CORE CONCEPTS

ENHANCING ACCOUNTANCY

|

|

|

A complete accounting of ALL the transactions in a socio-enviro-economic system is a challenge, and even with modern information technology, artificial intelligence, etc. is costly and most likely ineffective.

On the other hand, there is a way to account for PROGRESS at low cost and with high reliability using the core concept of double entry accountancy that has been used for hundreds of years.

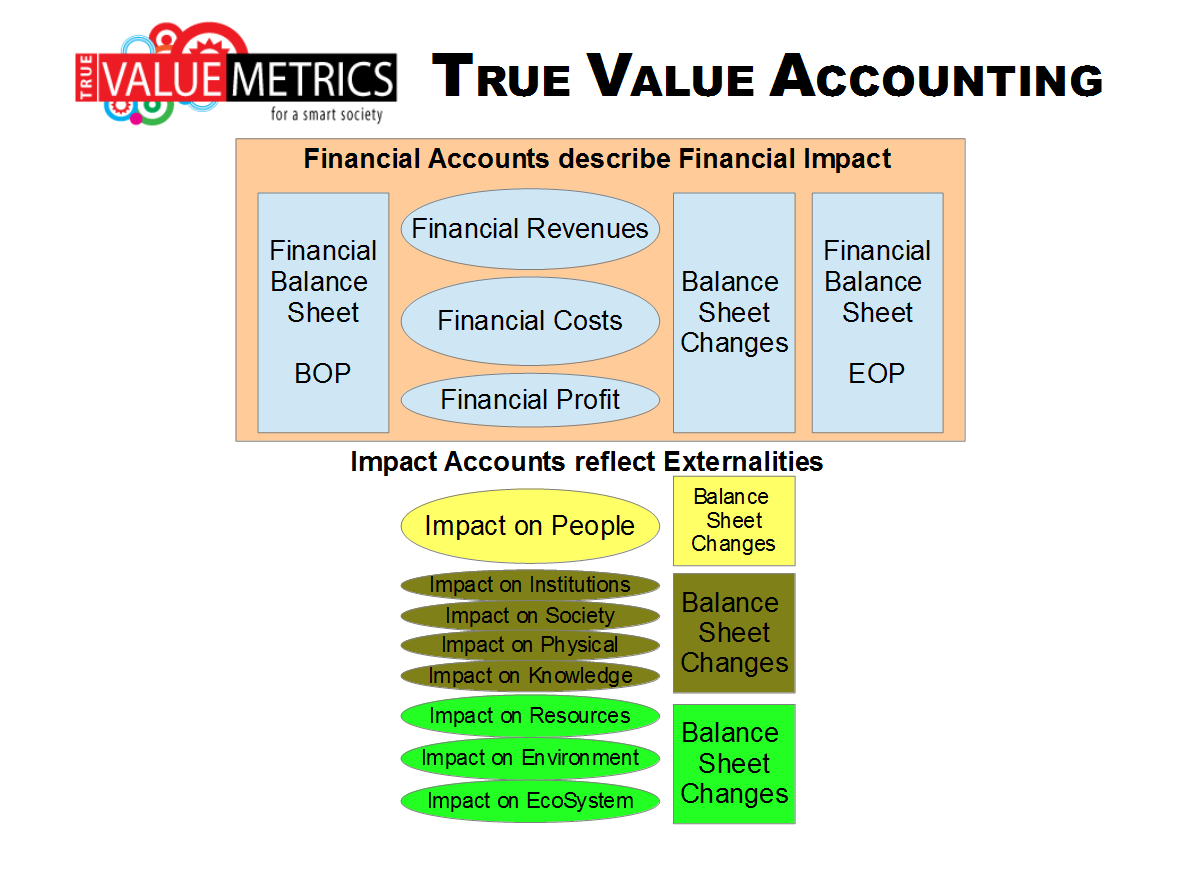

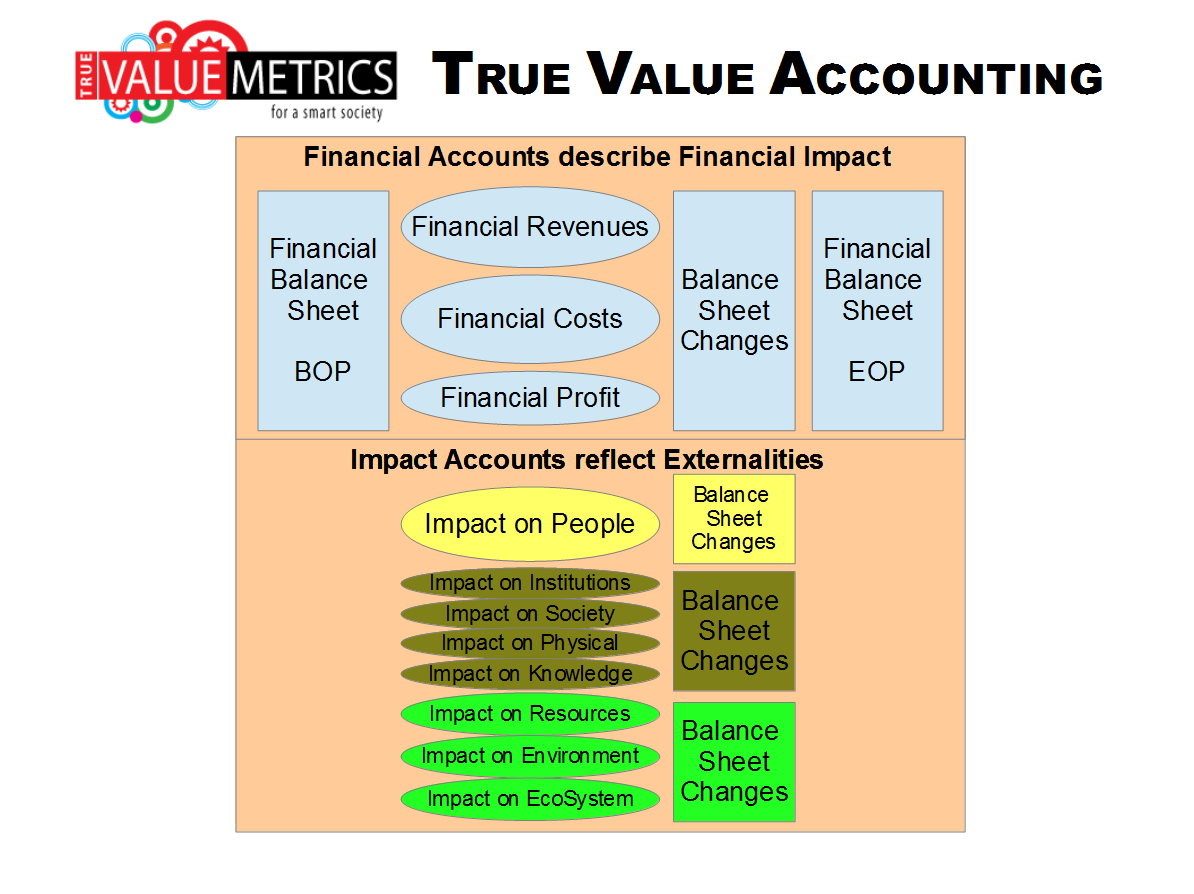

The relationship between the profit and loss accounts and the changes in the balance sheet is fixed. The profit shown in the P&L Accounts is the same as the net change in the balance sheet!

