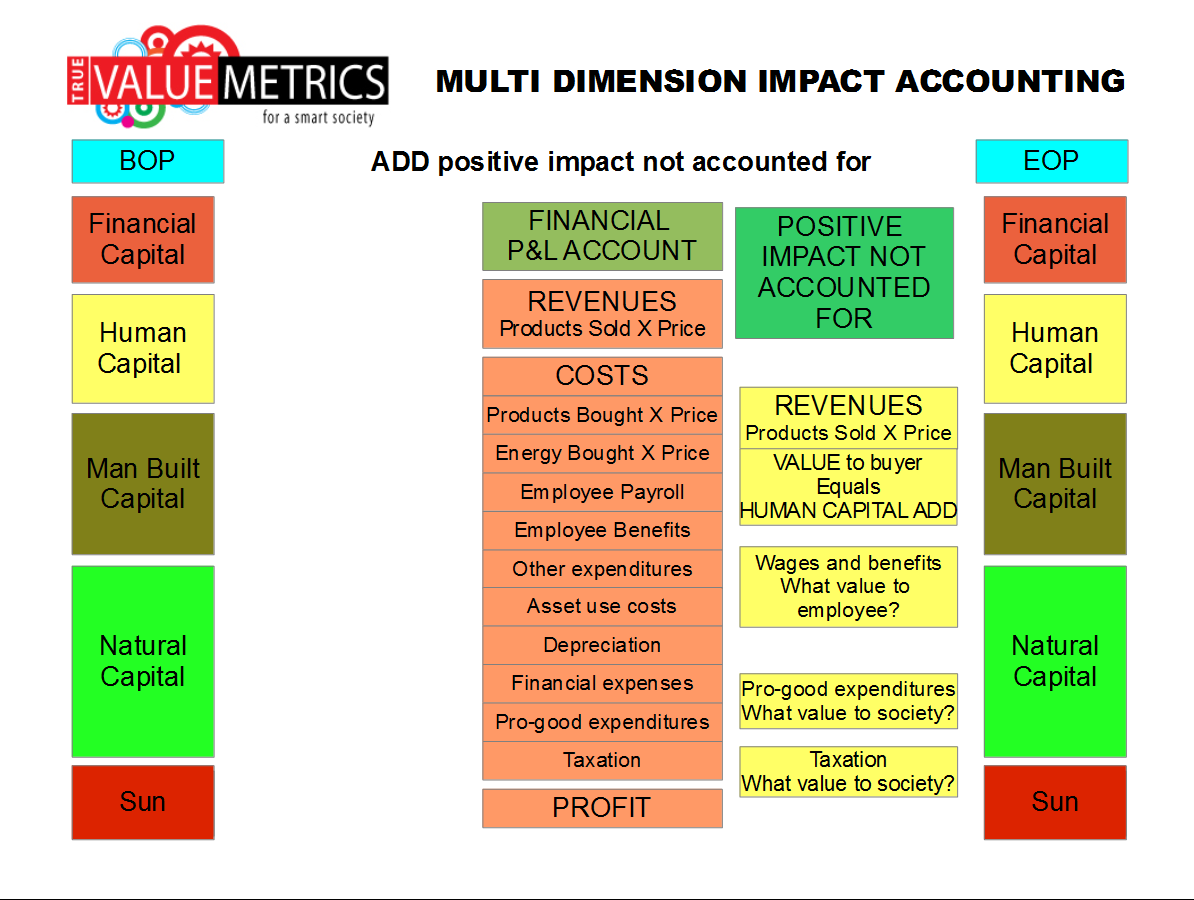

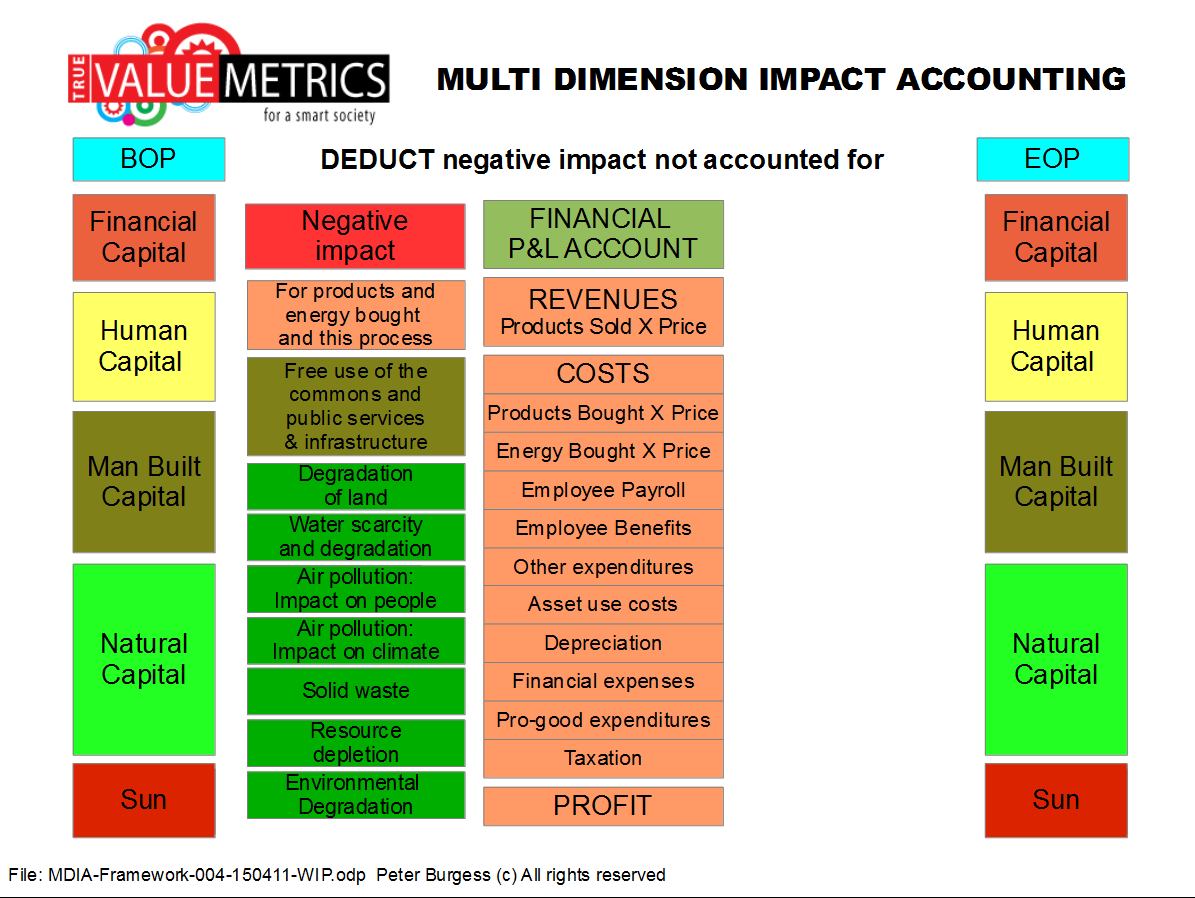

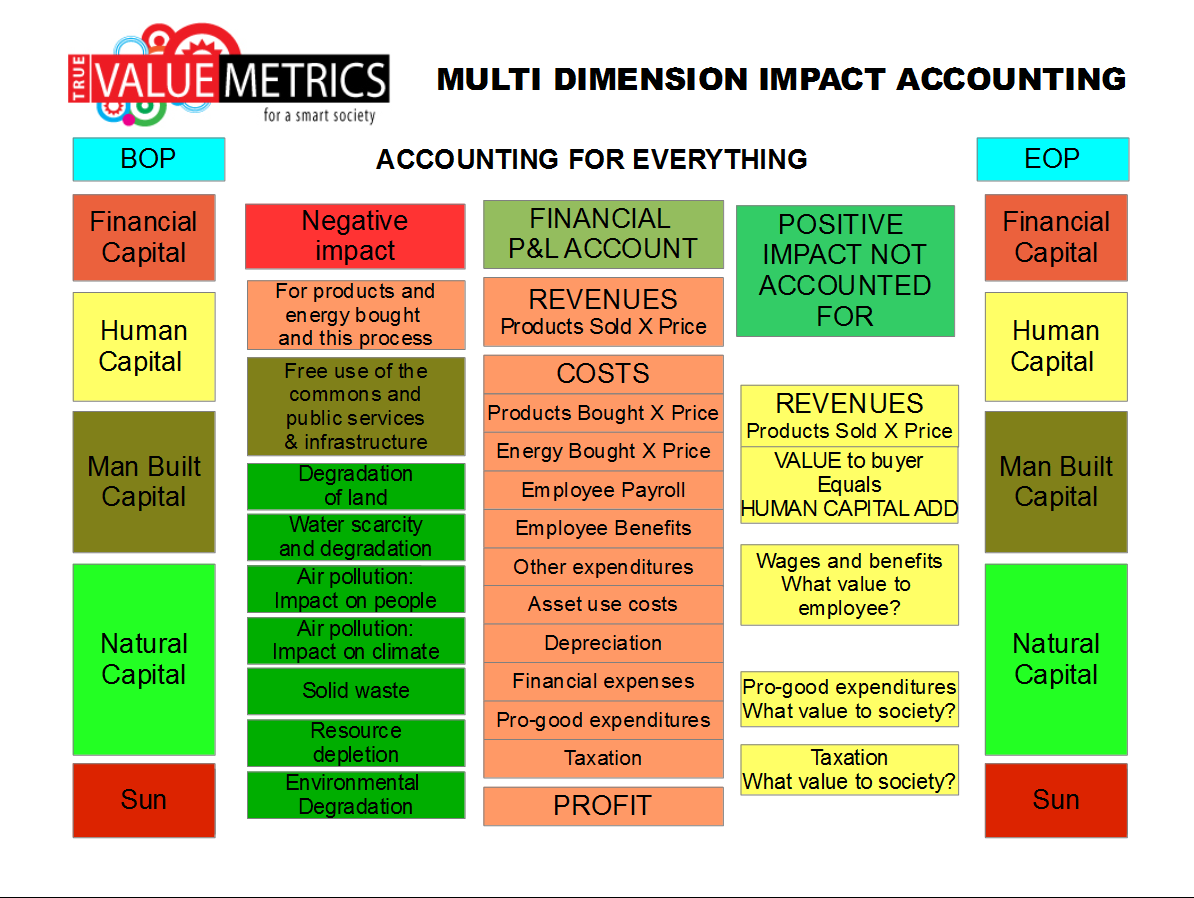

AUGMENTING CONVENTIONAL ACCOUNTING TO ADD IMPACT

How the TVA data architecture adds IMPACT of the PROCESS in an easy and rigorous manner

|

|

Add the GOOD impacts to the accounting, analysis and reporting

|

|

|

Deduct the BAD impacts to the accounting, analysis and reporting

|

|

|

Have GOOD and BAD impacts together

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOME EXAMPLES OF MAJOR PROCESSES USES IN DIFFERENT SECTORS

Sub heading

|

|

|

… and specifically this mean making all the PROCESSES that are used to support our QUALITY OF LIFE more efficient not only to make more PROFIT but also to have a BETTER IMPACT on SOCIETY (PEOPLE) and ENVIRONMENT (PLANET).

|

|

|

PETROLEUM REFINING / PETROCHEMICALS

|

|

Positive impacts:

... Enabled mobility

... Enabled new materials

Negative impacts:

… Natural Capital ... Resource Depletion ;

… Natural Capital ... impact of emissions on GHG concentration and climate change ;

… Economic Capital ... impact of climate change on the built environment (especially coastal cities) ;

… Social Capital ... risk of accident during production and transportation ;

… and a whole lot more.

|

|

