OVERVIEW

MANAGEMENT

PERFORMANCE

POSSIBILITIES

CAPITALS

ACTIVITIES

ACTORS

BURGESS

|

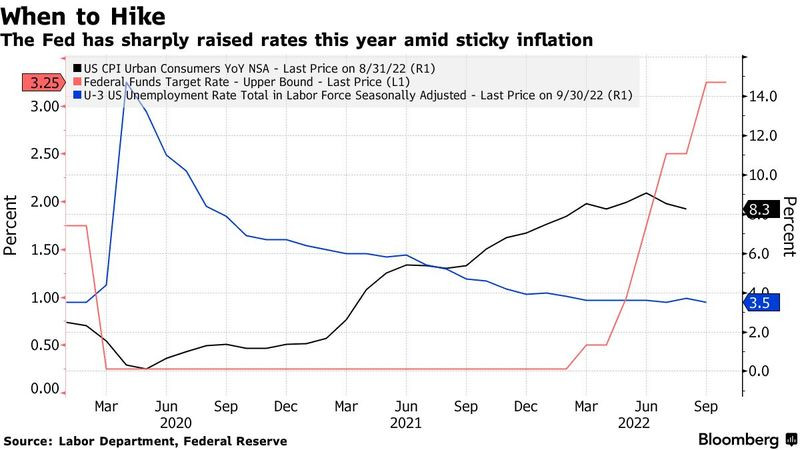

US FEDERAL RESERVE

POLICY CHOICES Bloomberg: Removing the Crutches ... Fed options in October 2022

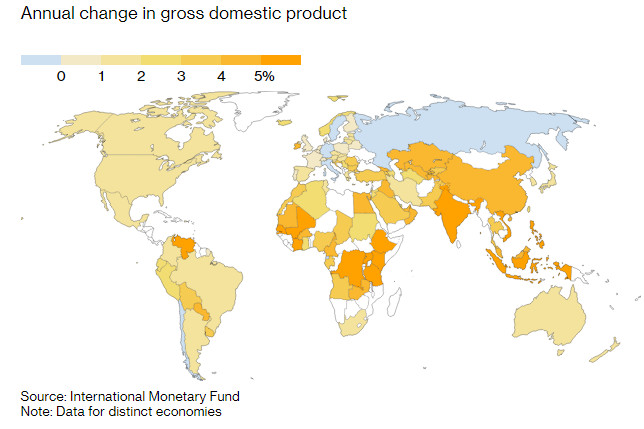

Global Economy in 2023 ... Annual change in gross domestic product Note: Data for distinct economies Original article: https://www.bloomberg.com/news/newsletters/2022-10-12/removing-the-crutches Peter Burgess COMMENTARY It bothers me ... rather it appals me ... that serious economsts and journalists rarely talk about the problem that is GDP. Gross Domestic Product (GDP) as it is calculated is an imossible metric to be guided by, though it is the one that has been used for decades. I was a student economist at Cambridge more tha 60 years ago and the problems with GDP were on the agenda back then, and yet the measure still dominates economic conversation and remains a big part of policy formulation. Both Keynes and Kuznets, both of whom had a rile in developing an early version of GDP as a matter of urgency in the 1930s wanted it to be refined or replaced in the early post-war years, but it has never happened. I have concluded that the reason for this is that the business community, the banks and the politicians are very comfortable with its sloppiness, and can often point to progress even when the true reality is exactly the opposite. The damage caused by extreme weather is ignored in the GDP computation, but the money disbursed to rebuild everything is included. This is equivalent to a business putting revenues into its accounts, but ignoring the expenses, That is no way to run a business, and GDP is no way to tune a nation! I am also uncomfortable with many of the published observations by the Fed concerning the state of the economy and what they are thinking about doing. My memory goes back to the economic events of the 1970s and the high inflation that was experienced at that time. In the 1970s it was the increasing price of crude oil that was driving inflation, with the price being controlled by an international cartel ... the Organization of Oil Exporting Countries (OPEC) orchestrated in large part by the Saudi oil minister Ahmed Zaki Yamani as I remember from that time. Looking back with the benefit of hindsight, I have concluded that the Seven Sisters ... the biggest oil multinational oil companies and some countries, especially the UK and the Netherlands ... were actively absent from any initiatives to make the OPEC cartel ineffective. Bottom line, the big oil companies and the UK and the Netherlands all stood to gain with the success of OPR=EC in raising oil prices globally, no matter the impact on people and other segments of national economies. Fast forward to the present time, and the big energy companies are taking advantage of a strong economy on the demand side and COVID related disruption in supply chains to exploit their customers to the maximum extent possible ... with little or no pushback from either the media, political leadership and policy wonks or academics. In my view there is a solution ... and that is for tax rules to included excess profits tax where profits surge because of market conditions unrelated to the costs and investments of the subject company. I know how complex and convoluted company structures can become ... but at some point this gets sorted out to show results to investors, and such results should be subject to an appropriate level of tax. In this context, an appropriate level of tax would be substantially more than what is commonplace at this point in history. I did grunt work on tax returns in the early 1960s when I was training in accountancy, and tax rates were twice what they are now, and tax avoidance way less sophisticated! Peter Burgess | ||

