|

|

CORE CONCEPTS of TRUE VALUE ACCOUNTING

FLOW / PROCESS /CHANGE in STATE

|

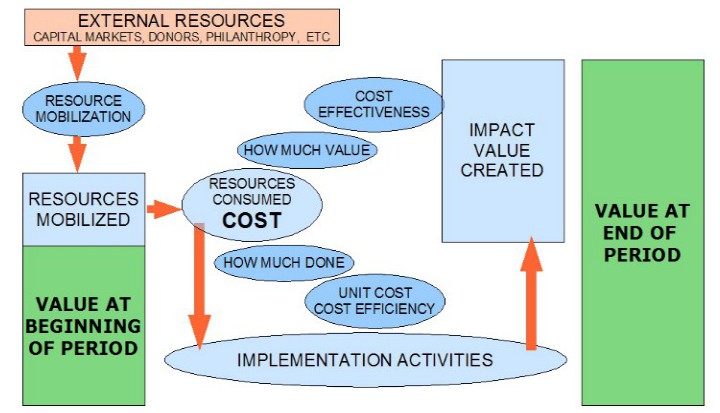

ACTIVITIES DELIVER RESULTS

Details of activities are NOT needed to measure PROGRESS ... merely CHANGE in STATE

PROGRESS is the increase in VALUE (of the STATE) from beginning to end of the period

Simply measure the change in the VALUE of everything

|

|

The Relationship Between Original State, Period Activities and New State

|

|

In this case the activities of the period do not change the state ... state at the end of the period (EOP) is the same as at the beginning of the period (BOP)

|

|

|

|

There is GOOD progress when the activities of the period result in a state at the end of the period that is better than the state at the beginning of the period.

|

|

|

|

There is BAD progress when the activities of the period result in a state at the end of the period that is worse than the state at the beginning of the period.

|

|

|

|

What this means is that PROGRESS can be ascertained by reference to the state at the beginning and the end of a period, with no need to have any knowledge of the activities during the period that results in the change.

When this is at the core of the progress measurement method, it enables a significant simplification of the data collection and analysis process.

TPB note: Over a period of around 20 years I was asked to do project monitoring and evaluation for the World Bank, the United Nations and others. The prevailing methodology was for the words of the project documents to be used as the basis for evaluation of performance, and it was often the case that a simplistic comparison of results with project goals could result in an assessment that the project was a success, it was also very clear that in terms of PROGRESS nothing had been achieved. As long as the performance of a project is merely about carrying out the activities as planned, but ignoring the impact and especially the impact on PROGRESS of the PLACE where the project was active, then 'development' is never going to be effective.

