|

Why That Merrill Lynch Retirement Reversal Matters

Back when I worked at mega-companies, there were two hard-and-fast rules of PR. Rule #1 was to release bad news right before a long summer weekend, so hopefully no one would notice. And Rule #2 was to wrap everything in “this is what clients asked for” messaging.

Merrill Lynch followed both of those rules by dropping a doozy this past Thursday.

But, first, let’s back up for context. Back when it appeared that the Department of Labor would require individuals’ retirement accounts to be managed (in which investment managers are required to put clients’ interests ahead of their own), Merrill Lynch* announced that , replacing them with advisory fees. Commissions are paid every time a trade is made, and thus can arguably incent advisors to trade more. Advisory fees are charged as a percent of assets managed by the company.

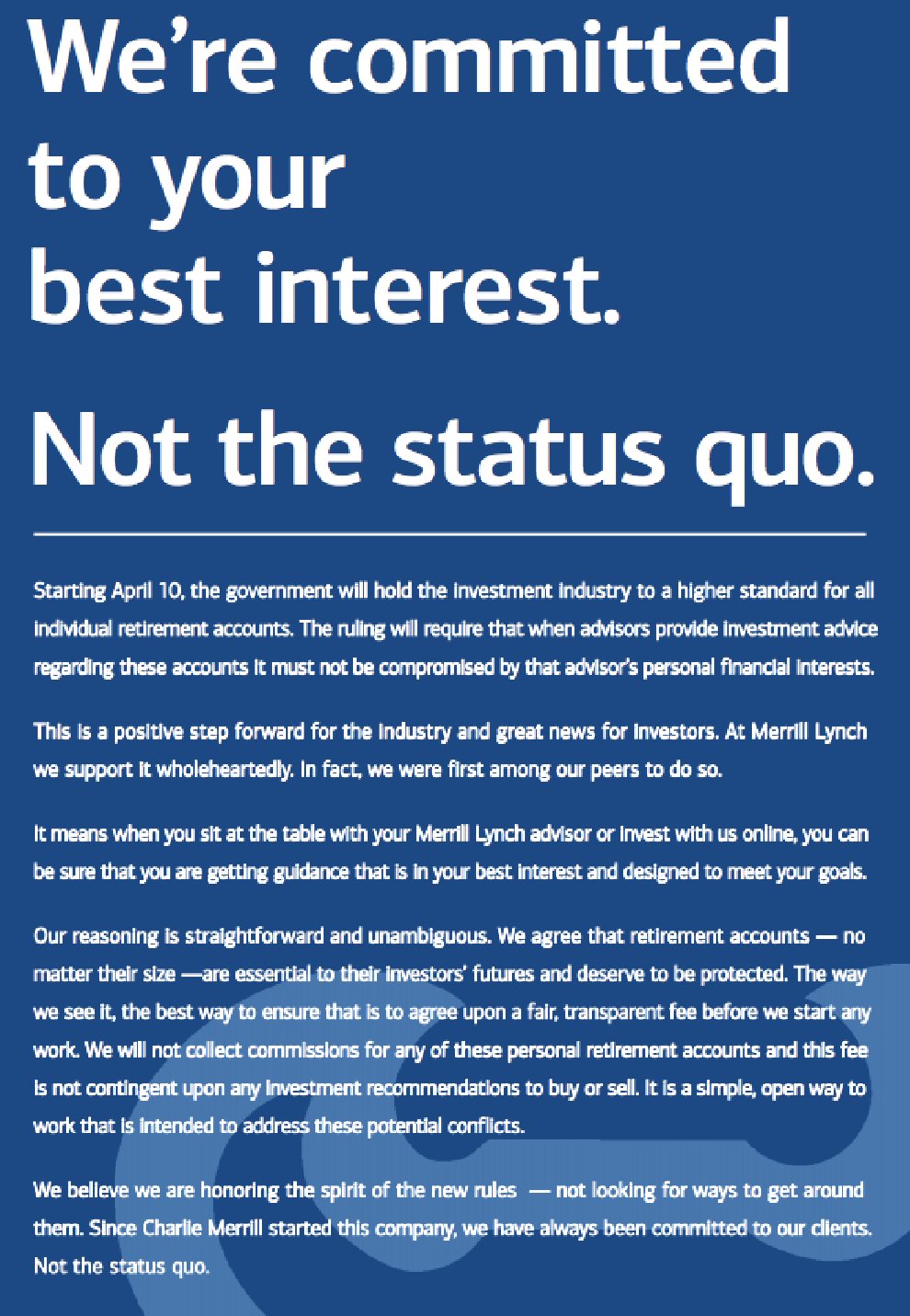

At the time, Merrill took out headlined “We’re committed to your best interest. Not the status quo” and launched (with ) trumpeting its leadership in making this change.

You’ve gotta read this newspaper ad — .

ad-01

In it, Merrill on the industry’s move to a fiduciary standard for retirement accounts:

This is a positive step forward for the industry and great news for investors. At Merrill Lynch we support it wholeheartedly.

From the same ad, on what the move means for its clients:

It means when you sit at a table with your Merrill Lynch advisor or invest with us online, you can be sure that you are getting guidance that is in your best interest ...

And on Merrill’s support of the move to a fiduciary standard:

Our reasoning is straightforward and unambiguous. We agree that retirement accounts … are essential to their investors’ futures and deserve to be protected … We will not collect any commissions for any of these personal retirement accounts … It is a simple, open way to work that is intended to address these potential conflicts.

And, for the big finale, Merrill on its stance:

We believe we are honoring the spirit of the new rules — not looking for ways to get around them. Since Charlie Merrill started this company, we have always been committed to our clients. Not the status quo.

(At Merrill, they understandably LOVE Charlie Merrill, so invoking him is always an argument ender.)

On Thursday, they essentially said, “jk.”

Under the Trump administration, the Department of Labor this past June. And last week, that it was reversing its move to ban commissions on retirement accounts. The web page, , which used to trumpet the changes with metadata on “delivering a higher standard of care” ... now shows a 404 error.

