|

#11

|

TVM BASIC ACCOUNTING

CORE ELEMENTS OF FINANCIAL ACCOUNTING

|

|

CONVENTIONAL FINANCIAL ACCOUNTING EMBRACES

BALANCE SHEET & PROFIT AND LOSS ACCOUNT

|

|

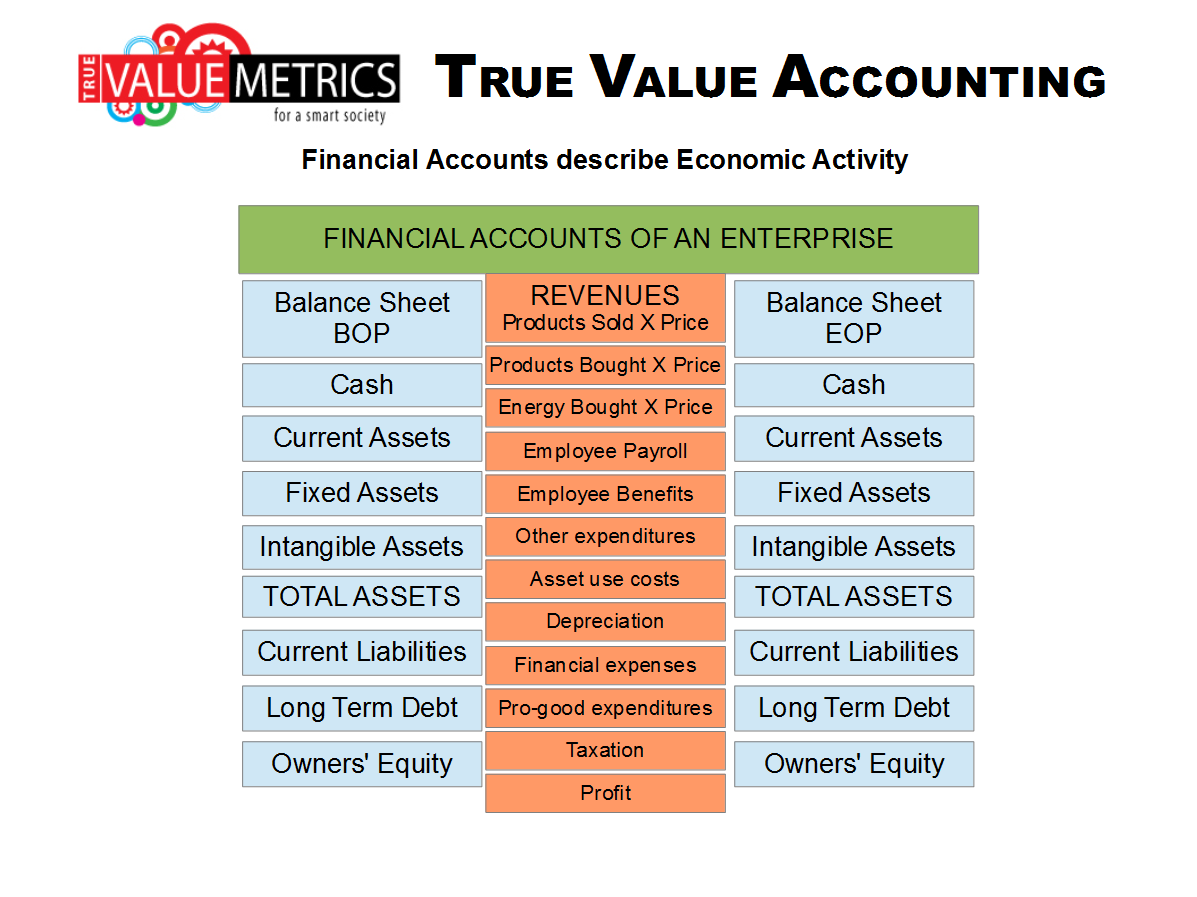

This graphic shows the basic elements of conventional financial reporting:

