BURGESS POWERPOINT

TEDxUWS - UpperWestSide

Peter Burgess ... April 26, 2016

|

|

|

TEDxUWS - UpperWestSide ... April 26, 2016

https://www.slideshare.net/PeterBurgess2/tva-p3-draft-ea

|

Open external link

|

|

INCOMPLETE ... EDIT IN PROGRESS

|

Published on Apr 26, 2016

1.

TEDxUWS Slideset for Peter Burgess talk at TEDxUpperWestSide on April 26, 2016 File: TVA-p3-DRAFT-Ea-160425.odp Peter Burgess (c) All rights reserved

2. BE THE CHANGE

'BE THE CHANGE THAT YOU WISH TO SEE IN THE WORLD' - GANDHI featuring talks on ART + SCIENCE + INTEGRITY + FOCUS

3.

Complex system … competing agendas

4-12.

I WILL ANCHOR MY REMARKS AROUND THE LETTER P

13.

Complex system … competing agendas

15. Peter Drucker, a well known management guru famously said: “You can't manage what you don't measure”

16.

17.

18.

19.

20.

21.

22.

23.

24.

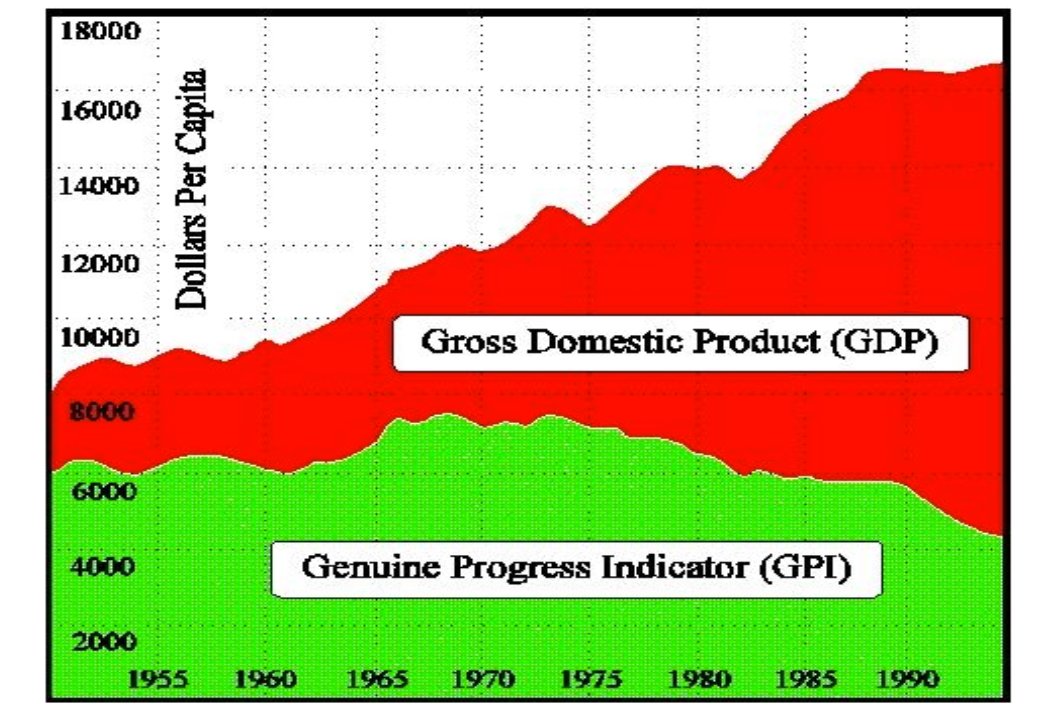

25. TRUE VALUE ACCOUNTING

26. MULTI DIMENSION IMPACT ACCOUNTING

27. TRUE VALUE ACCOUNTING

28. MULTI DIMENSION IMPACT ACCOUNTING COMPONENTS OF US MONEY SUPPLY

29. MULTI DIMENSION IMPACT ACCOUNTING US FEDERAL RESERVE ASSETS

30. MULTI DIMENSION IMPACT ACCOUNTING

31. TRUE VALUE ACCOUNTING

32. Complex system … competing agendas TRUE VALUE ACCOUNTING

33. The Phillips Machine – MONIAC – at Cambridge TRUE VALUE ACCOUNTING

34. TRUE VALUE ACCOUNTING

35. TRUE VALUE ACCOUNTING

36. TRUE VALUE ACCOUNTING

37. TRUE VALUE ACCOUNTING

38. TRUE VALUE ACCOUNTING

39. TRUE VALUE ACCOUNTING

40. TRUE VALUE ACCOUNTING

41. TRUE VALUE ACCOUNTING

42. TRUE VALUE ACCOUNTING

43. Complex system … competing agendas TRUE VALUE ACCOUNTING

44. TRUE VALUE ACCOUNTING

45. STEADY STATE TRUE VALUE ACCOUNTING

46. POSITIVE PROGRESS TRUE VALUE ACCOUNTING

47. DETERIORATION OF STATE TRUE VALUE ACCOUNTING

48. TRUE VALUE ACCOUNTING

