Date: 2026-05-25 Page is: DBtxt003.php L0900-MF-Sustainability-02a

|

PROGRESS AND PERFORMANCE REPORTING

Socially Responsible Context of Sustainability Reporting A framing articulated by Marco Tavanti |

| HOME | SiteNav | Chrono | Briefs | SEES | capitals | activities | actors | place | products | SI | SS | metrics | TPB |

| . |

|

|

Sustainability

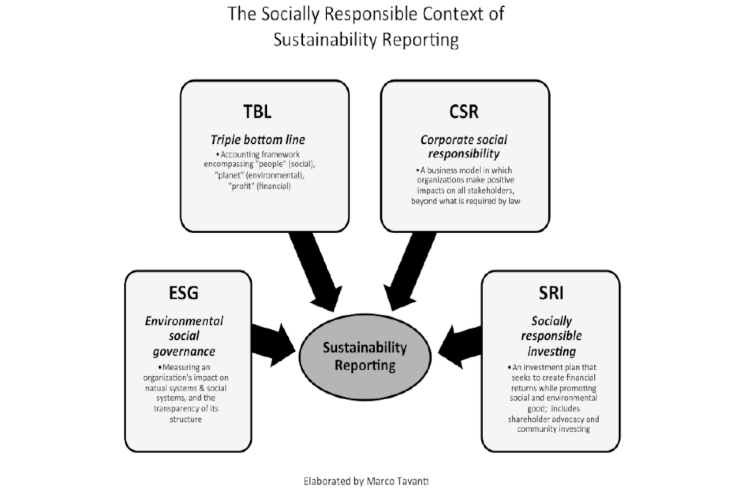

The problem with this formulation is that TBL (Triple Bottom Line), CSR (Corporate Social Responsibility), ESG (Environmental Social Governance) and SRI (Socially Responsible Investing) are all dealing with one huge interconnected system, yet there is little or no coherence and compatiblity between these four metrics. It is no surprise that goals do not get achieved! TVM, on the other hand uses an analysis framework that is comprehensive and coherent where ACTORS do ACTIVITIES that use RESOURCES from ALL the CAPITALS to produce IMPACTS that are beneficial or not for SOCIETY (PEOPLE) and also with ECONOMIC benefit or not (PROFIT) while doing the least damage to the ENVIRONMENT (PLANET) |

|

TBL

(Triple Bottom Line), Accounting framework encompassing people (social), planet (environmental) and profit (financial). |

CSR

(Corporate Social Responsibility), A business model in which organizations make positive impacts on all stakeholders beyond what is required by law. |

ESG

(Environmental Social Governance) Measuring an organization's impact on natural systems and social systems and the transparency of its structure. |

SRI

(Socially Responsible Investing) An investment plan that seeks to create financial returns while promoting social and environmental good - includes shareholder advocacy and community investing |

| Marco Tavanti ...Education ... 2018-experiential-by-design | Open PDF ... Tavanti-2018-experiential-by-design-JNEL-Journal.pdf |

|

Peter Burgess COMMENTARY ... added July 27th 2023 TBL ... the Triple Bottom Line ... was described by John Elkington in the 1990s. Why is it that there has been almost zero progress in using this framework of metrics to describe and manage the society, the economy and the environment that we all inhabit? I concluded a long time ago that the metrics in common use are the ones that are the most 'convenient' for those with wealth and power and influence. They are not the metrics that will do the best job of informing both the public and decision makers of the 'best' way to make the most beneficial progress for everyone. Business accounting and the related reporting has been in use 'for ever'. This from Google: The early development of accounting dates to ancient Mesopotamia, and is closely related to developments in writing, counting and money and early auditing systems by the ancient Egyptians and Babylonians. By the time of the Roman Empire, the government had access to detailed financial information.Double entry accounting was described in detail by Luca Pacioli in 14??, more than 500 years ago and many of the characteristics of modern financial accounting were incorporated into business law in the 19th century. The accountancy profession has served the business community quite well for over a hundred years, but has failed to modernise to be well suited for modern times. Among the many issues that need to be addressed is the singular focus on the investor when it comes to corporate reporting. I believe this has its origins in the widespread investor fraud that existed in the early days of the industrial revolution when business entrepreneurs blatently lied to potential investors about the performance of their companies. In recent years companies have taken to lying about their products, their social impact and their environmental impact ... less about their financial profits because this would be unlawful and addressed by the rules and regulations of 'auditors' and government and professional oversight bodies. Clearly ... the business community should be held to a higher and more modern standard than exists at the present time. Work has been done on this over the past several decades, but the results are quite modest and the pace has been outrageously slow. The reason for this is difficult to understand, but it could be that many of the people who have the competence to do the work do not want to engage because the status quo is likely better for them than a more effective system for a broader society, environment and economy, MORE TO BE ADDED |