|

Winning the Game! What Game?

More and more … of what?

So much of modern progress has merely been doing more and more of what, arguable, the world neither wants or needs. A huge effort has been expended in trying to create wants and needs … for not good reason.

The world has achieved an amazing capacity to produce … something never achieved before at any time in human history, but the metrics about socio-economics are pushing for production of all the wrong things … for things that produce profit and rarely if at all those things that would satisfy needs … be valuable, without being profitable.

The prevailing metrics are wrong most of the time, something that is terribly dangerous for the future of humankind andf the p[lanet.

Maximizing quality of life

In the money metrics construct winning is more and more of money and material goods … with quality of life assumed to improve with more and more of these things.

Keeping Score

In sports, scorekeepers keep score and the score tells which team it is that wins. Society is similar … with the present money metrics system of scoring, winning is about more and more money. In a value based society winning will be maximizing quality of life … the values that make life worth living.

In TVM, progress is like winning the game. It is maximizing quality of life. This is not a money construct but a value construct.

TVM is a way more complete system of metrics than conventional money accounting. Conventional accounting coherent and very powerful. It has stood the test of time, but has changed rather little since it was devised in its modern form more than 400 years ago.

In TVM, progress … maximizing the quality of life … has a central role for society, just as profit has a central role for the business entity.

Progress Is Balance Sheet Change

Corporate business accounting has well defined ways of computing profit for business. This definition of profit by Lord Benson over 60 years ago is very simple!

In the 1950s, Henry Benson … a senior managing partner at Cooper Brothers in the UK was asked while testifying in a British High Court to define profit. After a short moment of reflection he replied “My Lord, a profit is the difference between two balance sheets”

Henry Benson subsequently became Sir Henry Benson and later on Lord Benson. Cooper Brothers combined with Lybrand, Ross Bros and Montgomery of the United States to form the international firm of Coopers and Lybrand which in turn became a part of PriceWaterhouseCoopers PLC (The author trained with Cooper Brothers & Co in the 1960s!)

This definition is one of the most elegant definitions about anything anywhere. It is such a contrast to the way profit gets defined in law and regulation … and the FASB standards and IASB standards, where different rules can be applied in a variety of different circumstances, and in the end, there is no certainty about anything.

How change in state shows progress

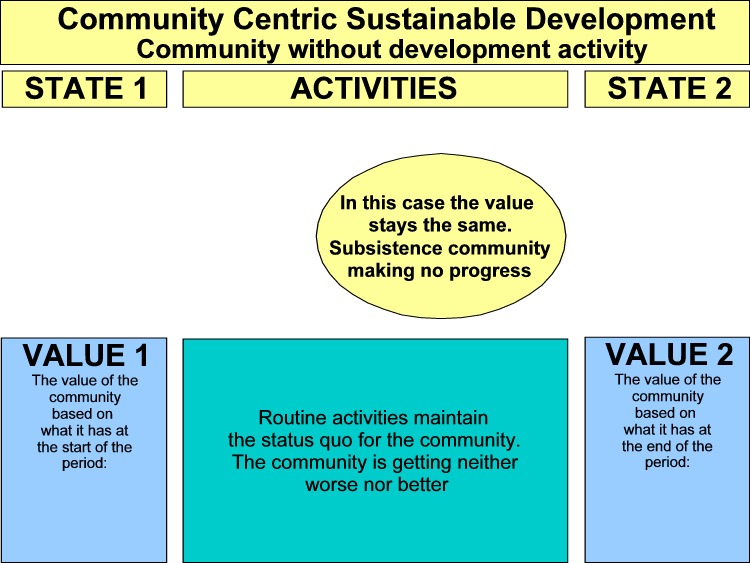

Simple balance sheet … the steady state situation

In this image, the value of the reporting entity (in this case, a community) is the same at the end of a period as it was at the beginning ... ordinary daily activities produce what is consumed ... it is a stable steady state situation.