|

Bloomberg: Removing the Crutches

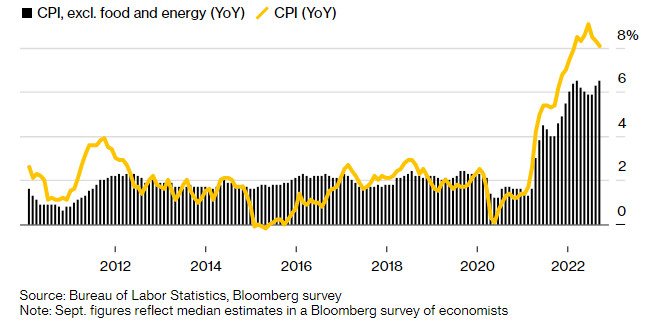

October 12, 2022 at 7:00 AM EDT You're reading the Bloomberg: New Economy Daily newsletter. Written by Malcolm Scott Hello. Today we look at global market shockwaves stemming from central banker comments in Washington, how Italy’s incoming government faces a grim first year, and a study asking what would have happened if the Federal Reserve had hiked interest rates earlier. A Painful Reminder As policymakers gather in Washington for the fall IMF meetings, one of them just issued a painful reminder that the kind of central-bank support markets have been accustomed to for so long can’t be relied on anymore. Bank of England Governor Andrew Bailey warned fund managers they have until the end of this week to wind up positions that they can’t maintain before the central bank halts its market support. That triggered a selloff in the pound that soon spread to US and then global stocks. Coming on the heels of a gloomy global outlook from the IMF, Bailey’s blast shot the UK to the top of markets’ long worry list. And don’t expect the US Federal Reserve to change its plans just because markets don’t like them either. Cleveland Fed President Loretta Mester said the central bank should stick with its approach to shrinking its massive balance sheet, notwithstanding ongoing volatility in financial markets. “I don’t see any need at the moment to adjust that plan. I think there is a lot of benefit to leaving that plan in place,” Mester said Tuesday during an interview with Kathleen Hays on Bloomberg Television. “Markets have understood the plan. They see it. They understand it.” The Bailey and Mester comments are a double reminder that in this age of inflation, squashing prices trumps the need to keep investors happy. Data on Thursday may show a key US inflation measure is set to return to a four-decade high. Inflation Remains Too High Core consumer price index seen returning to peak as headline CPI eases

Source: Bureau of Labor Statistics, Bloomberg survey Note: Sept. figures reflect median estimates in a Bloomberg survey of economists There’s other subplots bubbling away to keep officials in DC busy too. One is on the currency front, where there were starkly different views expressed relating to the dollar’s strength at unrelated events on Tuesday. In an interview with CNBC, US Treasury Secretary Janet Yellen said the strength of the dollar is the “logical outcome” of different monetary policy stances globally and that its value should be set by the market. “A market determined value of the dollar is in America’s interest,” Yellen said, sticking to a stance that seems to rule out coordinated efforts to weaken the greenback. By contrast, European Central Bank policymaker Francois Villeroy de Galhau said in a speech at Columbia University that Group of Seven foreign-exchange interventions can be effective if they’re coordinated. It was all very qualified: While the Bank of France chief reiterated the G-7 doctrine that central banks don’t target exchange rates, he said they can become “fundamentally misaligned” and “under such c ircumstances, there were G-7 interventions in the past.” “Several of them were effective, which we shouldn’t forget,” Villeroy said. A coded reminder to his US peers? —Malcolm Scott The Economic Scene The IMF’s projections of a grim global outlook are presenting Italy’s winner of the Sept. 25 election with an abrupt reality check. Giorgia Meloni is likely to preside over a contracting economy in her first year in office, the forecasts show. That adds to the challenges faced by the leader of Italy’s rightwing alliance, who is also struggling to find a finance minister.

