|

Does Monet Beat the Dow? How Artworks Perform as an Investment

Art can be an investment. But is it a good one?

Everyone loves a story about collectors who bought art for a song and sold it for a million. Once in a blue moon, that actually happens. In the case of Impressionist art, though, dappled landscapes and dreamy portraits by Monet, Renoir, and Degas were oftentimes considered investments before the paint on the canvas had dried.

By the 1920s, Impressionism-as-investment was so entrenched a concept that the New Yorker magazine’s Paris correspondent, Janet Flanner, could confidently write in 1926 that “with European monies and industrial values ruinously fluctuating, important modern art, if bought early and modestly rather than belatedly and dearly, is still the gilt-edged investment here.”

A work by the Impressionist painter, Edgar Degas.Photographer: EMMANUEL DUNAND/AFP

Whether that gilt has faded, though, is up for debate. Yes, in absolute dollars, the prices paid for paintings in the 1920s pale in comparison with the works’ value today. But how would they stand up to a more traditional investment such as buying blue chip stocks?

For answers, we turned to two artworks that will hit the auction block at the annual mega-sales in New York next month, then plotted their historical sale prices against the Dow Jones Industrial Average.

Caveats, First

Thanks to compilations called catalogue raisonnés, we know about every work Monet ever made. We do not, however, know for how much (or how often) all those works have sold. Because many sales in the art market are conducted privately, there is a chance (relatively small in this case, but a chance, nonetheless) that vastly higher or lower sales of works by Monet could be taking place without our knowledge.

Visitors eye paintings by Pierre Auguste Renoir, Leontine et Coco (Claude Renoir) (left) and Claude Monet, Bord de la Seine à Argenteuil, (right) at a Sotheby's exhibition in Hong Kong on Friday, Nov. 26, 2010. Photographer: Dale de la Rey

We also don’t know the circumstances in which these works’ past sales took place. Art is only as valuable as what the next person will pay for it, so if a painting came up for sale during a volatile economic period, or was sold under duress for a below-market price (as a result of divorce, death, debt, and so forth), it might have done far worse than the rest of the contemporaneous Monet market.

Finally, we have to consider the quality of the work: If a painting is ugly or a poor reflection of the artist’s style, it’s unfair to extrapolate from its performance to the artist’s broader market.

And Yet

And yet! There are always, and will always, be external factors that affect the price and performance of an artwork, and that’s the point. Knowing that there is inherent volatility to a market is not the same thing as discounting the results of that market. Whether a painting was sold on a whim or under duress, is ugly or pretty, is “good” or “bad,” probably doesn’t matter to whoever sank $65,000 dollars into a painting in 1962.

What matters, and still matters 55 years later, is whether that purchase was an act of prescience or extravagant folly.

The Paintings

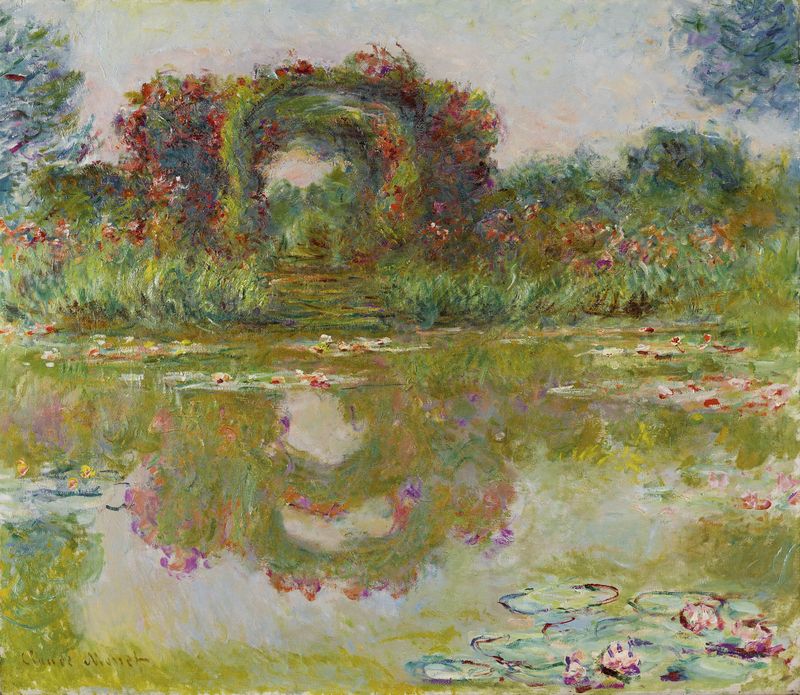

The two paintings we’ll look at are the top Monets in Sotheby’s Nov. 14 Impressionist and Modern Art sale. The first, Les Arceaux de Roses, Giverny, a three-foot-wide oil painting of a rose arbor, was painted in 1913 and offered by Monet himself for a charity auction on May 1, 1917.

