|

Put Foundation Endowments to Work for ‘Total Impact’

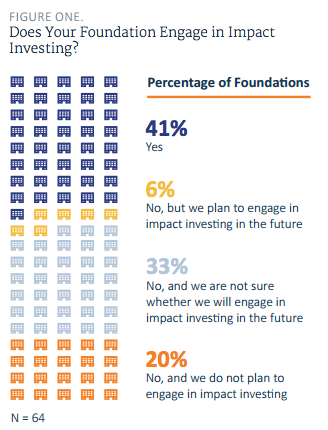

The Center for Effective Philanthropy (CEP) recently published research indicating the limited use of impact investing by US-based foundations. The report noted that such foundations are not active in impact investing because of their perception that it has minimal efficacy with respect to mission achievement and financial performance goals.

Screen Shot 2015-10-20 at 13.49.52

Source: The Center for Effective Philanthropy – Investing and Social Impact: Practices of Private Foundations, 2015.

At Sonen Capital, we are deeply concerned by these views and believe that certain misconceptions and dated thinking drove the results of the research. In fact, we believe that capital markets can and should help solve the world’s pressing environmental and social issues while at the same time deliver market-based financial performance. For foundations in particular, impact-oriented investment portfolios have enormous potential to amplify philanthropic programming and grant making.

Too frequently foundations invest at cross-purposes by investing their corpus in ways that are not consistent with their own charitable goals and missions. Foundations should begin to consider the full potential of their investment portfolios to maximize the effectiveness of their work, and take into account the considerable potential of their endowment in helping create positive social and environmental impact.

Baby Steps

CEP’s survey revealed that while 40% of foundation respondents participate in impact investing, they do so with a very small percentage of their endowment or grant budgets. Key findings in the survey reveal that:

... The rhetoric about aligning mission impact and corpus investing has far outpaced the reality of this practice;

... Given concerns around return implications, the ‘overwhelming’ majority of foundations continue to participate in investments that may ben antithetical to their organizations’ social purpose; and

... Fiduciary responsibility is interpreted so strictly that it becomes an impediment to aligning overall investment policy with mission, values and program goals.

In this piece, we seek to deconstruct the beliefs revealed by CEP’s survey, hoping to shed some light on the misconceptions that have delayed adoption of impact investing. These misconceptions can be segmented as follows:

... Impact investing will not help the foundation achieve its goals. Rather, grants made possible through financial returns from conventional investing are a more effective means to achieve social or environmental goals.

... As a result of financial returns being the priority and focus in endowment investment practices, any infusion of social or environmental purpose in investment management may compromise these financial returns.

... Foundation staff does not have the right expertise, skills or staff to engage in impact investing.