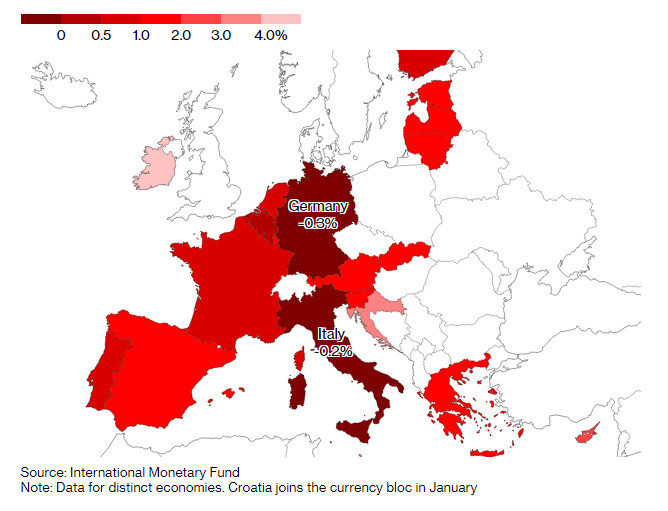

Euro-Area Economy in 2023

Annual change in gross domestic product

Source: International Monetary Fund Note: Data for distinct economies. Croatia joins the currency bloc in January As Alessandra Migliaccio and Craig Stirling explain here, Italy, the euro zone’s third-biggest economy is expected to shrink by 0.2% next year. It’s one of only two members facing a contraction in output, alongside Germany, which has also long been dependent on Russian fossil fuel. Today’s Must Reads

Source: Bloomberg Need-to-Know Research Fed rate increases last year would have only modestly reduced inflation in 2022, according to a new study from the San Francisco Fed which examines what critics view as a costly policy error. Hikes starting in March of last year and continuing through the beginning of 2022 would have only shaved off 1 percentage point from inflation, while increasing unemployment by 2 percentage points, San Francisco Fed economist Regis Barnichon found.

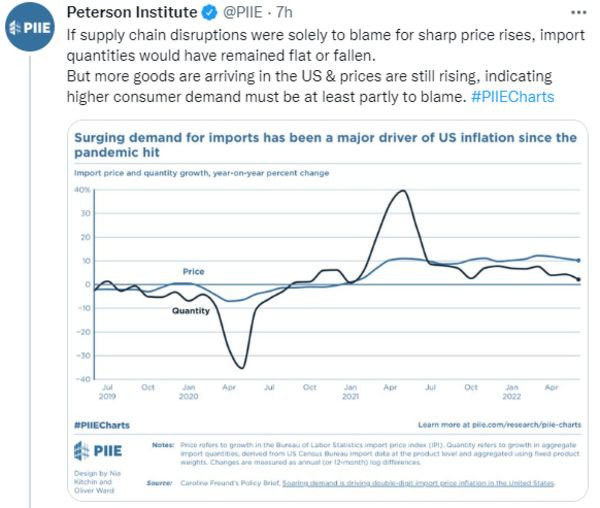

Source: Bloomberg The study also points to policy’s lags in affecting the economy. It takes at least one year for policy changes to impact inflation, Barnichon found. The analysis didn’t look at how an earlier ending of the Fed’s massive bond-purchase campaign would have impacted inflation and unemployment. The Fed in September 2021 announced its intention to start scaling back bond buying but it only completed that process in March, when it began to raise rates. On #EconTwitter Central banks have been eager to shift part of the blame for inflation to other issues like supply chains or energy. New research raises questions over such assertions:

Source: Bloomberg

| The text being discussed is available at | https://www.bloomberg.com/news/newsletters/2022-10-12/removing-the-crutches and |