|

Relief and development industry

In the relief and development industry, there is but the skimpiest of knowledge and understanding of costs

and the links between costs, activities and impact on society. The over-riding reason for this is that the

incentives in the sector have little or nothing to do with costs and productivity. There are few, if any

systems that have been institutionalized that have either of these parameters as a core interest.

The recurrent costs arising from development projects

I remember being asked to prepare a report (in East Africa) about the recurrent costs

arising from internationally funded development projects. This struck me as a silly

question because in my corporate career all the investments were oriented to

reducing recurrent or operating costs and increasing productivity. What was going

on?

It turned out that very little of the international portfolio of assistance had any focus

on cost and productivity ... the phrase “capacity building” was commonplace ... and

in practice this covered the spending of money on almost anything a consulting firm

wanted, and long term sustainability was totally dependent on the local government

funding something in perpetuity.

Typically the government had these capacity building projects high priority for

external funding and zero priority when own money had to be used!

There are many, many reasons for very weak cost accounting in the relief and development industry. One

of these is that most activities are funded through donors under some agreement that limits the amount of

“overhead cost” that will be reimbursed ... and in turn this limits the quality of the accounting and again

in turn this limits the understanding of project performance and costs.

If the development industry had cost accounting that showed what worked and what did not ... there

would be a much clearer basis for decision making. At the moment the modus operandi seems to have all

of the characteristics of “blind man's bluff”.

The key is to get data about history that can be used to build understanding that is useful ... practical ...

and not merely academically rigorous.

Project impact ... project design

I have taken part in hundreds, if not thousands of project evaluations. The cost was

always substantial ... and mostly the impact was negligible ... and in some cases quite

detrimental. But that was hardly ever the subject of the evaluation.

The solution to having negative evaluation is simple ... include in the project design

very limited goals ... and then measure performance against these tiny goals. Then,

relative to the tiny goals, the project will be performing well. Make sure that the TOR

for evaluation is to assess the project performance against the project goals.

Never mind that the money involved should have been able to do much more. This

issue is not to be addressed. The money has been approved, and the question is

simply whether or not the goals were achieved or not.

Many of the projects have cost a lot ... and done very little. A community of

development experts is happy ... but development has not progressed.

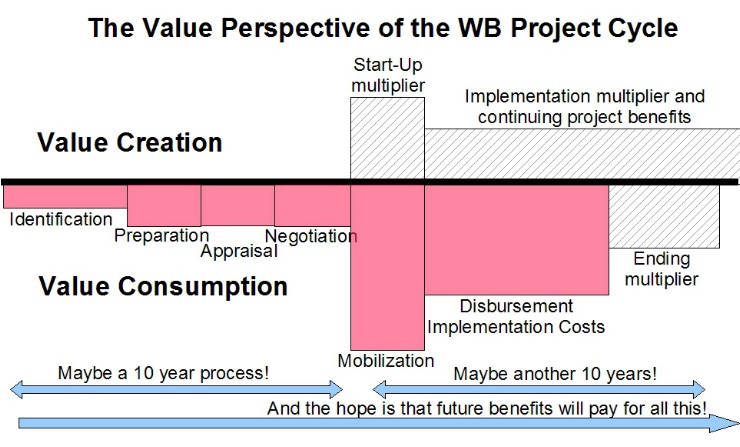

Value change during the project cycle

The World Bank project cycle is an example of the value chain. In this case the value chain is over time, rather than between organizations and places. This is ilklustrated in the following graphic:

Timeline of costs and values

The following graphic shows the very different timeline for incurring costs and realizing values. This is a critical problem in development and not central to much of the development planning process that is practiced.

As a practical matter most of the cost have been incurred before it can be shown that there are any benefits ... and this provides a dangerous opportunity for costs to be misused long before the lack of benefit raises questions about performance.

The timeline of a typical “development” project shows changes in value starting with value consumption

as the project is prepared and starts implementation, followed by value benefits as the project continues.

For big World Bank type projects the length of time is significant and the scale substantial ... with the

costs of value consumption certain and the benefits much less certain. When the benefits do not

materialize, the project creates massive value destruction ... and for many if not most World Bank

projects this is the sad reality.

TVM Value Accountancy looks at any and all economic activities from the perspective of value creation

and value consumption. The problem with the World Bank project cycle is that there is substantial value

consumption that is 'for sure', and long term benefit that is uncertain. The graphic shows that costs are incurred over a long time before a project is implemented. When a World Bank project does not generate the expected benefits there is a long term loan repayment cash flow that keeps the project in a value consuming mode for many years.

The real world situation may be worse than the theoretical situation, since the costs are certain and in real money and now, while the benefits are social and not very tangible nor certain and in the future. Most of the benefits of typical World Bank projects do not produce cash benefit flows, but they do require financial interest and repayment in very tangible hard currency.

While this is obviously terribly bad for the community and the economy that serves the citizenry, this is

less bad for those that have enriched themselves at various stages of the project ... no matter that the

project is an economic disaster over the long term.

|