49. YELLOW: The PEOPLE piece … Human Capital (HC) DIRTY BROWN: The ECONOMIC piece … Man Built Capital (MBC) GREEN: NATURE, ENVIRONMENT … Natural Capital (NC) COLOR KEY

50.

51.

52.

53.

54.

55.

56.

Fundamentals of the Socio-Enviro-Economic System Human Capital Man Built Capital Natural Capital

57.

Period 1 2 3 4 5 6 7 8 9 10 11 12 HC MBC NC TRUE VALUE ACCOUNTING HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC

58.

Period 1 2 3 4 5 6 7 8 9 10 11 12 HC MBC NC TRUE VALUE ACCOUNTING HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC HC MBC NC

59.

Complex system … competing agendas TRUE VALUE ACCOUNTING

60.

Fundamentals of the Socio-Enviro-Economic System Human Capital Man Built Capital Natural Capital Hum an Capital Man Built Capital Natural Capital TRUE VALUE ACCOUNTING

61.

Fundamentals of the Socio-Enviro-Economic System Human Capital Man Built Capital Natural Capital TRUE VALUE ACCOUNTING

62.

Fundamentals of the Socio-Enviro-Economic System Financial Capital Human Capital Man Built Capital Natural Capital Man Built Capital Natural Capital Human Capital Split out Financial Capital from other components of Man Built Capital TRUE VALUE ACCOUNTING

63.

Fundamentals of the Socio-Enviro-Economic System Financial Capital Human Capital Man Built Capital Natural Capital SunSun Man Built Capital Natural Capital Sun Human Capital Add Sun … the source of all energy Split out Financial Capital from other components of Man Built Capital TRUE VALUE ACCOUNTING

64.

Fundamentals of the Socio-Enviro-Economic System Financial Capital Human Capital Man Built Capital Natural Capital SunSun Financial Capital Human Capital Man Built Capital Natural Capital SunSunSun Man Built Capital Natural Capital Sun Human Capital Add Sun … the source of all energy Split out Financial Capital from other components of Man Built Capital Reorder because Financial Capital metrics exist TRUE VALUE ACCOUNTING

65.

66.

67.

68.