|

|

|

|

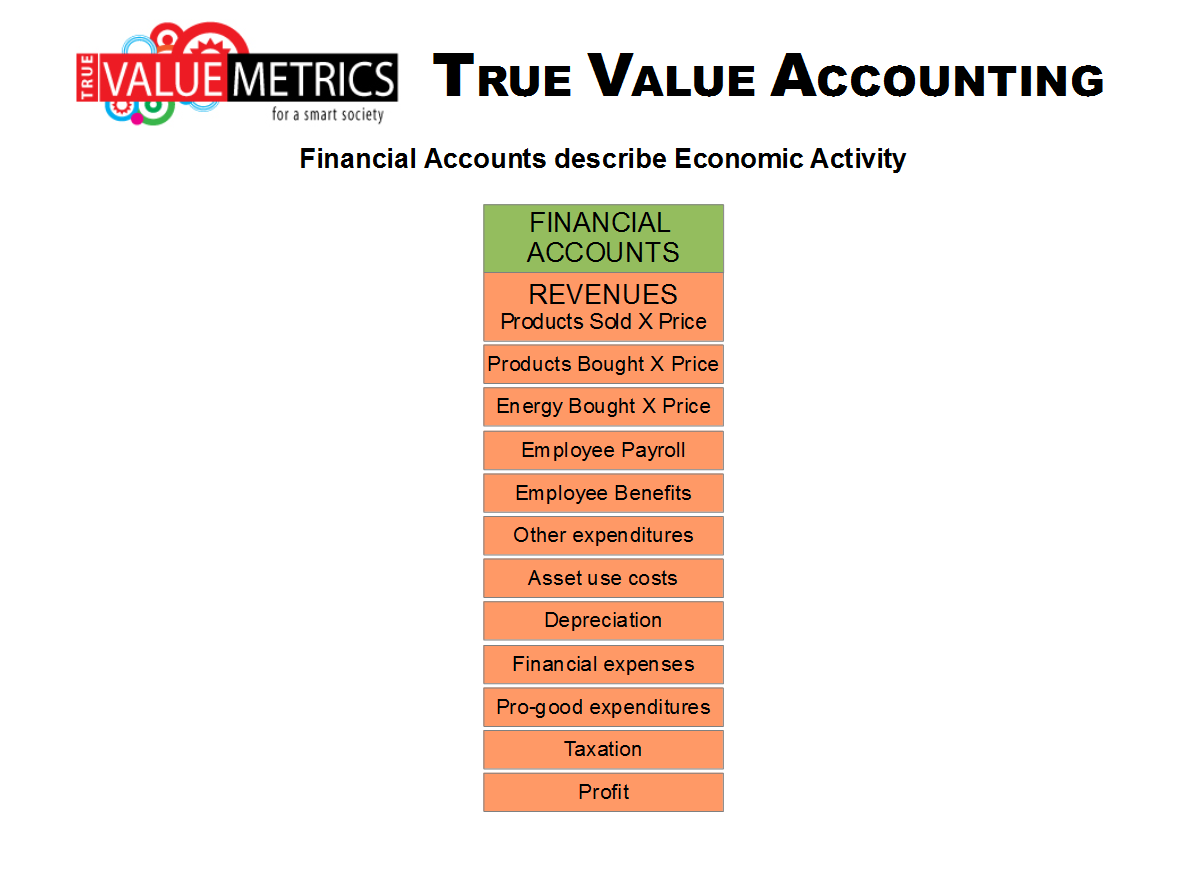

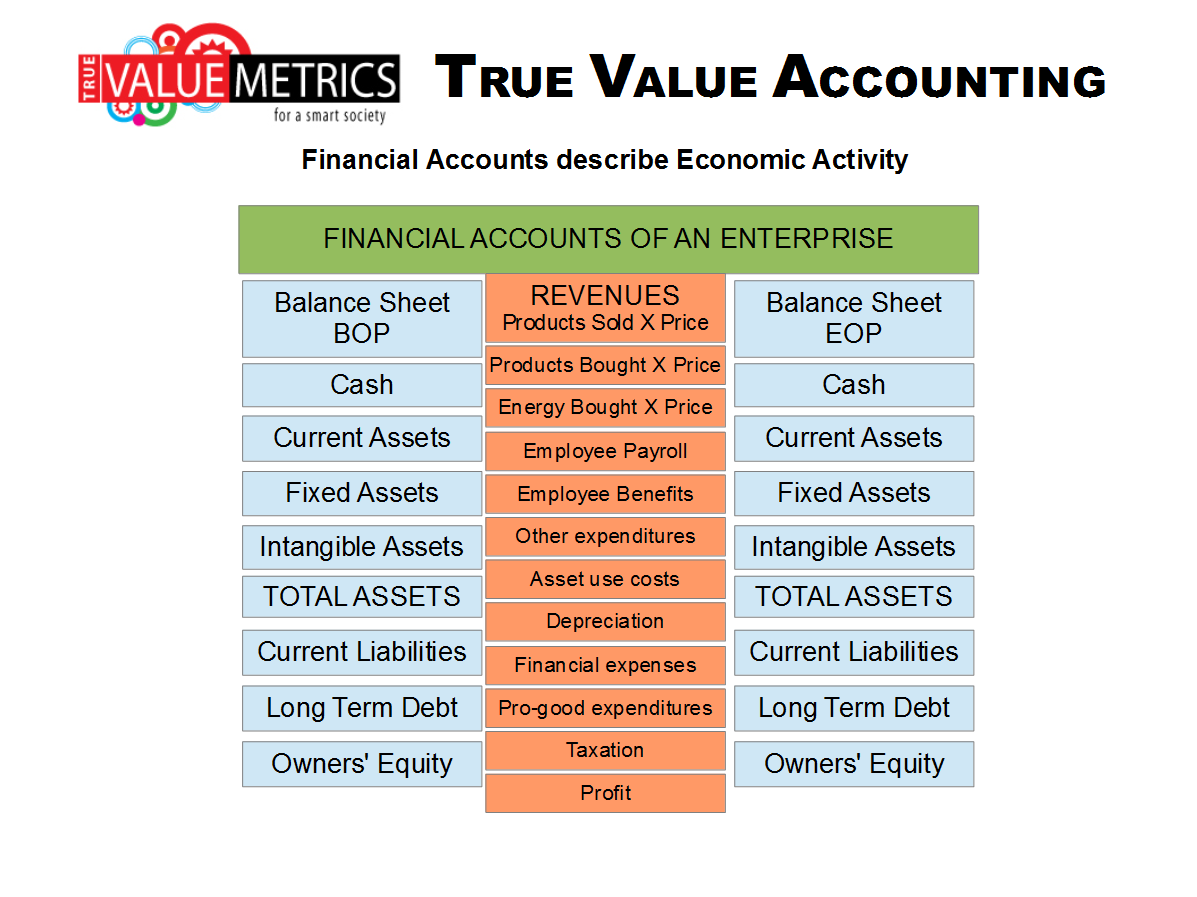

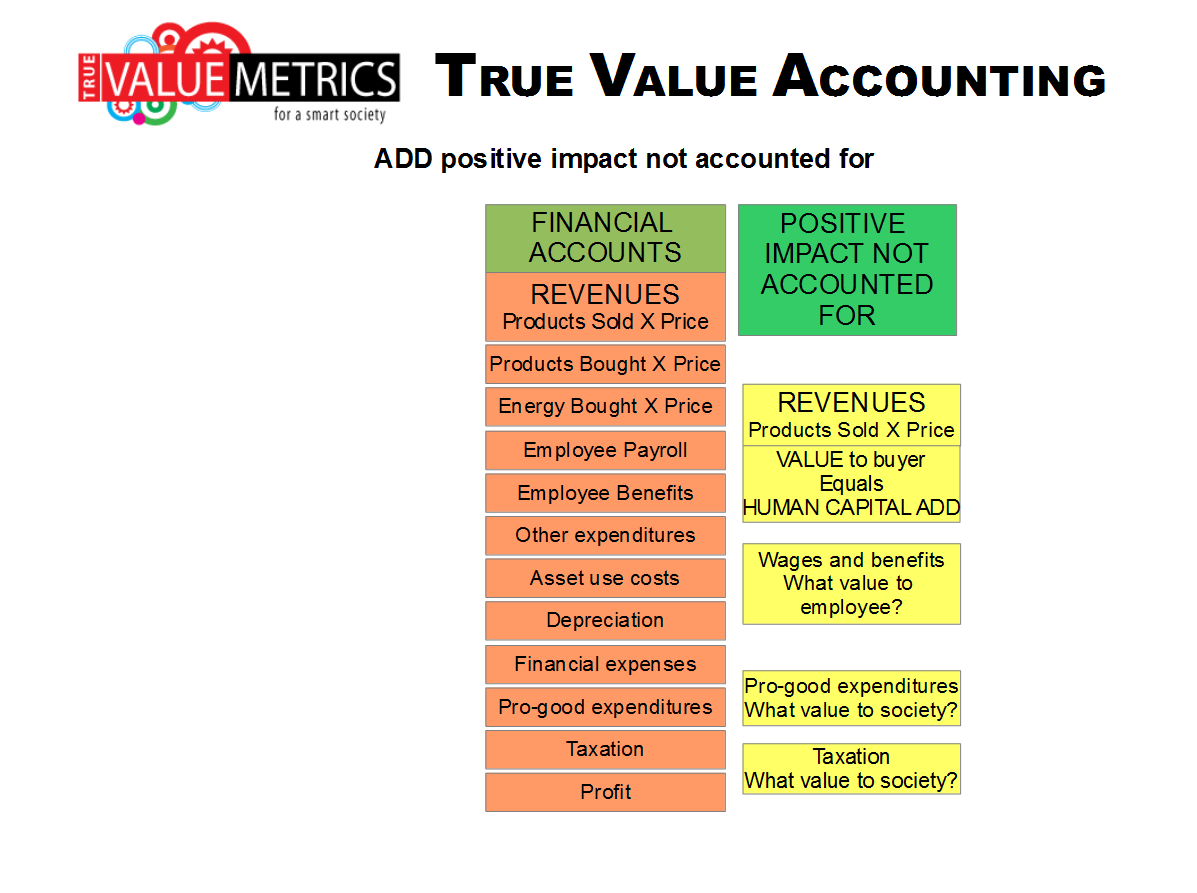

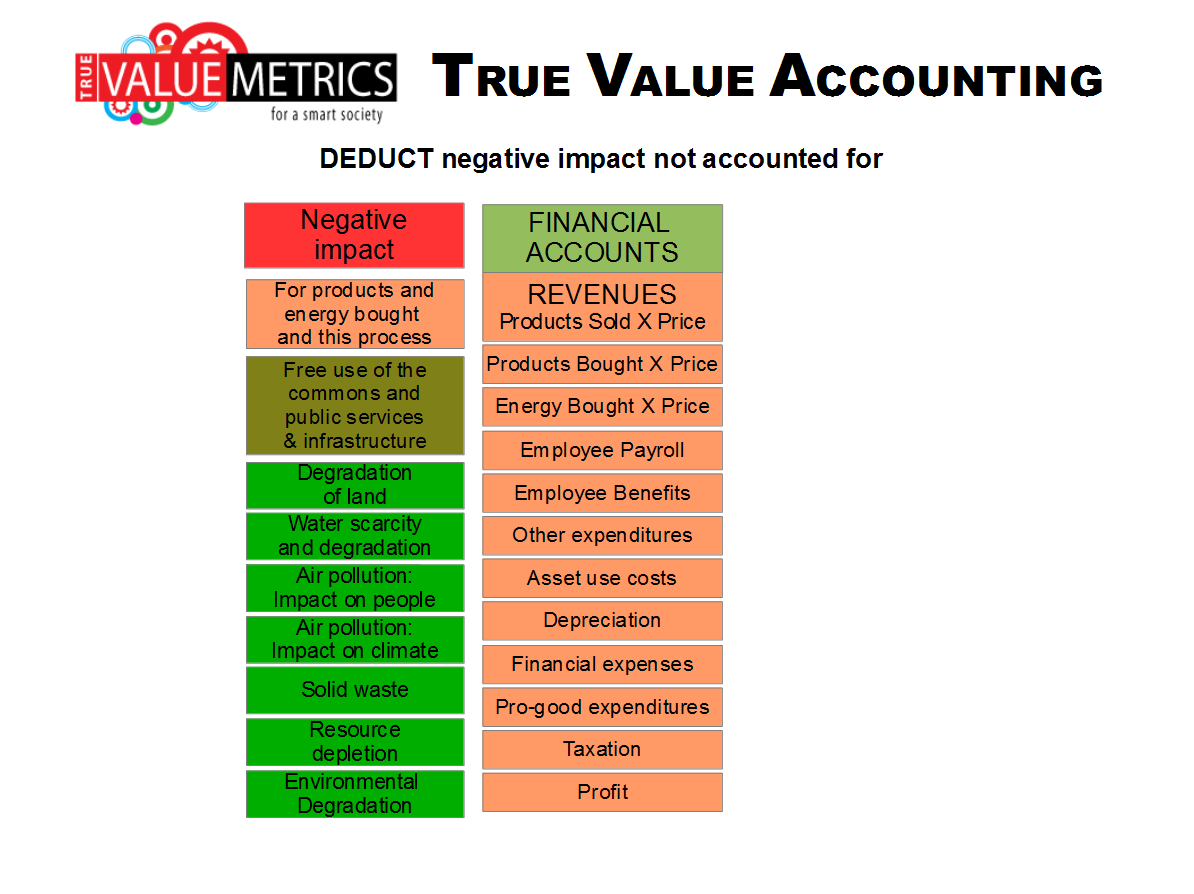

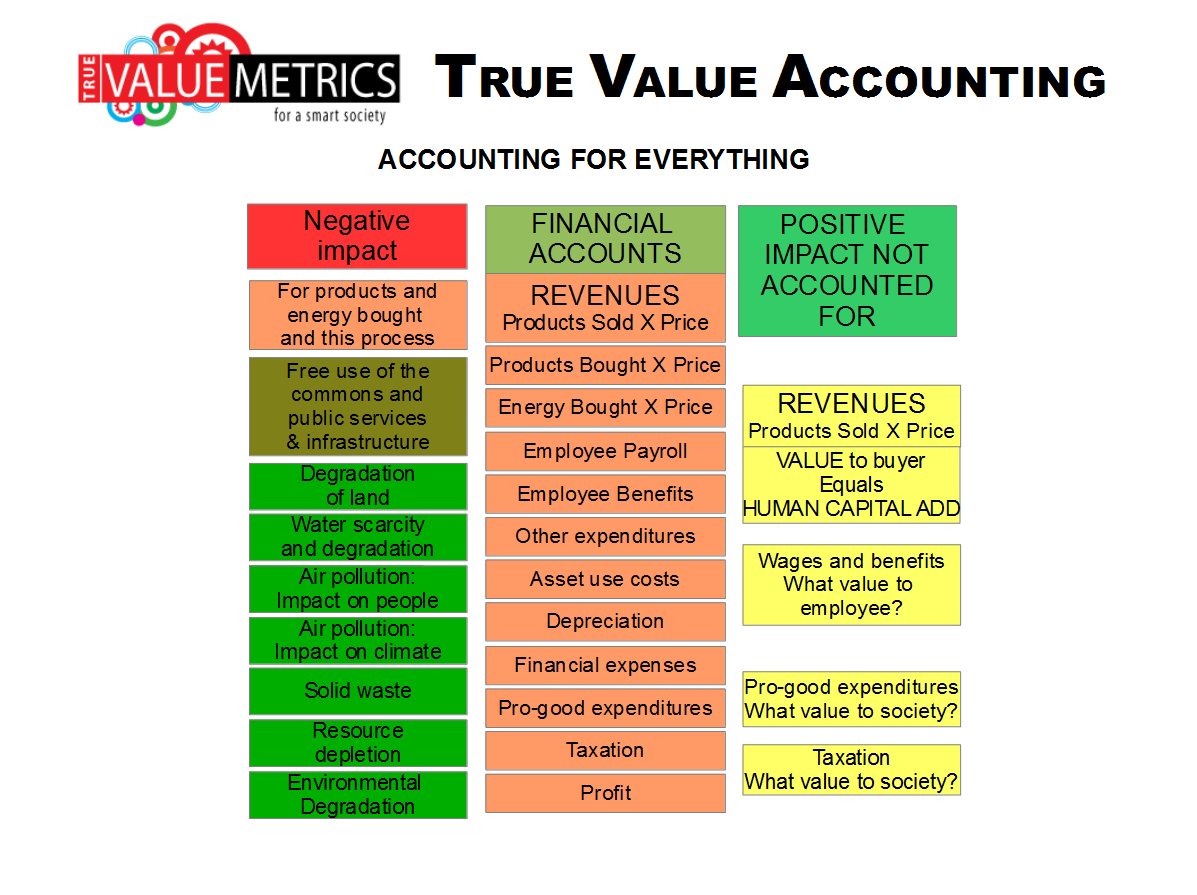

The problem with conventional accounting is that while it does a very good job for money based transactions, it ignores all the impact that is not measured with money and included in the core transaction.

Since the beginning of the industrial revolution, the growth of conventional financial wealth has come while human capital has been exploited and natural capital has been depleted. When the global economy was quite small in size, the natural capital depletion did not represent an existential threat, but the scale of the modern industrial activity has now reached a level where natural capital depletion is a significiant risk.