Les Arceaux de Roses, Giverny, painted in 1913 by Claude Monet.Source: Sotheby’s

Its first publicly recorded sale was 45 years later at Sotheby’s, when it sold for $65,000. The buyer at that sale then turned around and sold it the same year, 1962, at Christie’s in London. It stayed in a private collection for a further 45 years, and then sold at Christie’s London in 2007 for $17.8 million. It’s on offer next month for $20 million to $30 million.

Les Glaçons, Bennecourt, painted in 1893 by Monet.Source: Sotheby’s

The second painting, Les Glaçons, Bennecourt, is an earlier, slightly larger painting of an iced-over body of water that Monet painted in 1893. It was bought and sold by five people in four years, then ended up in the hands of New York’s Havemeyer family in 1897. It stayed with them until until 1983, when it was sold for $605,000 at Sotheby’s New York. It then sold privately twice, and now it’s reappearing at auction with an estimate of $18 million to $25 million.

The Math

While Les Arceaux sold multiple times, the first publicly available record of the sale is from 1962, when it fetched $65,000.

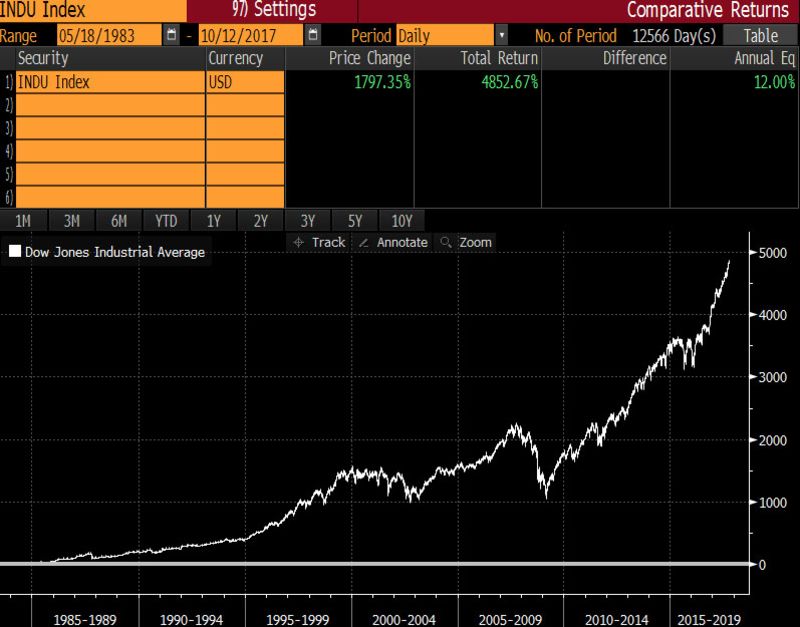

We can see that the Dow has since increased 3,097 percent on a price basis; that percentage increase from $65,000 to the present day would put the investment at about $2 million.

The Dow’s performance from 1962, when Monet’s Les Arceaux was purchased for $65,000, until now. Source: Bloomberg

But this initial calculation doesn’t take dividends into account. If we acknowledge what the Bloomberg Terminal says is the total return (the value of $65,000 if one reinvested any dividends), we come to a much higher number, 20,419 percent. Applying that to $65,000 would put us at $13.3 million. (Even this enlarged number might be conservative, given how the Bloomberg estimates total returns before 1999.) Even so, should Les Arceaux sell for its estimated $20 million to $30 million, you’d probably be better off if you had put your money in this painting than in the market.

The Dow’s performance since 2007, when Les Arceaux sold for almost $18 million.Source: Bloomberg

The second data point we have is the 2007 sale; since then, the Dow has experienced an 84.29 percent increase, which would put your total—had you invested the nearly $18 million then—at $32.8 million today. On applying the total return percentage, the number grows to $40 million. The present owner of the painting, in other words, lost at least $10 million owning art instead of putting it in an index fund.

The Dow's performance since Les Glaçons sold for $605,000 in 1983.Source: Bloomberg

For Les Glaçons, we have a single number, namely the 1983 sale for $605,000. Since then, the Dow has increased by 1,797 percent, which would make the sale price equivalent to $11.5 million today. That’s the bottom end of your result; include reinvested dividends and the total return jumps to 4,852 percent, which would bring the total to $30 million—$5 million above this painting’s high estimate.

The Takeaway

If you’d bought in 1962, you’d be doing great. If you bought after the 1980s, your returns against the Dow would be disappointing.

All this, however, leaves out one crucial component: You can’t wake up every day to admire a stock index above your dining room table.

|