- The elements of the Beginning of Period (BOP) Balance Sheet

- The debits and the credits for the Profit and Loss Account of the period

- The elements of the End of Period (EOP) Balance Sheet

|

TPB note: The profit may be determined either by adding up all the profit and loss account transactions or by the totality of the changes between the BOP and EOP balance sheets. There is something wrong when these two calculations produce different answers. When this is done for an individual for-profit entity, the results may look OK, but when the idea is applied to all the capitals, then the results are catastrophic ... but who cares if it is all about economic profit and only that!

|

TRUE VALUE METRICS ENHANCES ACCOUNTING TO

INCLUDE IMPACT ON SOCIETY AND THE ENVIRONMENT

|

|

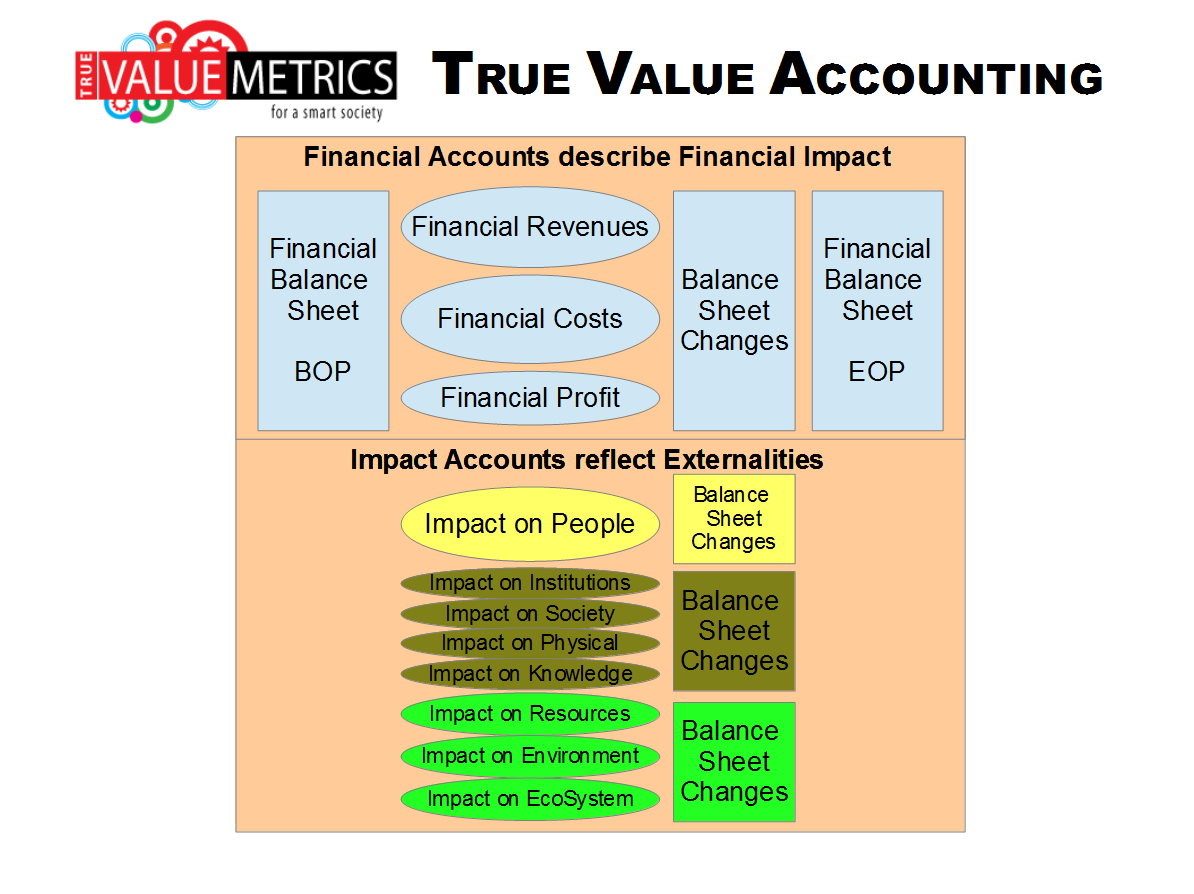

True Value Impact Accounting enhances financial accountancy to show external impact (externalities) that goes beyond the conventional reporting envelope, to show also:

- Social Impact .. changes to Social Capital

- Economic Externalities ...changes in Economic Capital outside the reporting envelope

- Environmental Impact ... changes in Natural Capital

|

ACCOUNTING FOR EXTERNALITIES AND

ALL THE SOCIAL, NATURAL and ECONOMIC CAPITALS

|

|

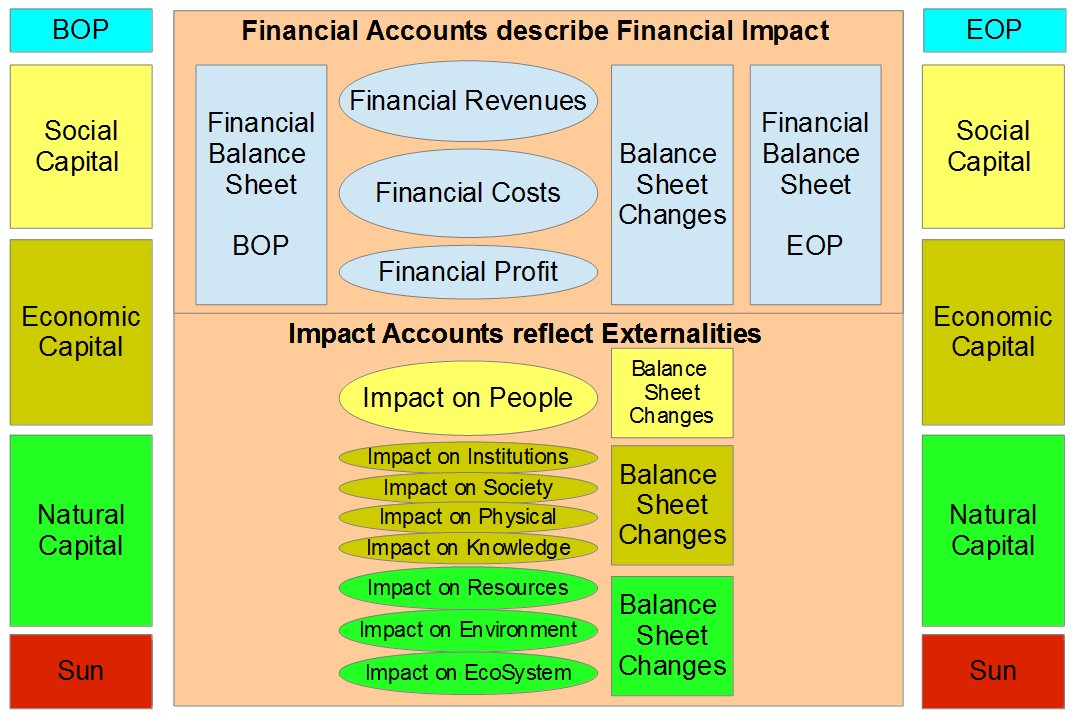

This graphic combines three of the key components of TVM's enhanced accountancy framework:

- The balance sheet and profit and loss accounts of conventional financial accounting

- The impact the core reporting entity is having on the external capitals

- The STATE of the external capitals

This basic framework applies for the corporate organization where conventional accountancy has been used for a very long time, but the numbers also nest in a manner that has similarities with business consolidations and group accounts.

In the case of TVM, this framework may be applied in a variety of different ways and for every possible perspective including:

- for multiple aspects of the complex for-profit corporation

- the individual process

- the stand-alone facility

- the supply chain

- separate locations

- the complete organization

- for the individual

- for the family

- for the place

- for a community

- for a region

- for a country

- for a product

- for a project or program

|

|