|

|

|

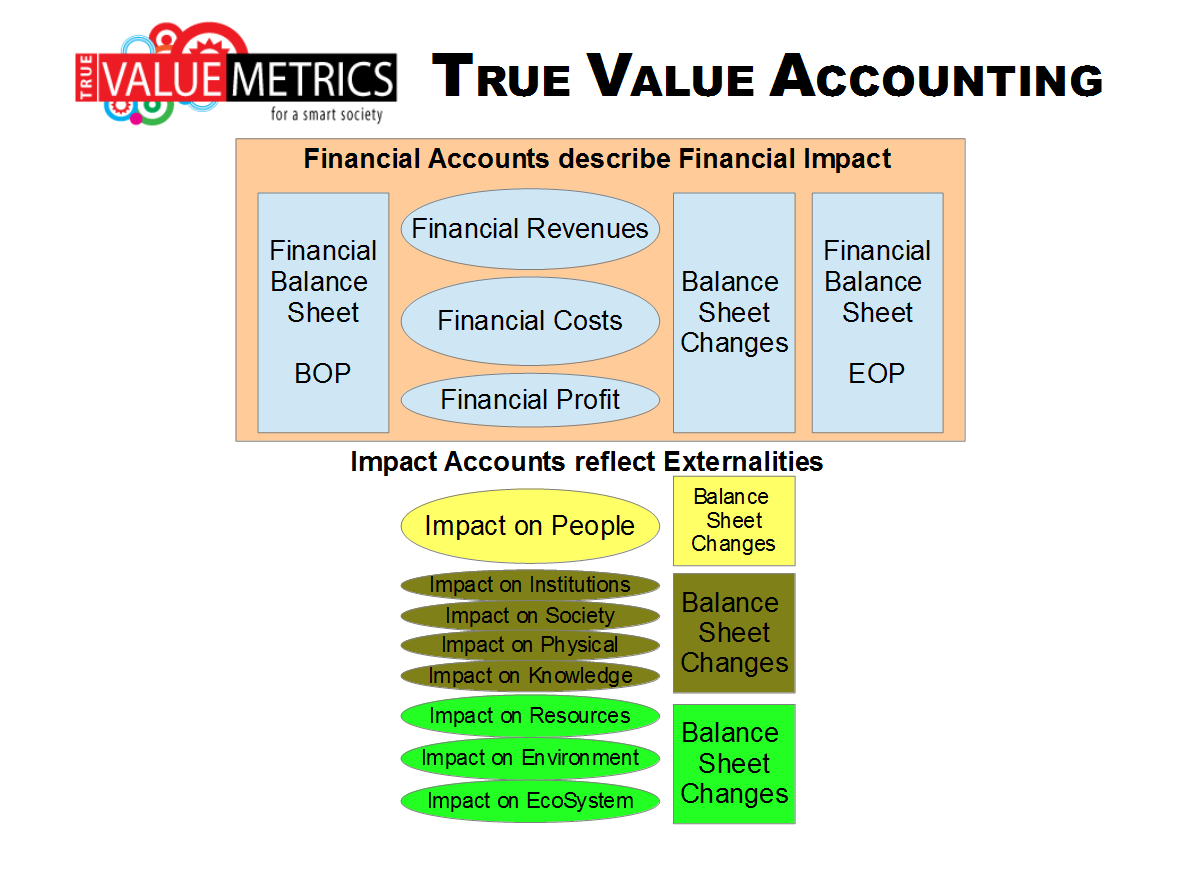

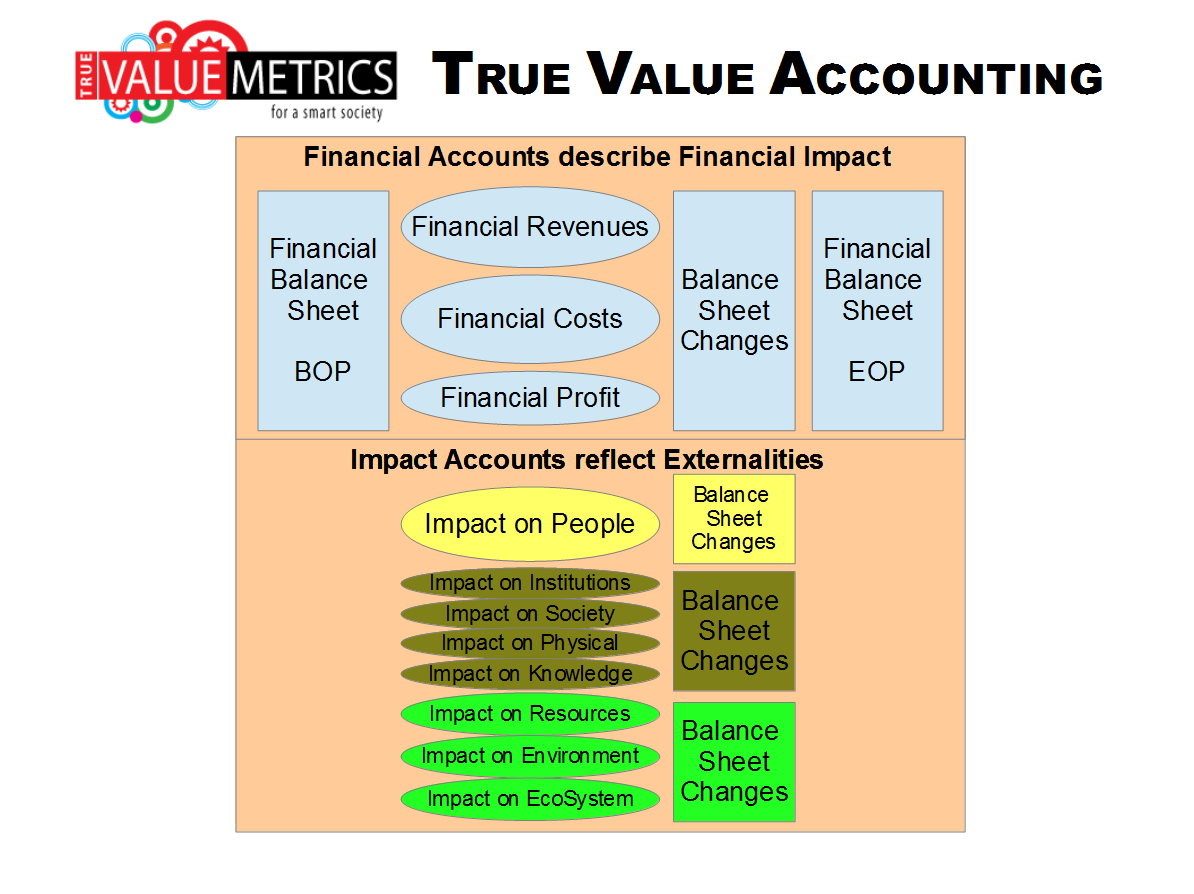

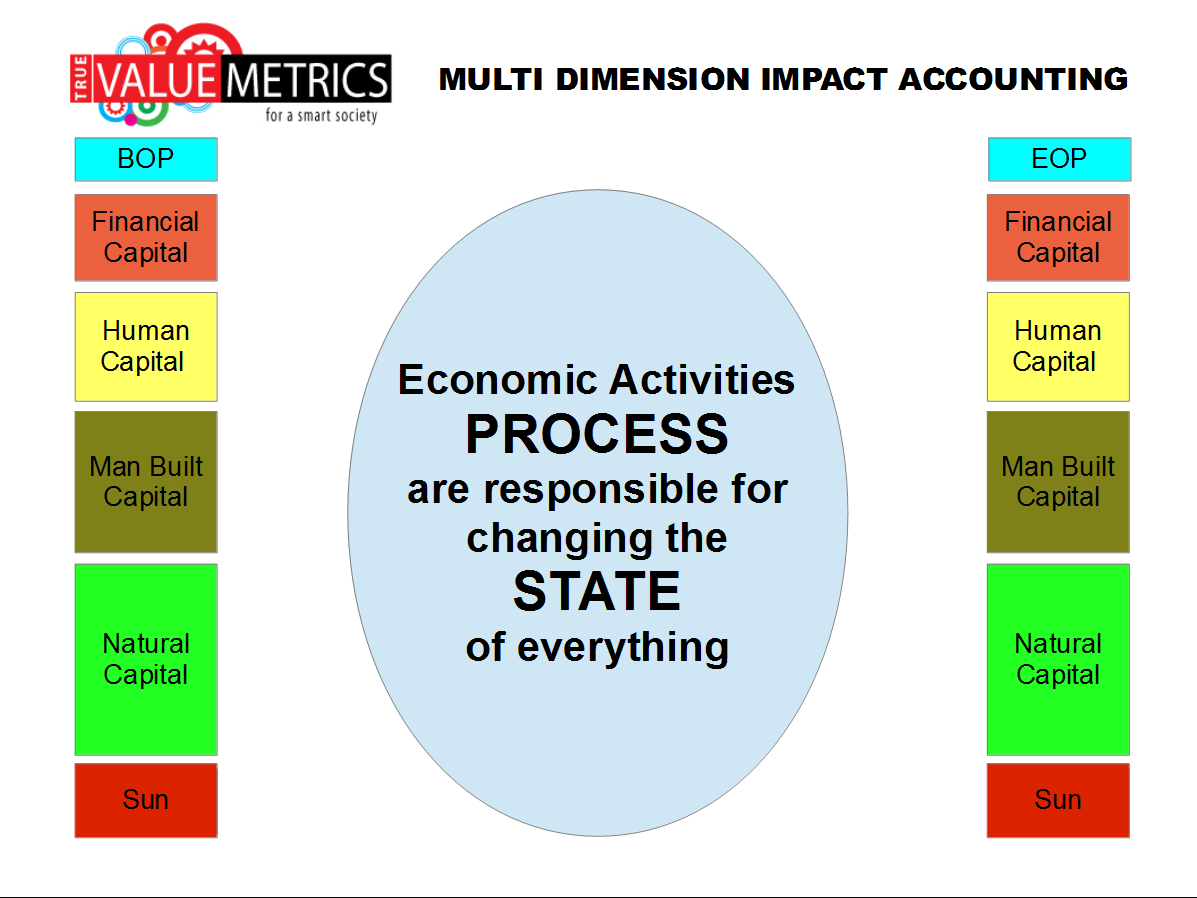

STATE ... A Balance Sheet Shows State

|

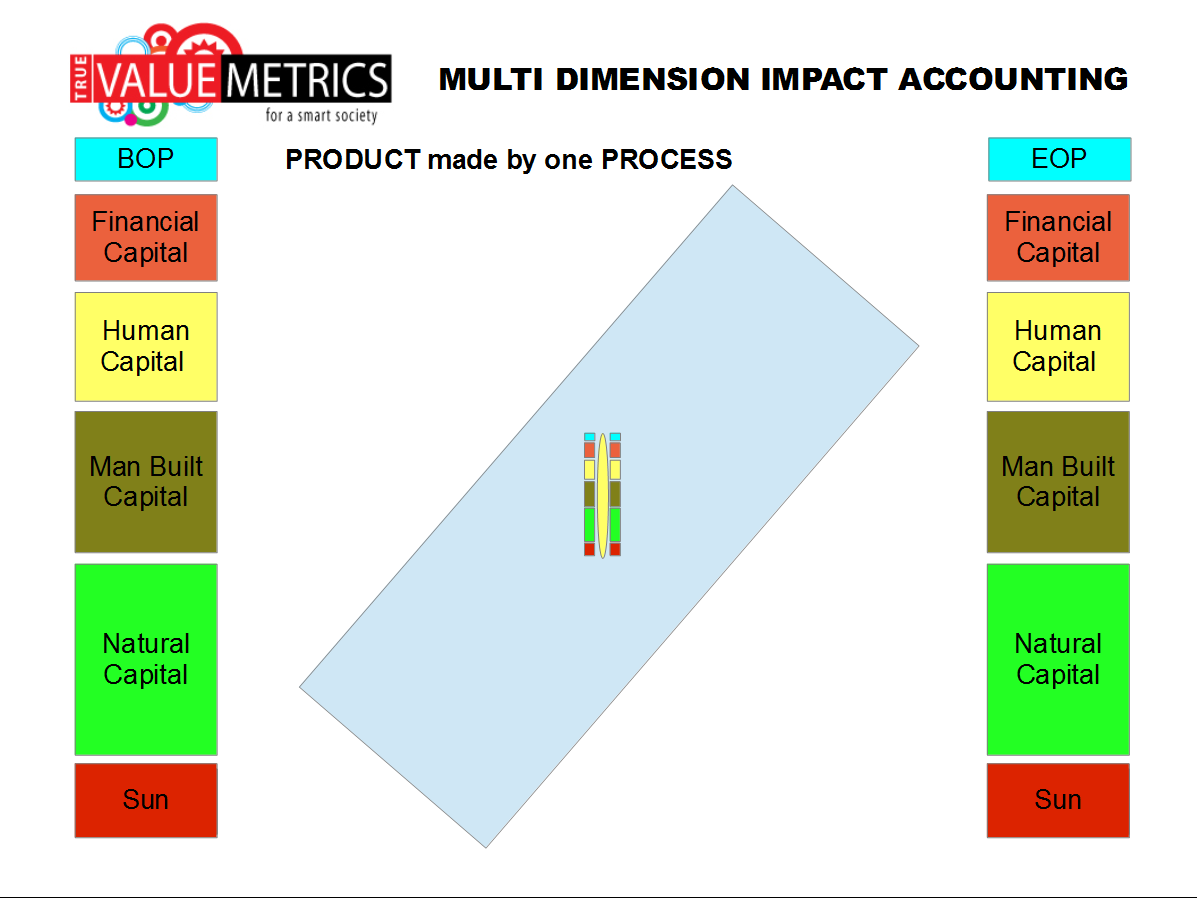

PROCESS

THE MAIN DETERMINANT OF SOCIO-ENVIRO-ECONOMIC EFFICIENCY

|

|

|

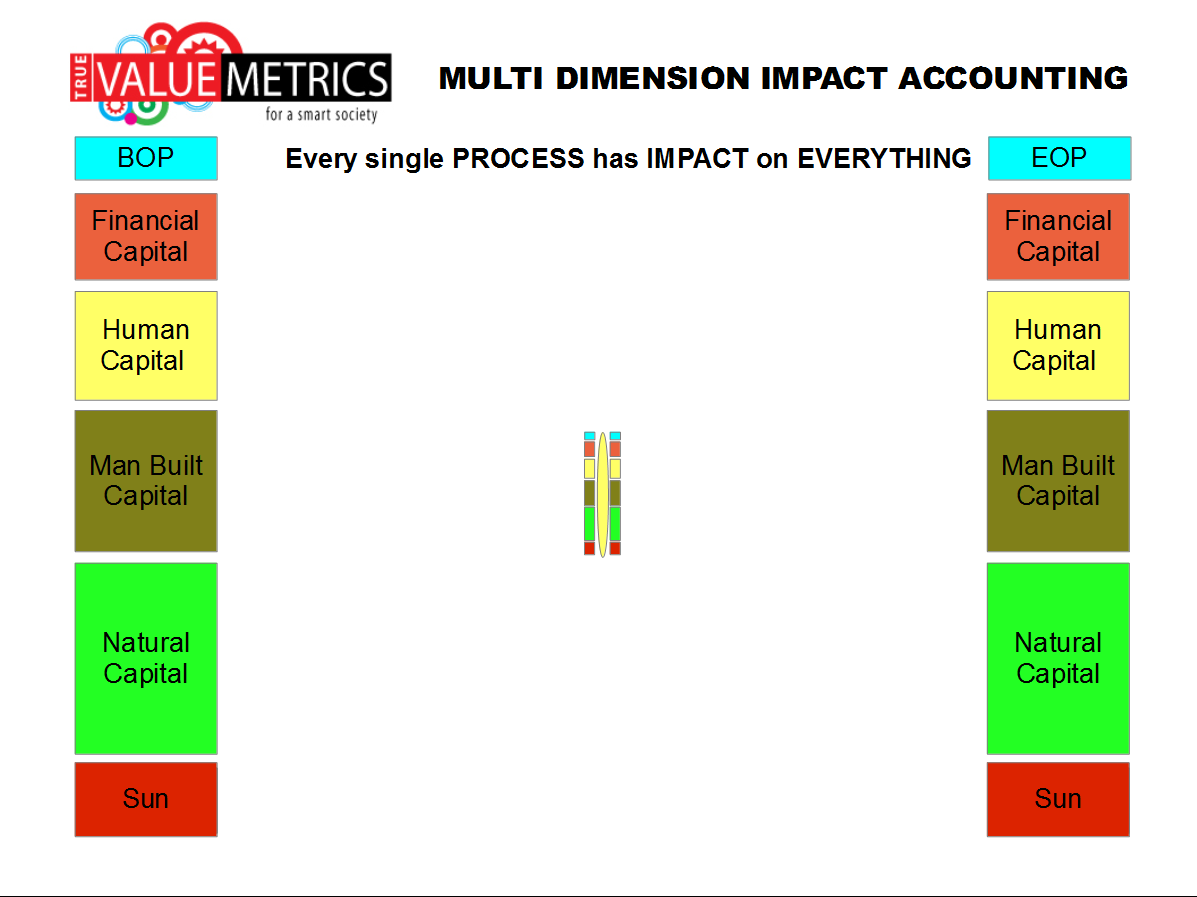

PROCESS IS EVERYWHERE ...

NOTE: The PROCESS is equivalent to the NODE in context / entity / relationship diagrams

PROCESS uses inputs (labor, materials, energy, knowhow, natural resources, etc.) and in the process degrades the environment;

PROCESS produces PRODUCTS (goods and services) ... outputs ... that enable good quality of life and living standards.

|

|

|

The EFFICIENCY of the PROCESS determines the IMPACT on PEOPLE and PLANET.

EFFICIENCY is not only the PROFITABILTY of the PROCESS …

… but also how much GOOD IMPACT there is for PEOPLE …

… and how little BAD IMPACT for SOCIETY and the ENVIRONMENT.