Accordingly, simply by knowing the change in the state from the beginning to the end of a period, progress may be measured without having any knowledge of the activities during the period that results in the change. Using this concept for progress measurement, it enables a significant simplification of the data collection and analysis process.

|

|

Steps in expanding conventional money accounting to true value impact accounting

|

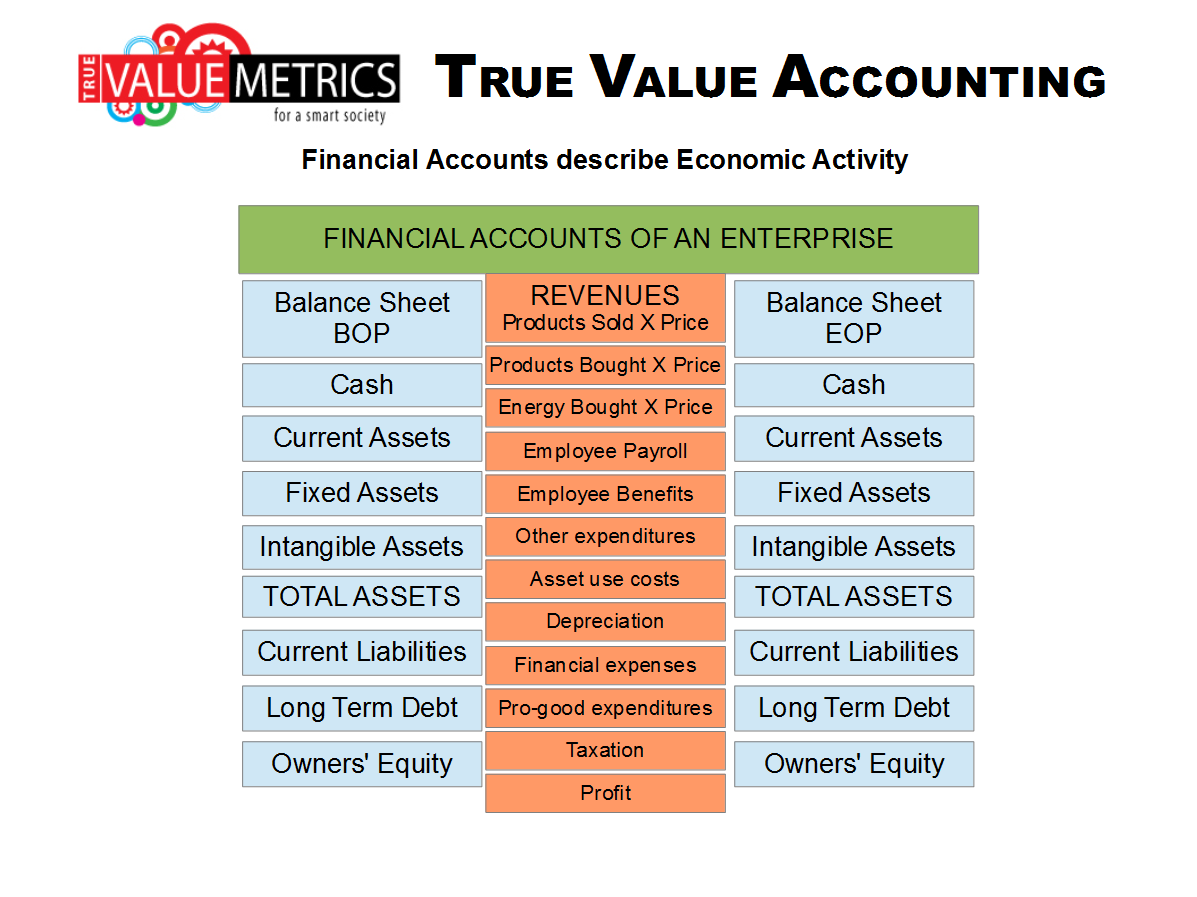

The financial performance of an organization can be measured by reference to the change in the balance sheet of the organization from the beginning of the period to the end of the period.

The profit and loss account explains the activities of the organization during the period.