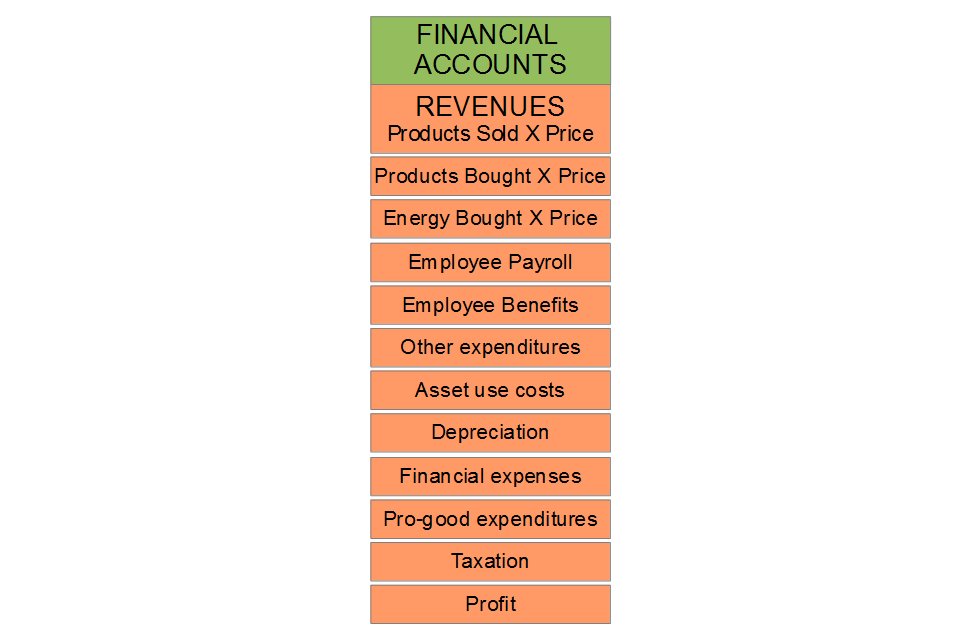

FINANCIAL ACCOUNTS Financial Accounts describe Economic Activity REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit TRUE VALUE ACCOUNTING

69.

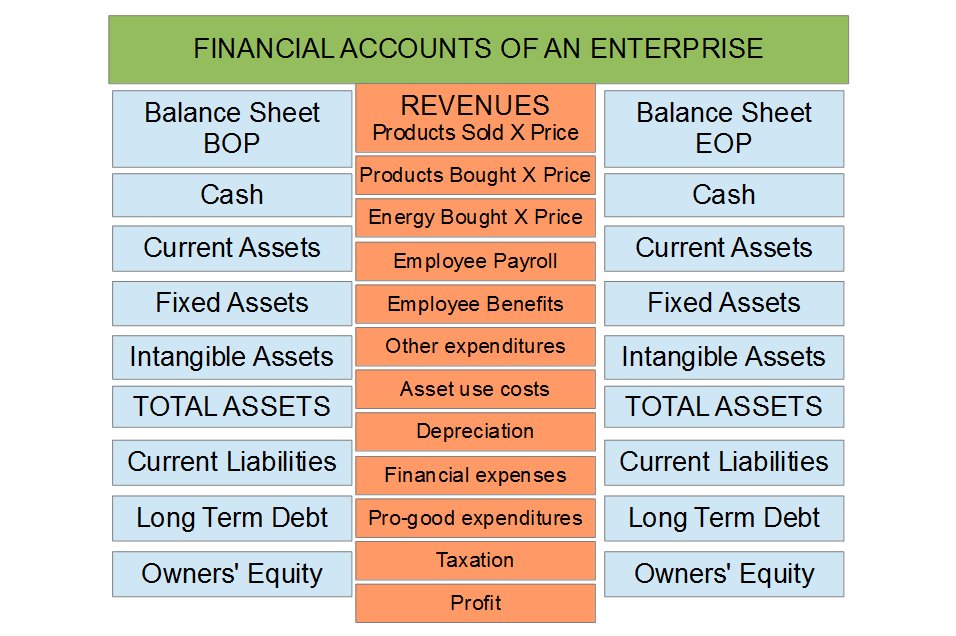

FINANCIAL ACCOUNTS OF AN ENTERPRISE Financial Accounts describe Economic Activity REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit Cash Current Assets Fixed Assets Intangible Assets TOTAL ASSETS Current Liabilities Long Term Debt Owners' Equity Cash Current Assets Fixed Assets Intangible Assets TOTAL ASSETS Current Liabilities Long Term Debt Owners' Equity Balance Sheet BOP Balance Sheet EOP TRUE VALUE ACCOUNTING

70.