|

|

|

|

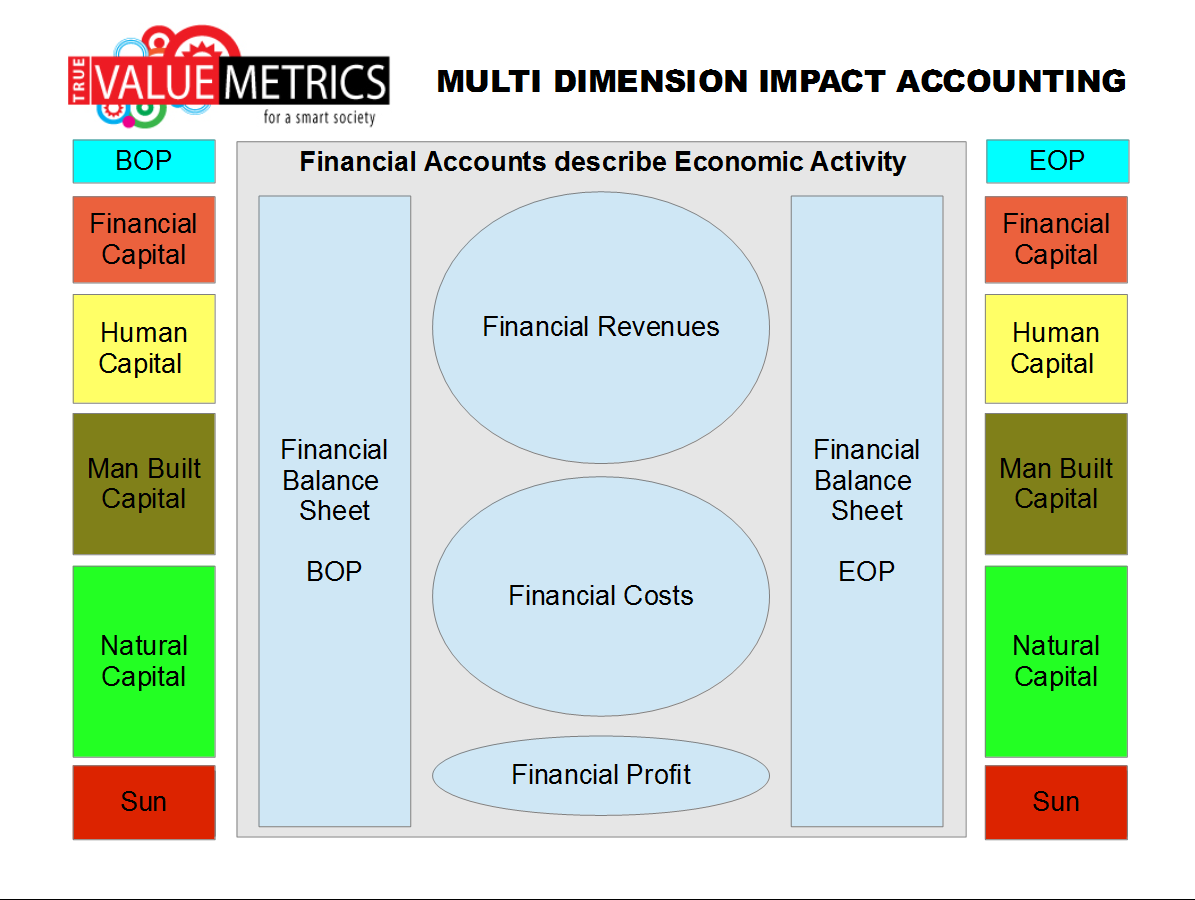

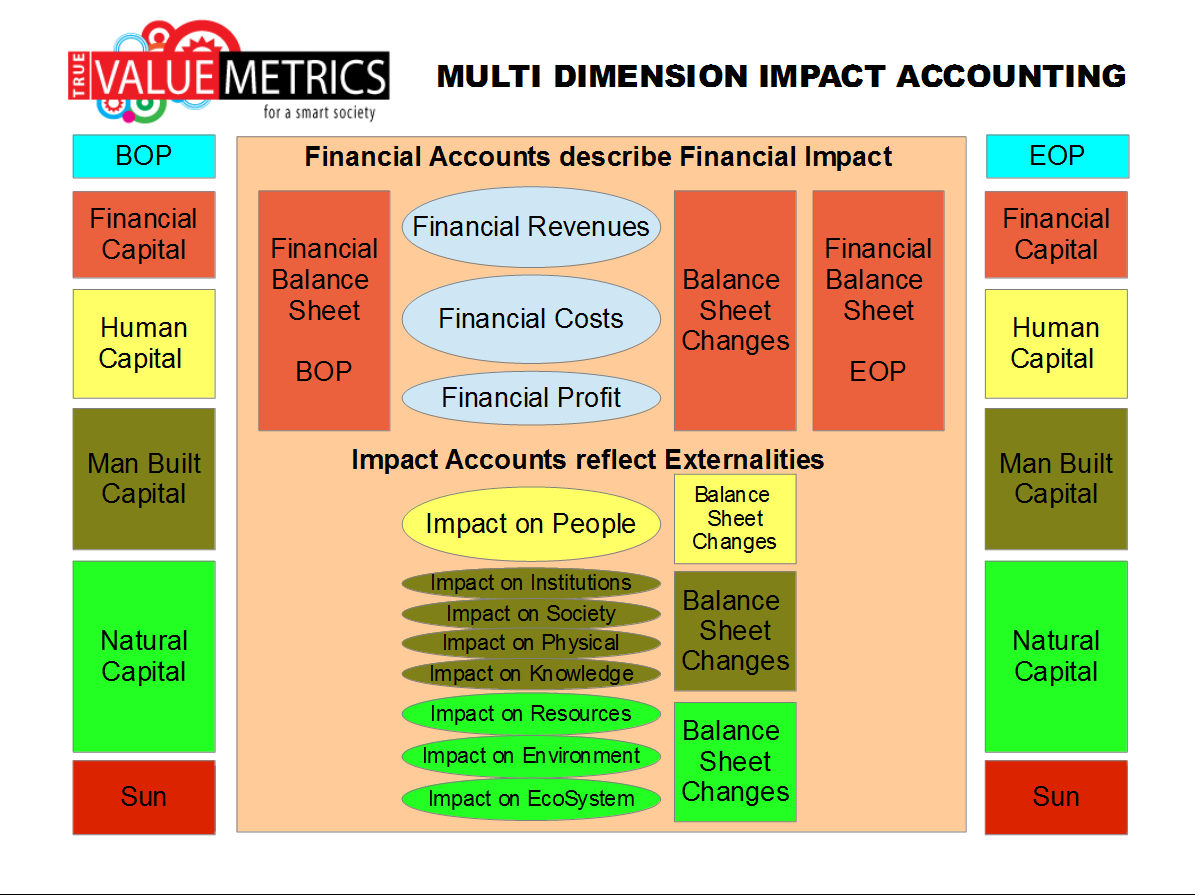

Financial Accounts and related management information are very powerful

HOWEVER ...

Financial accounts describe economic activity in financial or money terms while completely ignoring impact on everything else.