The financial accounts are limited to the financial transactions of the organization. They ignore all externalities and do not include any information about the impact on people or the environment.

|

|

|

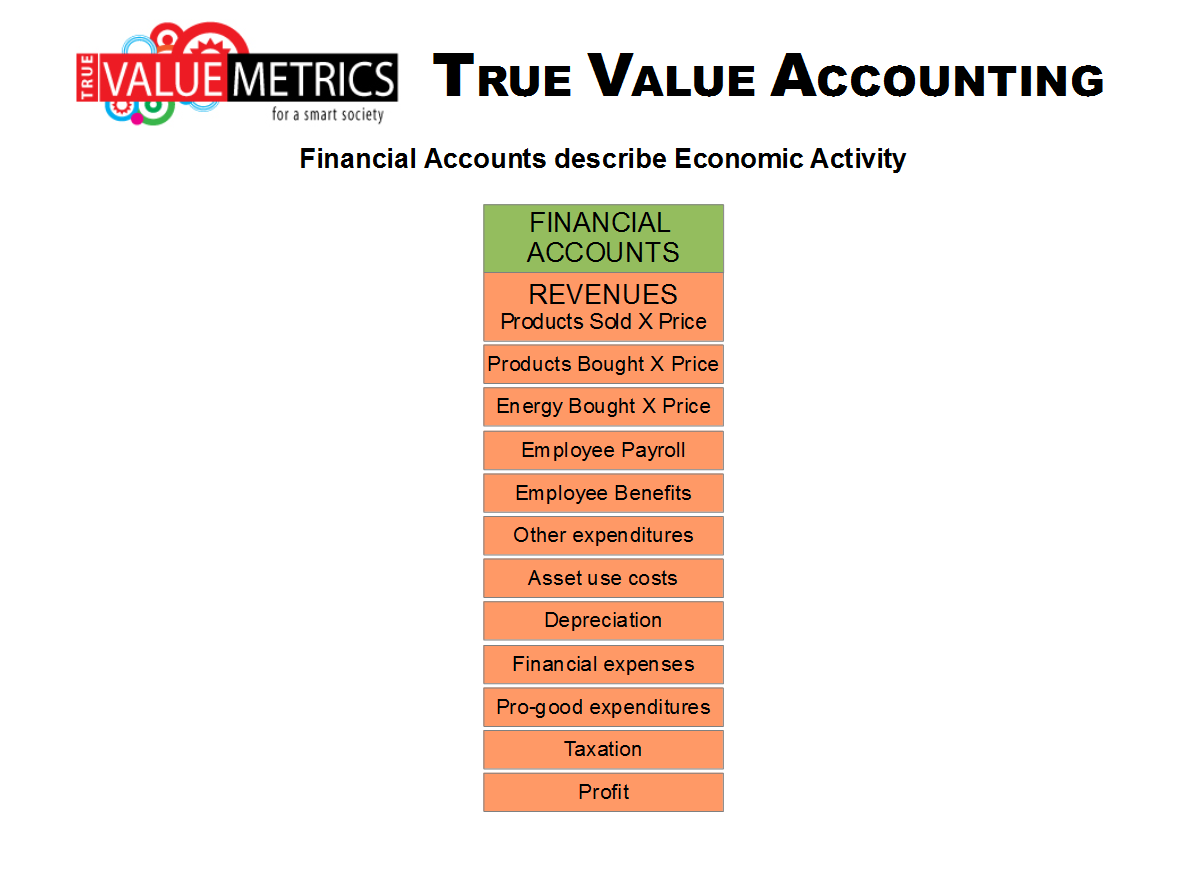

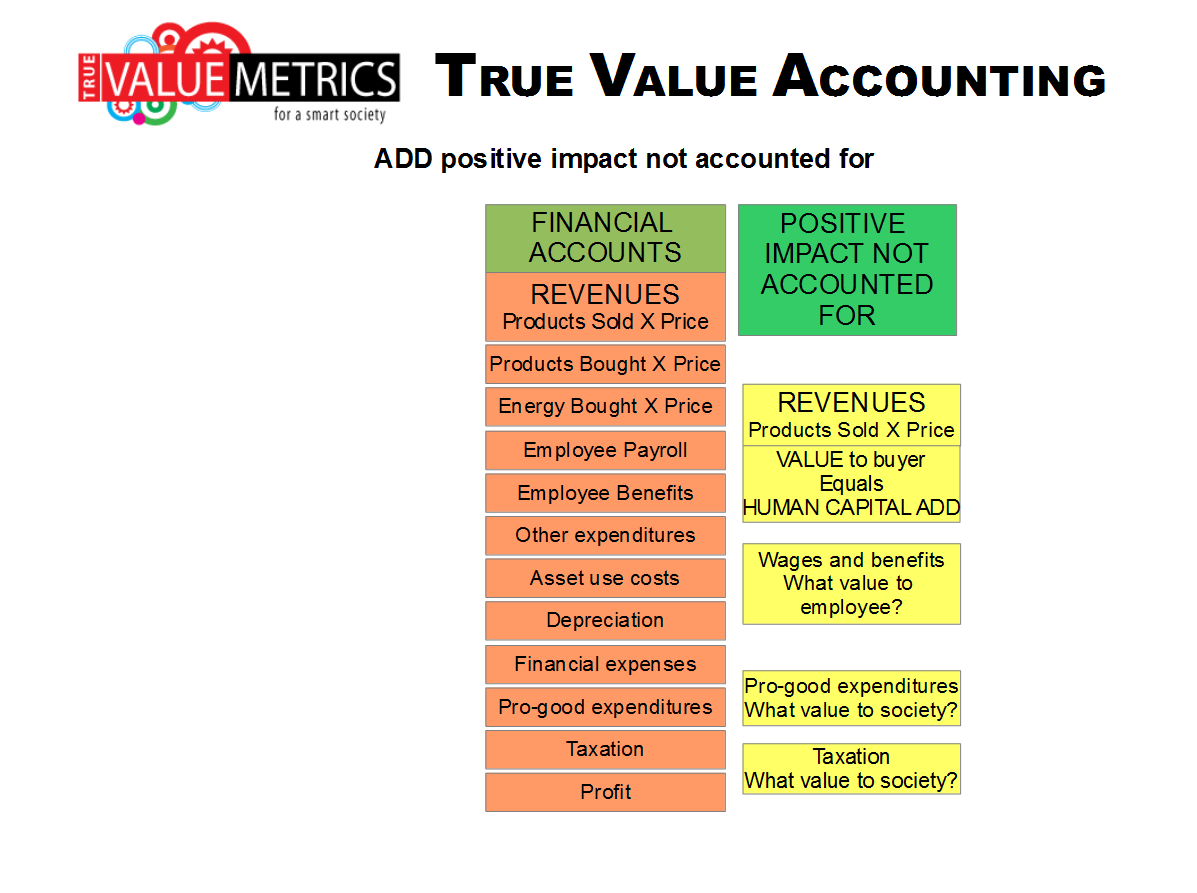

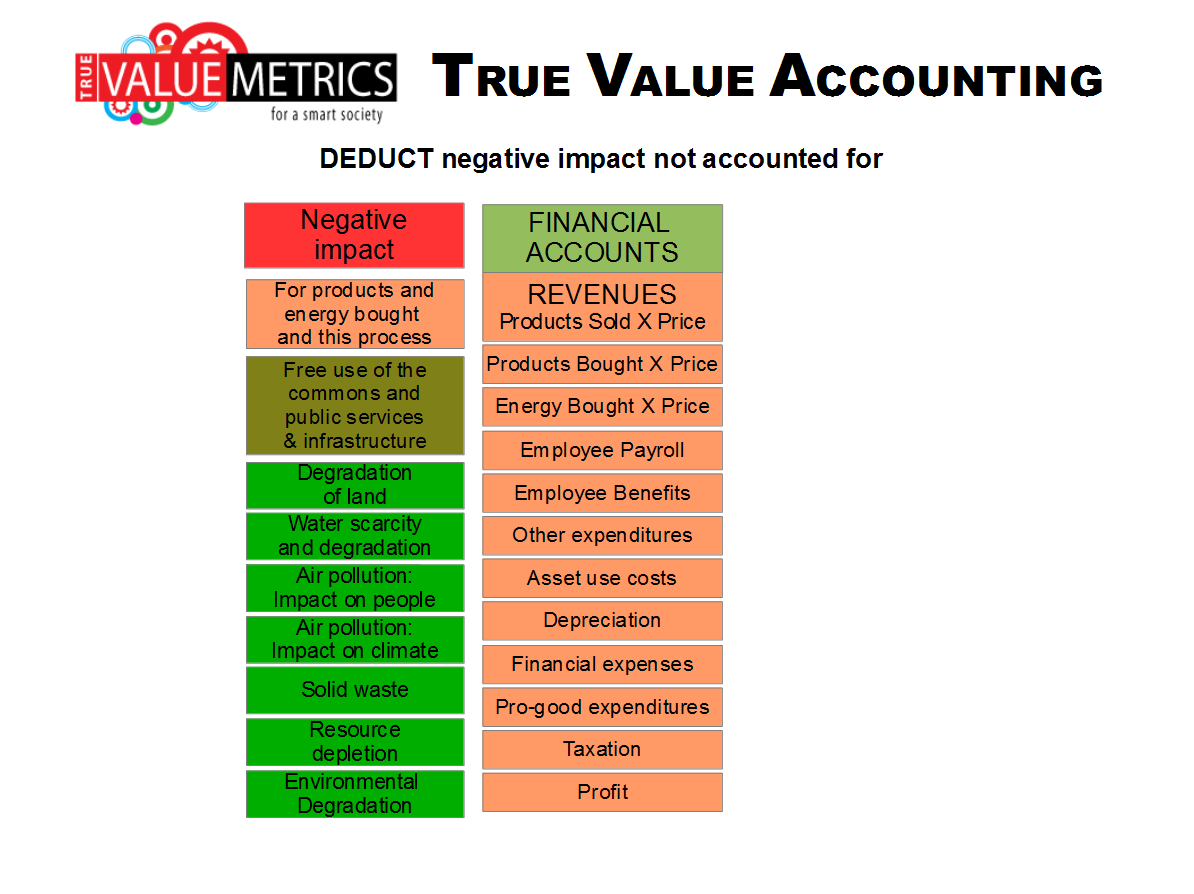

In the Financial Accounts, the Profit and Loss Account accounts for all the transactions that are denominated in money. The totals of the Profit and Loss Account document an enormous amount of important information about the activities of the organization.

The financial dimension of the transactions is enough to account for the financial profit performance, but is not enough to show the impact on everything that matters.

- There is no accounting for SOCIAL IMPACT

- There is no accounting for ENVIRONMENTAL IMPACT

There are organizations that have creating benefit for their owners as their primary and only goal. These organizations are parasites and pose an existential risk for humanity. Worse there are legal arguments especially in the United States that posit the idea that the sole responsibility of a corporate organization is to maximise the value for its owners.

Worse, most business schools have a strong curriculum to teach students how to operate a company for maximum financial performance, but few have substantial teaching about the value of a company's social impact and the cost of environmental degradation caused by a company's activities.

|

|

|

Many important companies started their lives as SOCIAL ENTERPRISES. Unilever started as a social business in the late 1800s. One can also argue that the early railways also had an important social purpose.

There are important positive impacts that arise from the operations of a business that should be accounted for ... that should be numbered.

There is a strong correlation between more consumption and a better quality of life for poor people in in poor economies. This correlation does not apply for rich people in rich economies. It is insane to argue that more and more consumption will result in better and better quality of life.

Quality of life will be improved by better quality of product ... for example: food that is as nutritious as it can be, not as profitable as it can be.

|

|

|

|