About the SECTOR / INDUSTRY ... technical development and the performance of the processes

|

Open L0700-SI-ENERGY

|

|

About the way this SECTOR / INDUSTRY flows in STREAMS / STRANDS / STRINGS through the system

|

Open L0700-SS-ENERGY

|

|

For example … in AGRICULTURE ...

better stewardship of WATER use;

… attention to pollution from run-off containing fertilizers, herbicides, pesticides, etc;

… more responsible use of animal medication to avoid risk of drug resistance important for human health;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

|

For example … TRANSPORTATION ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… attention to the matter of waste water and solid matter polluting the environment;

… and a whole lot more.

|

|

|

For example … OFFICE BUILDINGS ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… and a whole lot more.

|

|

|

For example … HEAVY INDUSTRY ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… attention to the matter of waste water and solid matter polluting the environment;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

|

For example … MINING ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… degradation of the land;

… attention to the matter of waste water and solid matter polluting the environment;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

|

For example … CONSTRUCTION ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… attention to the matter of waste water and solid matter polluting the environment;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

SOME CONCLUDING OBSERVATIONS

Sub heading

|

|

|

CONCLUDING OBSERVATION ...

… more than anything else improving the EFFICIENCY of PROCESS will change the trajectory of global socio-enviro-economic performance;

… in the past efficiency has simply been about less COSTS and more PROFIT;

… in the future EFFICIENCY has to be about better QUALITY OF LIFE for PEOPLE with very little of no damage to the ENIRONMENT (PLANET)

INTEGRATED FINANCIAL AND IMPACT ACCOUNTING ...

… integration of financial and impact accounting will make it possible for very much better decisions to be made.

… high efficiency can be rewarded and there can be social accountability for bad practices and low efficiency.

CHIEF PERFORMANCE OFFICER

Maybe in the near future it will be possible to rename the CFO (Chief Financial Officer) to be the CPO … the Chief Performance Officer, a C-level position that integrates financial performancewith impact on society (people) and impact on the environment (planet).

|

|

|

|

|