|

|

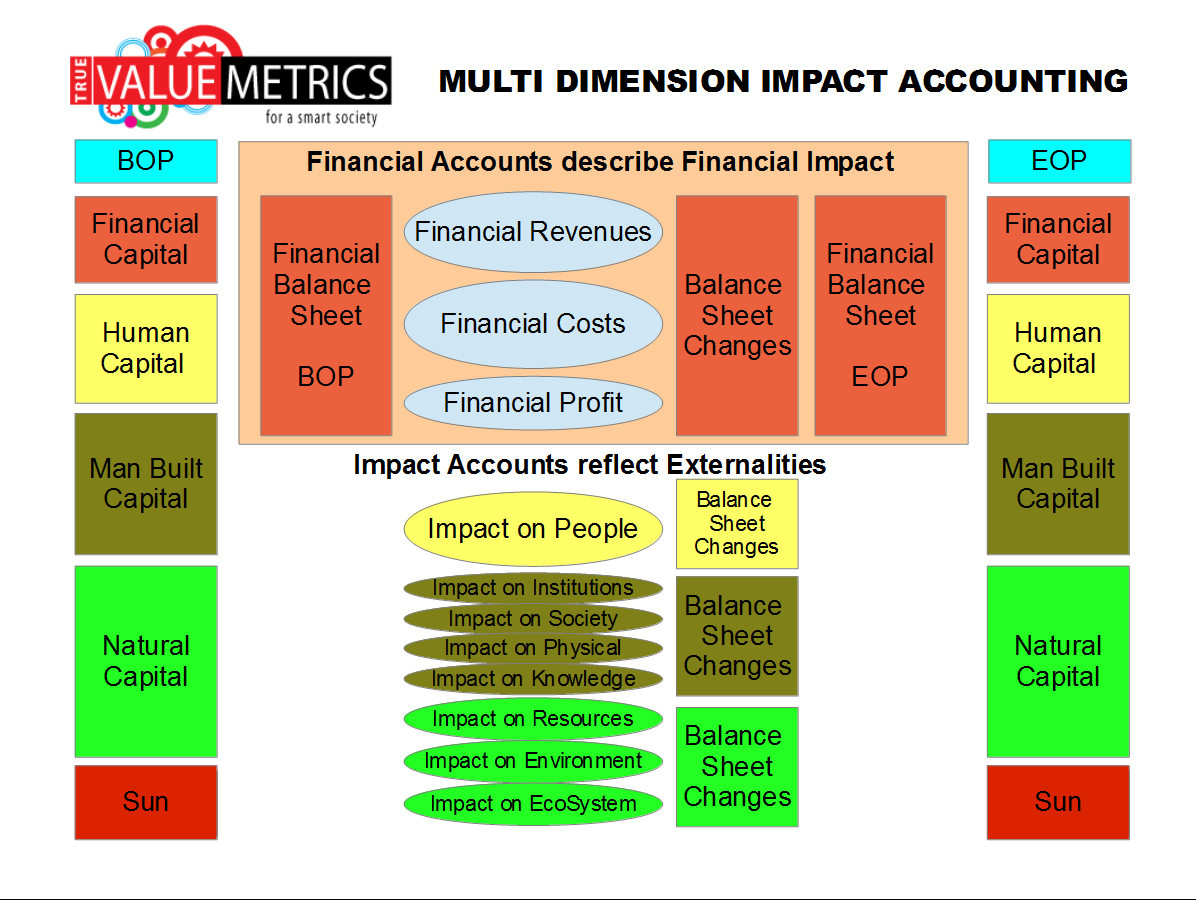

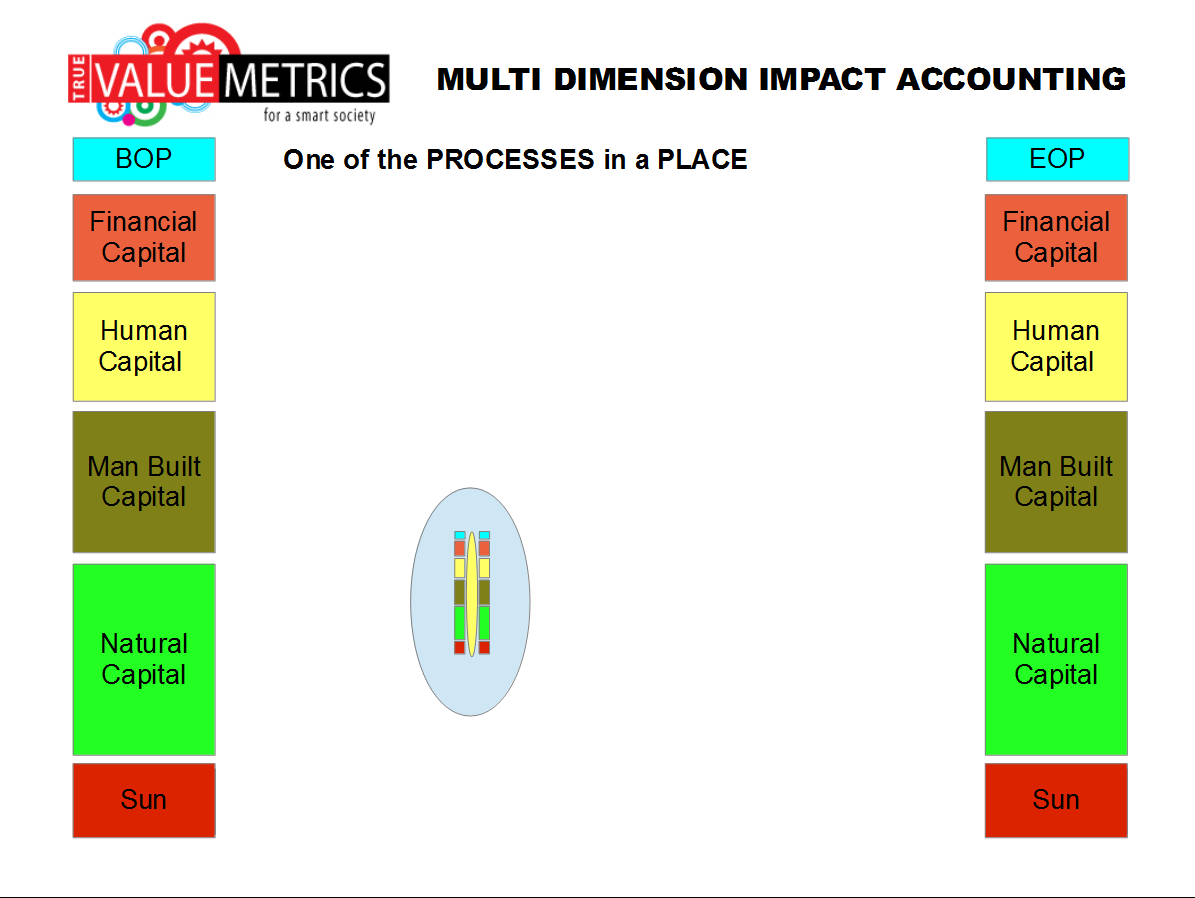

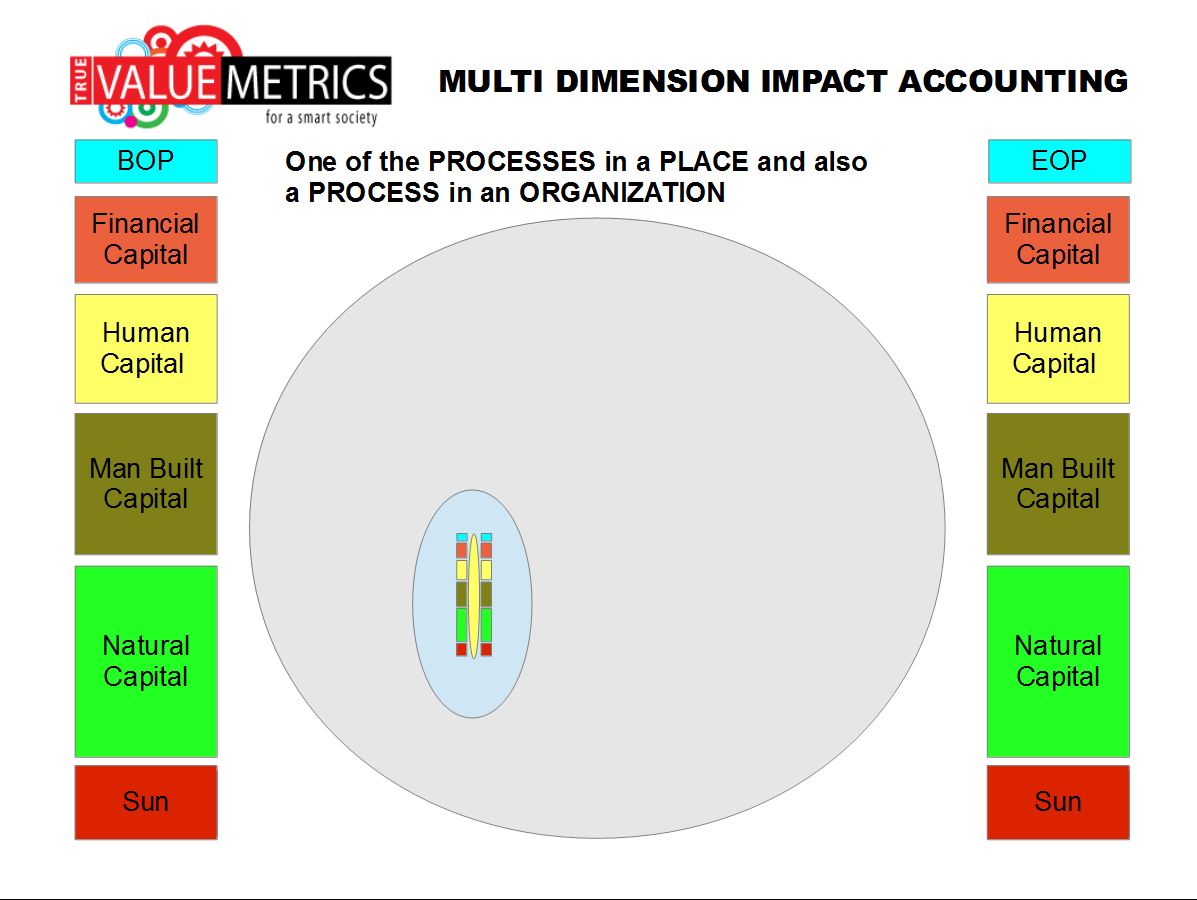

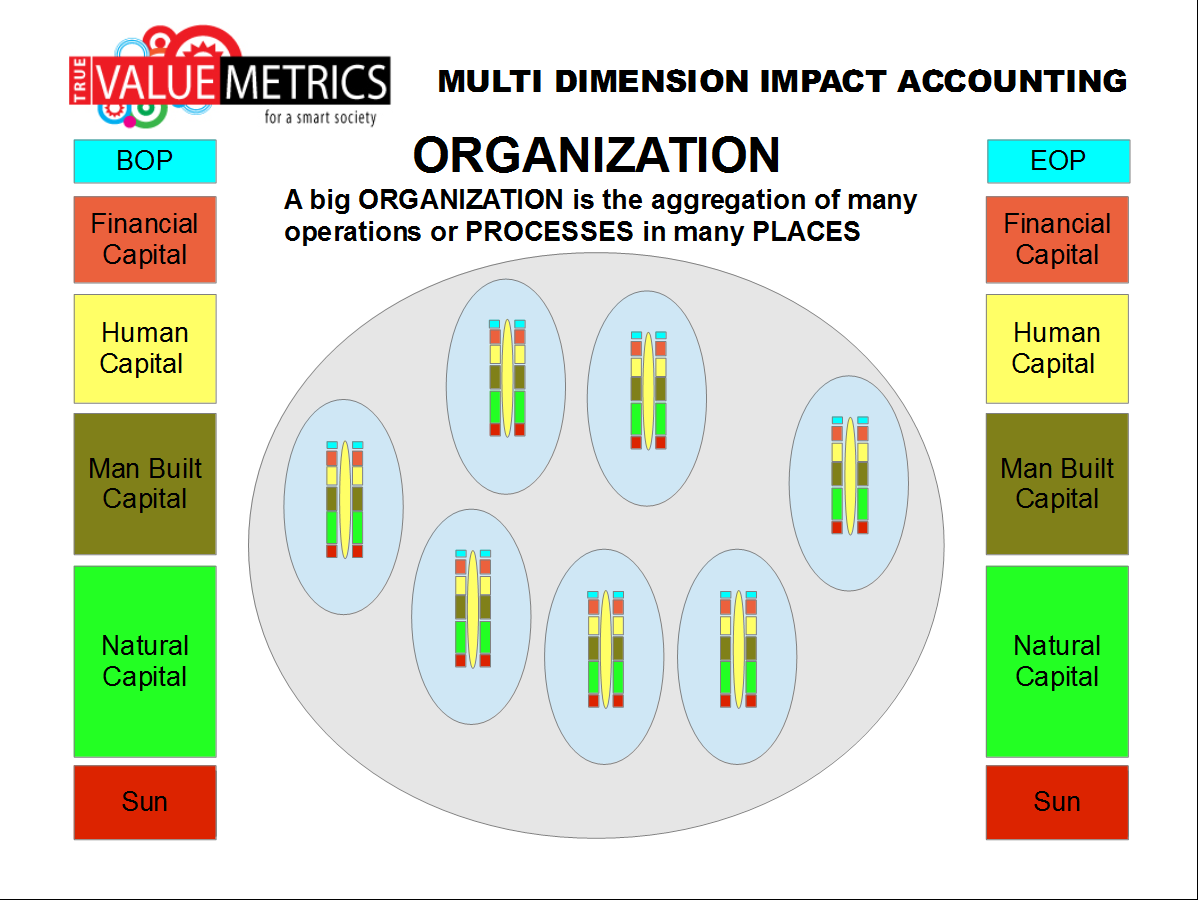

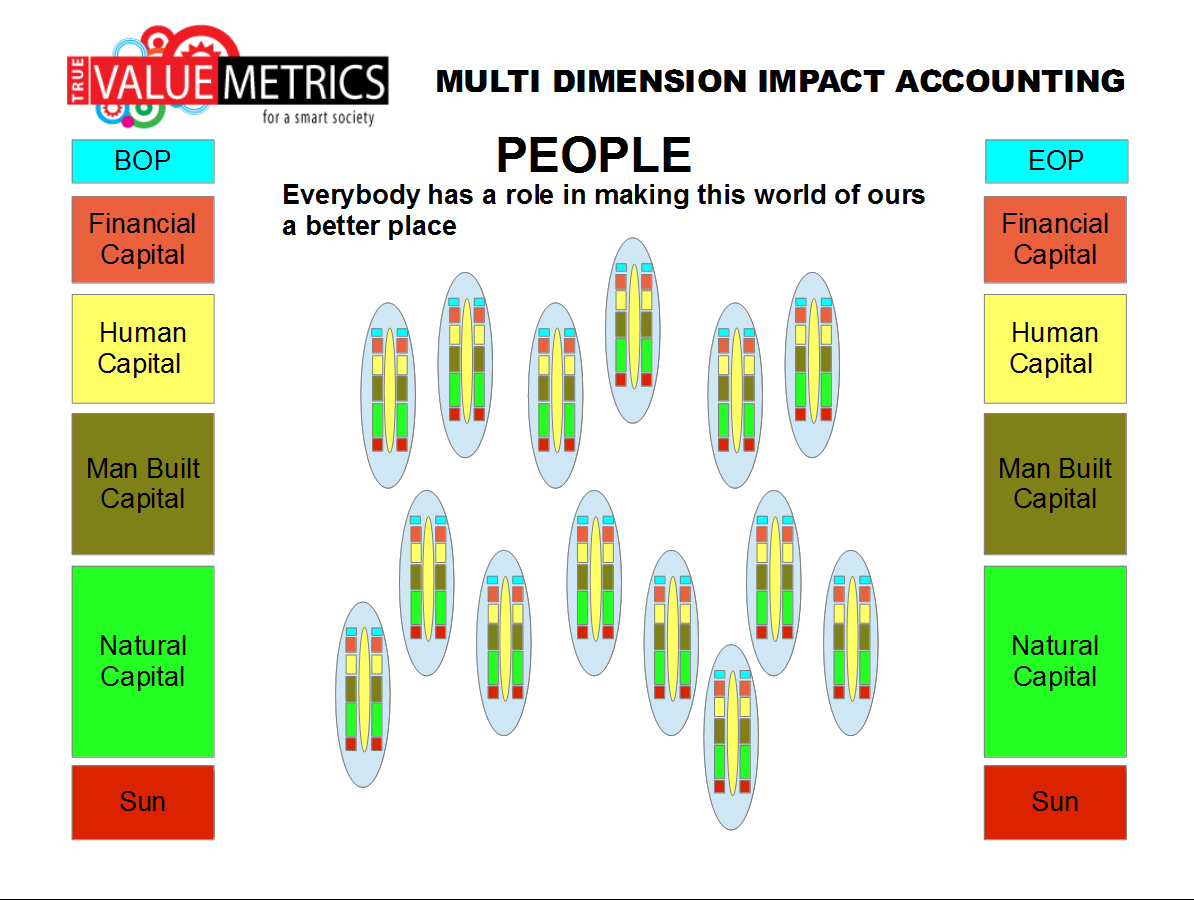

IMPACT OF THE PROCESS

IMPACT OF ECONOMIC ACTIVITY ON ALL THE CAPITALS

|

|