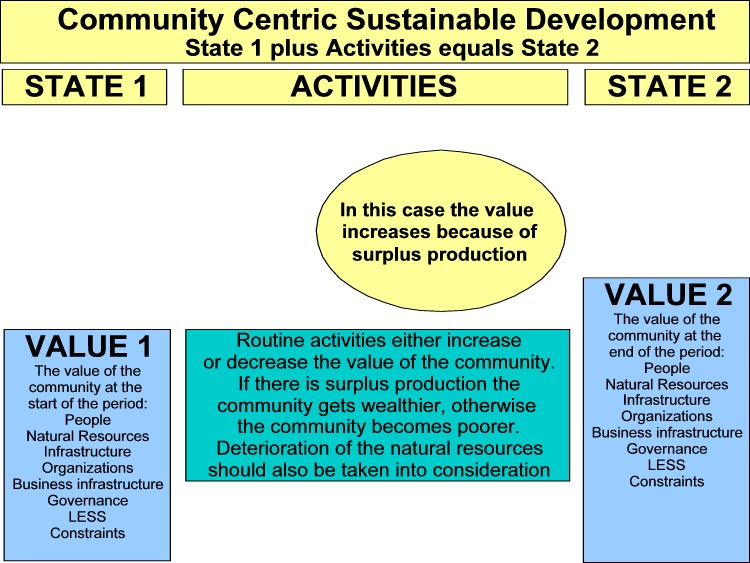

Balance sheet progress

The steady state situation is unusual. What is normal is either progress or regression. In this next case the value of the community is more at the end of a period than at the beginning of the period ... ordinary daily activities produce more than is consumed.

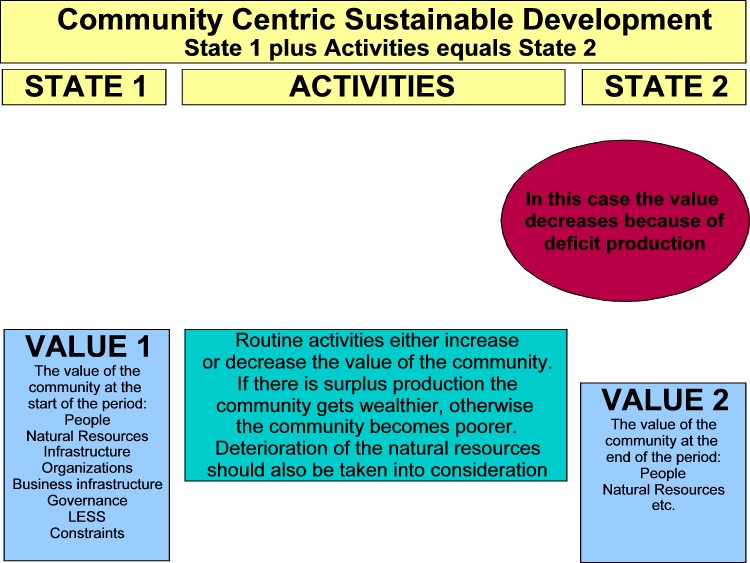

Balance sheet regression

In this last case the value of the community is the less at the end of a period than at the beginning of the period ... a problem because activities produce less than are consumed.

Progress … incremental value over time

Progress is incremental value … that is improved quality of life … improved social value that makes quality of life better.

Socio-economic value progress is one of the core metrics for a smart society … yet almost absent from the money related metrics used by the corporate community, capital markets and the broader society at the present time.

TVM has a community focus treating the community as the reporting entity. The rules for consolidating accounts apply as all the subsidiary units doing economic activities in the community are brought into account. TVM includes transactions that reflect value as well as the normal money transactions.

TVM is more accountancy than a statistical construct. The data are as simple as possible ... the transactions as small as possible, as many as possible and as clear as possible. Some of the value of TVM derives from how TVM can do accounting for community progress. In the following graphic ... the value of the community at the beginning of the period is the same as it is at the end of the period ... the community has gone about its business for the period, the time has gone by, but nothing has changed.

Data about the daily activities is not needed in the TVM system in order to be very clear about progress ... whether it is progress or problem. All that is needed is data about the value changes that have taken place from the beginning of the period to the end of the period as shown below.