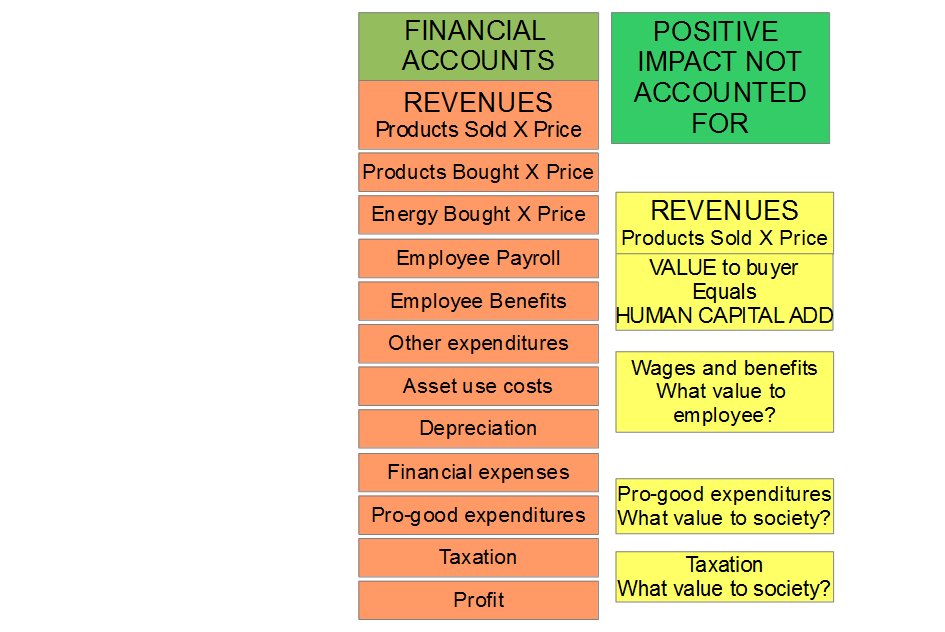

FINANCIAL ACCOUNTS ADD positive impact not accounted for REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? POSITIVE IMPACT NOT ACCOUNTED FOR

71.

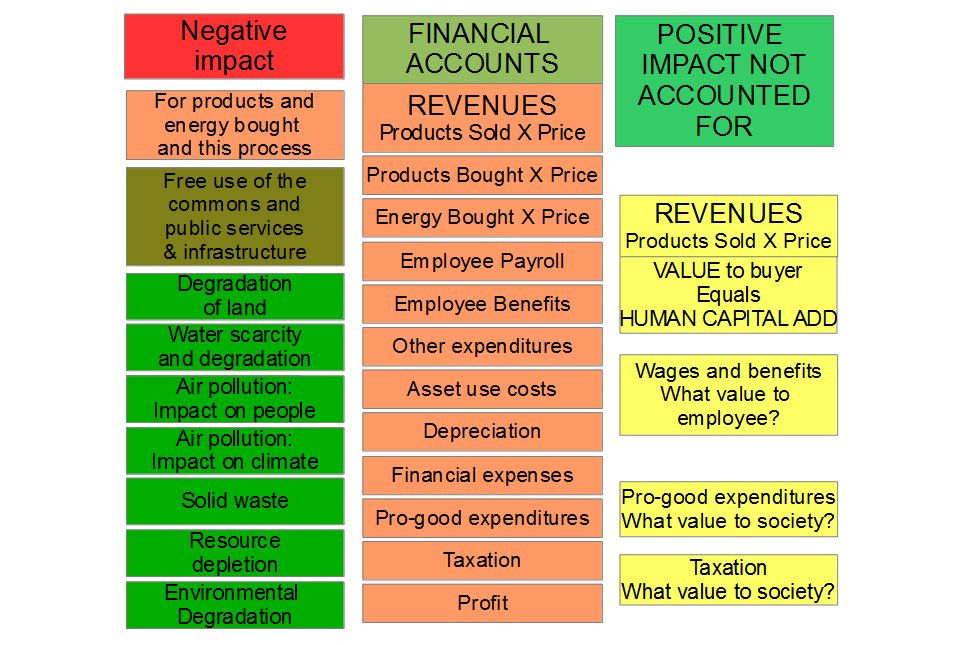

FINANCIAL ACCOUNTS DEDUCT negative impact not accounted for REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation Negative impact TRUE VALUE ACCOUNTING

72.