Goal Achievement and Measuring Impact

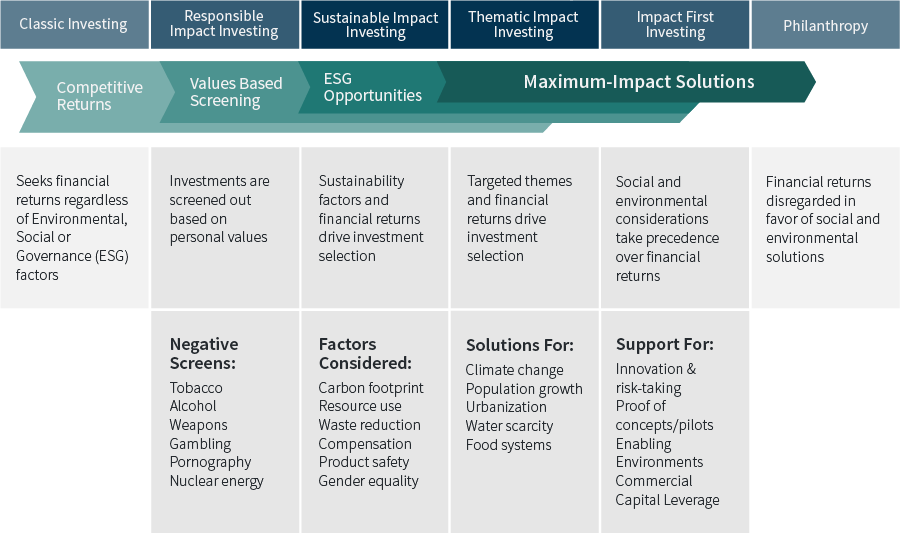

The rapidly growing impact investment industry now offers multiple different solutions for investors, ranging from simply excluding businesses or industries that are working in opposition to a particular social mission, to portfolio-wide, impact-driven strategies oriented to specific impact themes across all asset classes. In helping this industry grow and clients to understand the benefits of impact investment strategies, Sonen has built an evaluation framework that can help identify how impact is created and how it is expressed across asset classes.

Impact investing takes a variety of forms. Sonen views it within a spectrum that has classic investing, which emphasizes profit maximization without regard to the problems such profits may help create on one end, and by philanthropy, which focuses exclusively on positive impact creation without regard for financial performance on the other. Between these two lies the world of impact investing, as noted below.

Responsible investing removes businesses or industries altogether, essentially avoiding negative impact.

Sustainable investing integrates Environmental, Social or Governance (ESG) considerations into investment decisions and can increasingly reflect specific E, S or G issue areas of concern to investors.

Thematic investing focuses on goods or services that explicitly address a social or environmental need, such as resource scarcity, water or climate change.

Impact first investing prioritizes impact creation over financial performance, and includes foundation tools such as below-market Program Related Investments (PRIs).

Impact Investing Spectrum

Sonen - Methodology Chart-01

Impact investing can include any combination of these investment approaches and is applicable across all asset classes.

As more measurement methodologies emerge, and more non-financial data becomes available, investors have ever-greater ability to align financial resources with socially-minded worldviews. An accessible first step for many investors is to conduct a portfolio assessment to determine if any specific investments are directly contrary to personal or institutional objectives. (See Case Study below)

It is important to note that as asset classes and impact approaches vary, so too do the type, scale and measurability of impact creation. Sonen has developed a proprietary measurement system called AIMS that seeks to capture these subtleties, taking into account:

... Additionality – the incremental impact that results from an investment;

... Intentionality – the conscious decision to create positive social or environmental impact, on the part of the investor or the investee;

... Measurability – the ability to quantify the level of impact creation, which varies significantly between asset classes; and

... Scale – the amount and reach of impact created.

By applying the AIMS framework investors gain greater understanding of the intrinsic and potential impact of any given investment, and ultimately help align investment portfolios with specific impact objectives.

Financial and Fiduciary Standards

We strongly believe that sustainability-minded investment requires no financial compromise. Indeed, Sonen’s investment strategies have exceeded their conventional, non-sustainable, benchmarks, net-of-fees since inception.[1]

Our own demonstration that impact investing is not compromise performance is buttressed by further empirical evidence that shows sustainability-minded investing does not necessarily result in financial compromise (barring the financial risks that are inherent in any investing). For example, the September 2014 CDP “Climate Action and Profitability” study illustrates that active integration of sustainability practices into business strategies results in outperformance compared to those companies that fail to show such integration[2]. CDP’s research provides evidence that companies that manage carbon emissions benefit from 18% higher returns on equity than companies that don’t manage such emissions.[3] Further, a meta-study of similar research on sustainability and financial performance reveals that companies with strong sustainability scores show better operational performance, and “investment strategies that incorporate ESG issues outperform comparable non-ESG strategies.”[4]

The notion that impact investing violates a fiduciary duty is misplaced. As mentioned above, impact investing is not necessarily performance concessionary. Additionally, and perhaps more importantly, ignoring ESG factors within the investment decision-making process itself could be considered a breach of fiduciary duty. As sustainability becomes increasingly more important for business success, as part of prudent investing investors have a duty to include sustainability into the investment decision-making process. Indeed, if fiduciary duty is defined as an obligation to enhance financial performance, the failure to integrate sustainability into investment analysis would also conflict with the performance of that duty, by ignoring the risk-adjusted performance of assets over the medium to long term.

