|

MANAGEMENT METRICS

A TVM ENHANCEMENT OF THE IR FRAMEWORK

TVM has both betterment of all capitals AND

the complex interplay of all the impacts of activities

Peter Burgess COMMENTARY

There are many ways to look at the global socio-enviro-economic system. With TrueValueMetrics (TVM) the goal has been for the metrics to be as simple as possible while maitaining a reasonable fidelity to reality.

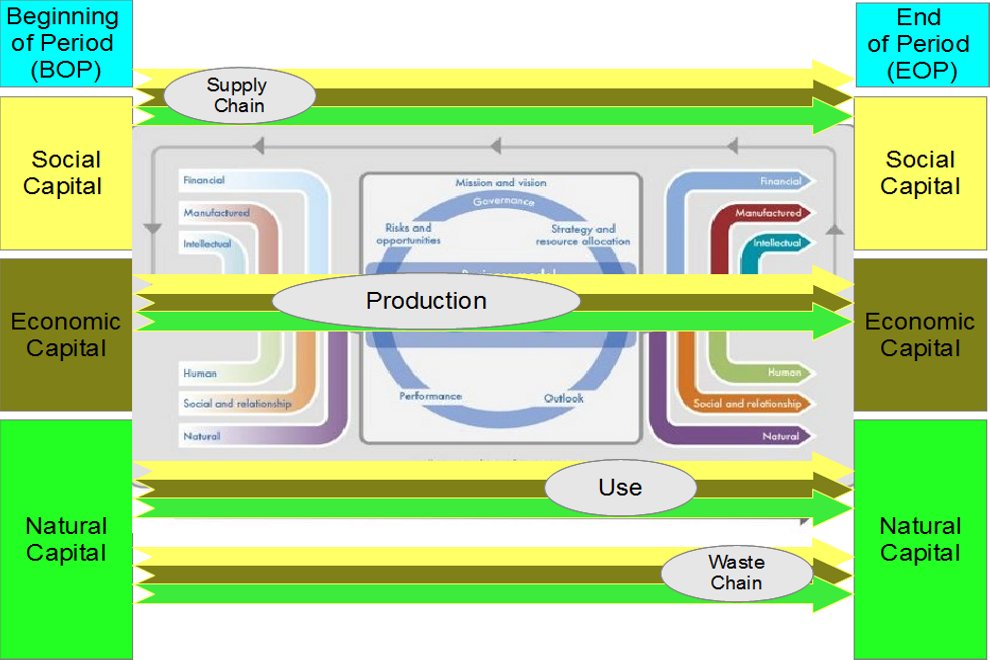

The whole of STATE or CAPITAL is broken down into three segments: (1) Social, (2) Natural or Environmental, and (3) Economic or Man-Built)

All of the ACTIVITIES in the socio-enviro-economic system have impacts ... both negative and positive ... on all of the CAPITALS.

Very early in my adult life, I was learning about the metrics associated with engineering systems and technology. Not long after this I was being trained to become a Chartered Accountant and it struck me that the logical framework of much engineering analysis had the same form as the core framework of double entry book-keeping.

This is an important strength of double entry accountancy which has been in use for several centuries as the dominant performnce metric in the economy going back to the Merchants of Venice and almost vertainly long before.

There are a multitude of ACTIVITIES all with different characteristics. The development of TVM has used the following classification as a way to help simplify and focus: (1) SUPPLY CHAIN (2) PRODUCTION, (3) USE, and (4) POST USE WASTE CHAIN.

MANAGEMENT is all about running AXTIVITIES so that there is the most improvement in the STATE or CAPITALS over time.

Conventional and prevailing and dominant financial accountancy is a powerful system with metrics that address the depletion of resources as measured by economic metrics like money and the augmentation of financial value as a result of economic activities. In most accounting and related reporting, the rules and regulations call for only a limited accounting of the impacts associated with activities ... but these rules and regulations are based on the need to resolve issues arising during the industrial revolution of the 19th century which now are of limited fitness of purpose for the issues that have emerged a hundred years later.

Simply put the dominant focus of accounting for business was to inform owners (investors) about the business performance and not much else, while in the modern day there is a need to inform all stakeholders about the impact of economic activity no matter where and in what legal form the activity is taking place.

The international accountancy profession of which I was once a part is failing impressively. It is worrysome that the big firms are not failing in terms of their own profit performance, but in terms of their true purpose and good impact on society and the environment.

Peter Burgess

|