FINANCIAL ACCOUNTS ACCOUNTING FOR EVERYTHING REVENUES Products Sold X Price Products Bought X Price Energy Bought X Price Employee Benefits Employee Payroll Other expenditures Asset use costs Depreciation Financial expenses Pro-good expenditures Taxation Profit REVENUES Products Sold X Price VALUE to buyer Equals HUMAN CAPITAL ADD Wages and benefits What value to employee? Pro-good expenditures What value to society? Taxation What value to society? For products and energy bought and this process Free use of the commons and public services & infrastructure Degradation of land Water scarcity and degradation Air pollution: Impact on people Air pollution: Impact on climate Air pollution: Impact on people Solid waste Resource depletion Environmental Degradation POSITIVE IMPACT NOT ACCOUNTED FOR Negative impact TRUE VALUE ACCOUNTING

73.

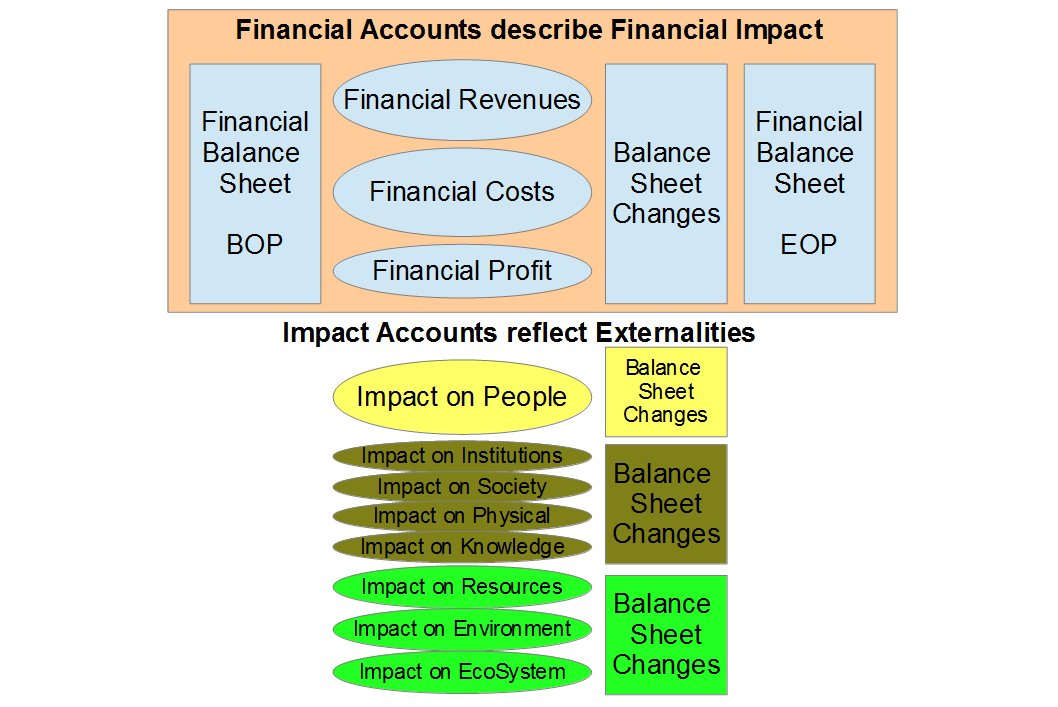

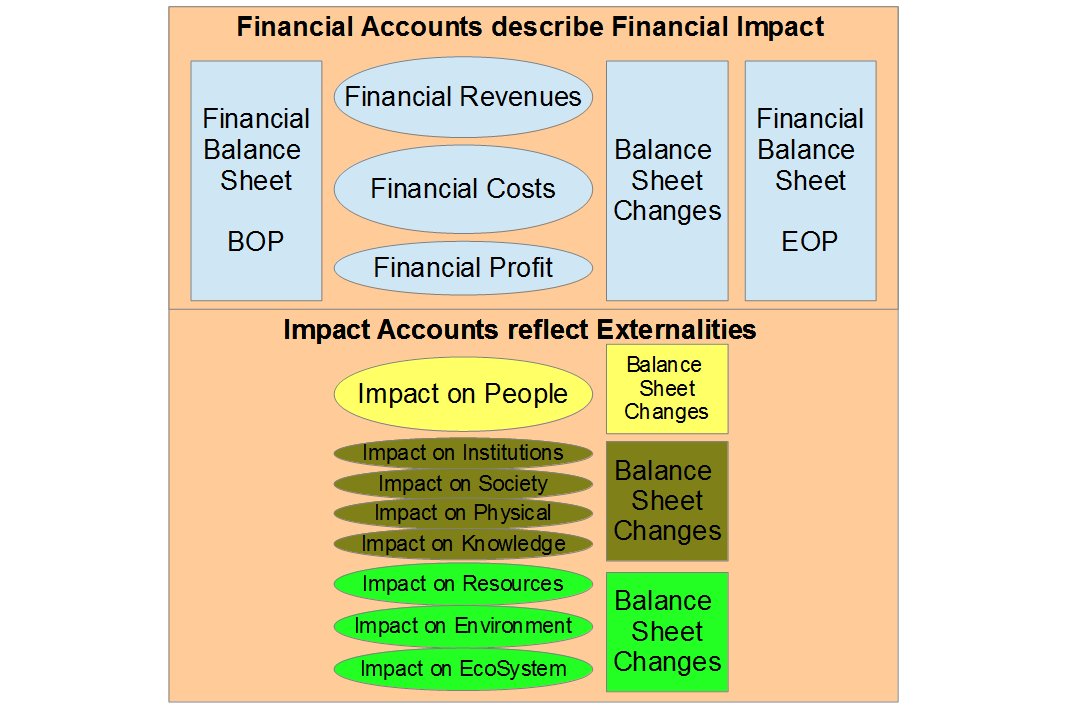

Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes TRUE VALUE ACCOUNTING

74.

75.

Sun BOP EOP Sun Financial Capital Human Capital Man Built Capital Natural Capital Sun SunSun Financial Capital Human Capital Man Built Capital Natural Capital Sun Financial Accounts describe Financial Impact Impact Accounts reflect Externalities Impact on Institutions Impact on People Impact on Society Impact on Physical Impact on Knowledge Impact on Resources Impact on