This view was recently confirmed by the U.S. Department of Labor on Oct. 21 when it reversed a 2008 guidance that discouraged retirement plan fiduciaries and their investment advisers from considering environmental, social and governance factors when choosing investments for their portfolios. The reversal, made through a new interpretive bulletin that reinstates a 1994 guidance, recognizes a growing consensus that fiduciary duty may in fact require fiduciaries to look at these aspects to protect plan participants’ retirement accounts from undue risk.

Foundations interested in addressing climate change have multiple opportunities to align assets with such mission AND to evaluate success. Investors can scrutinize the carbon emissions of entire portfolios, evaluate companies’ efforts to reduce emissions, invest in clean energy opportunities, and engage directly with companies to improve related sustainability practices.

Foundations would do well to consider impact investing as an additional tool that can amplify their mission, and that investment policies embodying the active pursuit of positive, aligned impact ultimately will be additive to grant making and regular philanthropic programming.

Organizational Capacity

It is true that at times professional foundation staff does not always have the requisite investment expertise to implement a successful impact investment strategy. However, through greater efficiencies and cooperation within the broader foundation staff, we believe that this shortfall can be overcome. For example, staff typically provides strong content expertise on particular social or environmental issues. However, foundation staff that has such expertise is often separated from the investment professionals that manage the endowment – indeed it is rare that there is any interaction between program staff and investment managers. This remains true despite the fact that regardless of functional responsibility, the goals of their work – to support the mission of the organization – are shared.

Without increasing the responsibilities of programmatic staff a number of steps might be taken which would allow foundations to increase the positive impacts of their investment portfolios. Significant improvements in mission alignment can occur by encouraging the sharing and communication of internal resources and knowledge. This could include the participation of a program staff member on the investment committee as well as the integration of explicit language around the foundation’s mission into the Investment Policy Statement, the investment guidance document directing the institution’s investment management. Foundations may also ask their investment managers to proactively seek investment opportunities that fit within a broad set of guidelines that ensure greater alignment between programming and endowment investing.

Foundation Investments Often Work at Cross Purposes to Mission

It is not difficult to identify some of the stark inconsistencies between foundations’ social purpose and their investment portfolio. In some cases, the investments themselves are increasing the social or environmental problems that the foundations are actually trying to solve.

For example, one $30 million foundation’s focus is on the conservation of natural resources, with additional focus areas in marine conservation, and environmental initiatives. However, holdings in its investment portfolio include Schlumberger (the world’s largest oilfield services company) and National Fuel Gas (a company with sizeable natural gas exploration activities). A foundation with an environmental focus would be better served by focusing its investments on producing environmental outcomes, rather than investing in the companies that are creating the problems that the foundation seeks to address.

In another stark example, consider a national organization, funded by a half dozen of the country’s largest philanthropies that is dedicated to “solving the childhood obesity crisis.” One of the funders, with net assets over $3 billion, maintains investments in Coca Cola, PepsiCo, Nestle, and Mondelez (think Oreos). Investing in these organizations while at the same time addressing child obesity simply makes no sense.

Conclusion

There is a clear growing velocity of financial resources being invested with social and environmental sensibilities, up $10billion from 2013-2014 and projected to increase by another 16% in 2015 (GIIN, JP Morgan). There is also a growing awareness that we can no longer divorce our investment practices from our individual or institutional view of the world. Momentum is building around divestment campaigns (e.g. fossil fuels), and organizations such as Responsible Endowment Coalition, that evidences this growing awareness and desire for portfolio alignment.

Impact investing is an extraordinary opportunity for foundation’s to amplify the impact of their good work by integrating their investments with their missions. Foundations should focus not only on assessing the impact of their grant making but also on their total impact, which includes their endowment, where the vast majority of their assets lie and where positive and negative business externalities occur at large scale.

=========================================================================

[1] Through Q2 2015; Sonen Capital

[2] https://www.cdp.net/CDPResults/CDP-SP500-leaders-report-2014.pdf

[3] ibid

[4] From the Stockholder to the Stakeholder: How Sustainability can Drive Outperformance; University of Oxford and Arabesque Partners; March 2015; page 10

|