Progress is about an improving quality of life … it is not merely having more profit or more growth, though these may be part of the assessment. In the TVM methodology the primary measure of progress is the value increment accruing to a society … the net of value consumed in the period and the value created during the period taking into consideration all the activities of the community. The framework for quantifying value transactions have some similarities with those of business accounting.

The three key datapoints in TVM are cost, price and value. Value is the key datapoint in measuring progress or problem. Cost is a function of and derivative of productivity and important in the analysis of activities. Price is important in money accounting and how value creation is allocated to different groups.

While value is important, it is also a complex datapoint because there may be an unlimited number of views of what the unit or measure of value is for any specific element. This has been embraced for some years now by capital markets as they have created more and more complex financial instruments ... maybe not all of them proving to have substance ... but the basic idea also works for TVM value, and in the case of TVM it has been combined also with standards also drawn from traditional corporate accounting. TVM refers to the unit of value as the CVU ... Common Value Unit. More than anything else, however, TVM is designed to be very practical, very simple, very low cost and very valuable.

Activity Produces Progress

Which changes the balance sheet

Resources are consumed

TVM considers activity as an event that consumes resources and creates outputs like goods, services and happiness. Where value creation exceeds value consumption there is value adding, otherwise value destruction.

TVM treats the period value adding aspect of economic activity in the balance sheet in exactly the same way that period profit is treated in a business balance sheet. The profit of business is the net of changes in all the assets and liabilities of the business balance sheet. Similarly the value adding of economic activities changes the value balance sheet.

The balance sheet concept applies at the level of the activity or of the community. The value balance sheet may be used also for organizations and for individuals or families. The most useful for the “management” and oversight of society and socio-economic performance is, however, the balance sheet of the community.

Value is created

When a resource is consumed in some activity, something is done. It is of interest to know what is done, but normally the objective is not to do something but to have something of value be created. Metrics about the amount of activity in relation to the resources used enables the calculation of cost efficiency … but it is the production of value that is more important and enables the calculation of cost effectiveness.

Where value creation exceeds the value consumption there is value adding … otherwise there is value destruction.

Value adding or destruction impacts balance sheet

Value adding or destruction impacts the balance sheet … the balance sheet of the activity and the balance sheet of the community.

A community balance sheet that incorporates elements of quality of life will change when value adding or value destruction activities take place in the community.

It should be noted that “off balance sheet” transactions are as wrong in TVM value accounting as they are in corporate accounting. The value balance sheet for a community is affected by all socio-economic activities that relate to the community.

Profit versus Value

A value balance sheet for a community that is host to large scale minerals extraction will quantify what it is losing in natural resource value compared to what the community is gaining in value such as employment and perhaps assistance with infrastructure, education, health, etc. TVM value chain analysis and value accounting relative to the business organization may indicate that the profit for the organization is substantial while there is offsetting value destruction for the community.

How can this be? And the answer is that business money profit accounting keeps value “off the balance sheet”! It can be argued that not having value metrics is important to the modern corporate community!

Intangible activity has impact

Policy improvement

There are many intangible activities that can change the value balance sheet of a community … and change it significantly and rapidly.

Impact of Policy Improvement

For example, improvement in the policy framework that expands economic opportunity changes the “value” of many of the community value assets associated with people. TVM enables the dynamic of exponential change to be recorded and be a part of the accountability of decision making.

Improvement in the way decisions are made about allocation of resources to value adding activities changes the value balance sheet. TVM makes explicit the relationship between tangible and intangible activities and value change even though these matters are not linear but multiple sets of complex exponential multipliers.

Security … crime

Security changes a lot … the value of security is high based on all the economic opportunity that exists when there is compared to when there is not. People need security in order to go about their daily lives and engage in socio-economic activities. A high crime neighborhood is associated with a poor quality of life!

Job opportunities

The “value” of a person is diminished when there are no job opportunities where a person may used their skills.

Organization

A place may have people and resources but nothing gets done and there is no progress. This is because there is no capacity for organization. Putting in place an framework of organization adds value to the community and enables resources to be used effectively to create the value for progress.

|