|

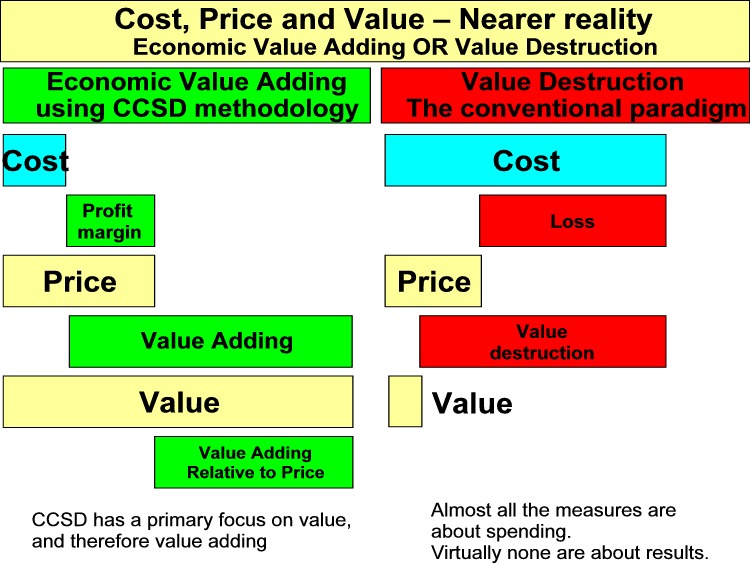

There are three key numbers: cost, price and value. Of these, value is the most important and the focus of TVM value accountancy.

Value is the key datapoint in measuring progress or identifing a problem. Cost is a function of and derivative of productivity and important in the analysis of activities. Price is important in money accounting and how value creation is allocated to different groups.

Cost, price and value are very important numbers about any economic activity. There is a substantial amoung of information about price and to some degree about profit, but very little easily accessible data about cost and value. Every store prices its merchandise and there is minute be minute reporting of the prices of commodities, stocks and other financial instruments that are trading at on exchanges. There is nothing like this for data about costs ... and even less organized data about value.

Corporate accountancy is only about money cost and money price. TVM uses cost, price and value. Cost, price and value are the three key numbers that describe economic activity. The relationship between these numbers determines the performance of almost any economic activity. All of these measures are important ... any one missing and the understanding of the dynamic of societal progress is compromised.

Value. While value is important, it is also complex because there may be an unlimited number of views of what the unit or measure of value is for any specific element.

Interestingly the capital markets have been able to value complex financial instruments simply by the process of trading them. Their value is what a buyer is prepared to buy them for and a seller is willing to sell them for. This worked ... up to a point ... in capital markets as they have created more and more complex financial instruments.

The same basic idea works for value in TVM value accountancy. Within the TVM framework there can be many different value elements which get a standard value within the system using a unit of value which may be referred to as a Common Value Unit of CVU. Standards are similar to standards in cost accountancy.

Though this may sound complicated, in fact, TVM is designed to be very practical, very simple, very low cost and most important, very valuable and cost effective.

Cost and price. Cost and price make it possible to calculate margins and profits ... and this is what is done in normal corporate accountancy and financial reporting. As we shall see later, in modern financial reporting both cost and price are capable of being distorted so that the most favorable margins and profits are being reported ... something that professional accountancy was structured to avoid.

Cost and value. Cost and value make it possible to calculate value adding ... something that is very important for society. For this to be of greatest use, the calculation of cost must include not only the money cost but also the value consumed associated with the activity.

Price and value. In some cases price and value are the same. In this situation the value chain through delivery to the final consumer is extracting from the consumer a price that is equivalent to the value. The consumer does not get anything of the added value. In fact the typical business model is one that aims to extract as much revenue from the market as possible.

UNDERSTANDING COST AND VALUE BEHAVIOR

COST, PRICE AND VALUE

Price has an important role in the matter of economic incentive ... and the question of sustainability.

The value chain works and is efficient when the transfer pricing through the value chain provides a reasonable

rate of return on capital employed within each piece of the value chain. If any of the links in the chain

become unprofitable, the value chain becomes dysfunctional.

HOW PRICE IMPACTS COMMUNITY

Price is a key variable in the performance of society. It is not as important as cost, but the way price is

used in society determines the way value is shared between the various economic actors. The following

graphic shows how an economic transactions that has costs and value is shared between the enterprise and

the client depending on the price being applied to the transaction.

For society as a whole the value adding is the difference between the value and the cost. For the client the

value adding is what is left of value adding after the enterprise has taken out its profit. In the profit

maximizing enterprise the goal is to have profit as much as possible, and the amount left in the hands of

the client is of little consequence.

Base Case

In a lower cost case the enterprise profit increases at the same price point ... and the amount of value

derived by the client stays the same.

Lower Cost Case

If the client and the enterprise are in the same community it does not matter so much whether the client or

the enterprise has what share of the value added ... but where the enterprise is from outside the

community it matters a lot. In the case where the enterprise is external ... the case of Foreign Direct

Investment (FDI) for example ... the value adding for the community is small because the profit leaves the

community. If the costs are incurred in the community there is some multiplier effect ... but typically local

disbursements are small and most of the costs, as for example in mining are equipment, fuel, expatriate

payroll .... with rather little value for the community.

The External Enterprise Case

|