error page 2

Why should anyone care?

Because, as noted, commissions can incent financial advisors to trade more; this can be a clear conflict of interest given all of the research that . There is a (probably true) report of at Fidelity earning superior returns, theoretically because their owners weren’t trading them. There is the (definitely true) story of my calling Fidelity years ago to buy an index fund and being told by one of its representatives that it was one of their best-performing funds, again likely because it’s a set-it-and-don’t-overtrade-it fund.

Back by popular demand?

But what about Merrill’s contention, in last week’s reversal, that is what clients are asking for? I mean, shouldn’t they respond to what the clients are asking for??

Well … it’s hard to know what to ask for if you don’t have full information. And shows that 73% of individuals didn’t know how the Department of Labor rule moving to a fiduciary standard might affect their retirement accounts.

Let me ask you: Would you be able to calculate the difference in what you pay for an investment account with a commission approach vs. a fee-based plan? Would you?? Because I couldn’t. A few years ago, I tried to do something similar with my accounts at one of the big firms, to calculate how much I had paid them in the year prior. But I wasn’t able to track down and add up all of the commissions and additional fees. (I may not be able to claim that I’m the sharpest knife in the drawer, but I have spent most of my career in the industry or analyzing the industry.) I called my financial advisor at that firm to walk me through it … and he couldn’t do it either. (And this guy is one the top advisors, according to industry rankings.)

What we do at Ellevest

Regardless of which way the winds are blowing in D.C., , and thus is required to act in your best interests. We charge a set fee as a percent of your assets with us, and so we are never incentivized to over-trade your account.

And on retirement accounts: over to Ellevest, we perform an analysis of the fees you are currently paying and those you would be paying with us. And then we give you that information so that you can make an informed — a truly informed — decision about the move you are making.

We are fortunate that Ellevest is a start-up, so can build the firm we want it to be from the ground up.

*Full disclosure: This is a business I used to run.

Salliessignature

CO-FOUNDER & CEO, ELLEVEST

|