Environment Impact on EcoSystem Balance Sheet Changes Balance Sheet Changes Balance Sheet Changes TRUE VALUE ACCOUNTING Financial Accounts describe Financial Impact Financial Costs Financial Profit Financial Revenues Financial Balance Sheet BOP Financial Balance Sheet EOP Impact Accounts reflect Externalities Balance Sheet Changes

76.

Complex system … competing agendas TRUE VALUE ACCOUNTING

77.

78.

79.

80.

81.

82.

THANK YOU Some links and contact information: Email Peter Burgess … peterbnyc@gmail.com Peter Burgess LinkedIn profile https://www.linkedin.com/in/peterburgess1 Link to TrueValueMetrics.org website http://www.truevaluemetrics.org/ Link to navigation to other resources: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav#1 TRUE VALUE ACCOUNTING

83. REMINDER This slideset is A WORK-IN-PROGRESS. It will be upgraded periodically. It is part of a series of more than 100 slidesets. Navigation to these is available here: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=N1-Slidesets-p3 More about the True Value Metrics initiative is at: http://www.truevaluemetrics.org/DBadmin/DBtxt001.php?vv1=list0100-MainNav FEEDBACK is welcome. Please email to Peter Burgess … peterbnyc@gmail.com … with a catchy phrase in the subject line so that it gets attention, and please identify the specific slideset(s) or webpage involved. TRUE VALUE ACCOUNTING

|

|

|

|

|