|

The next slides show how the data architecture has to be designed in order for IMPACT of the PROCESS to be accounted for in a rigorous and logical way …

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

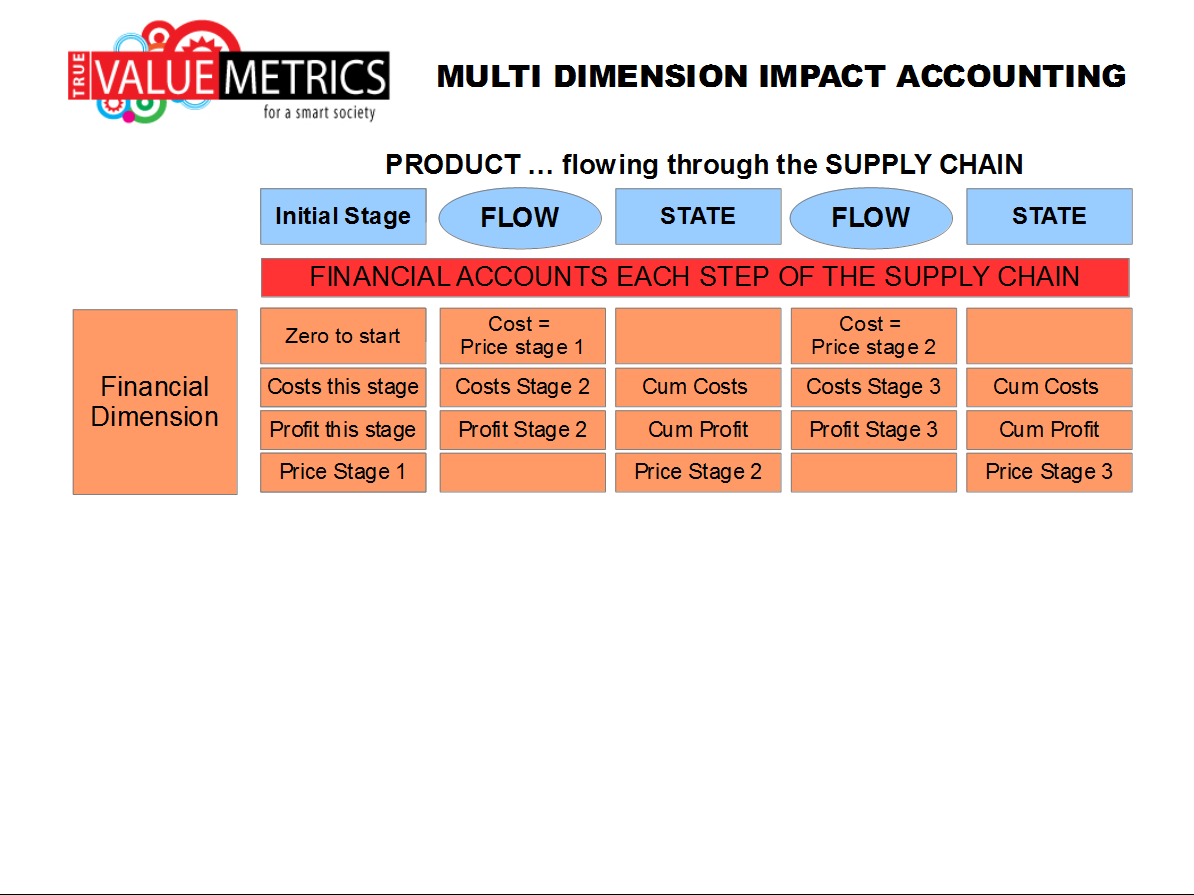

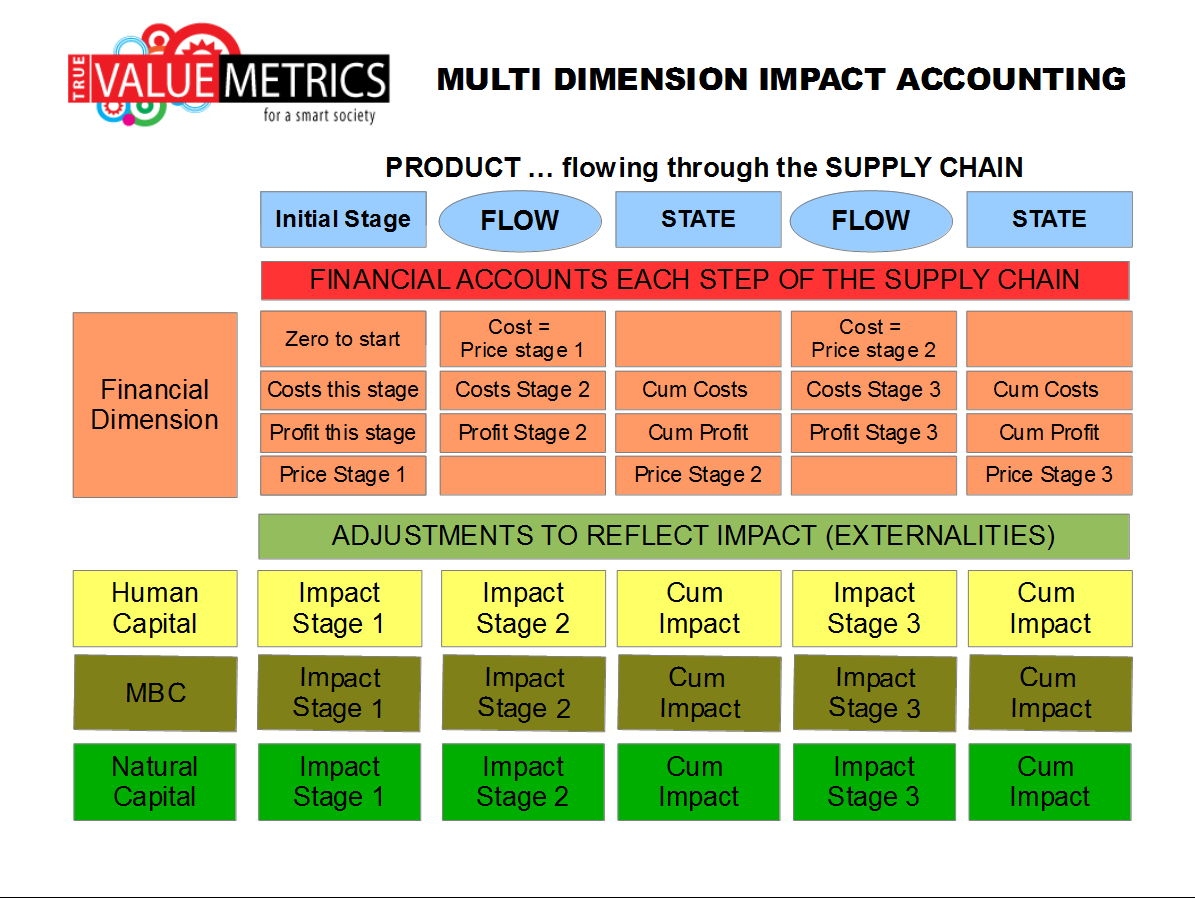

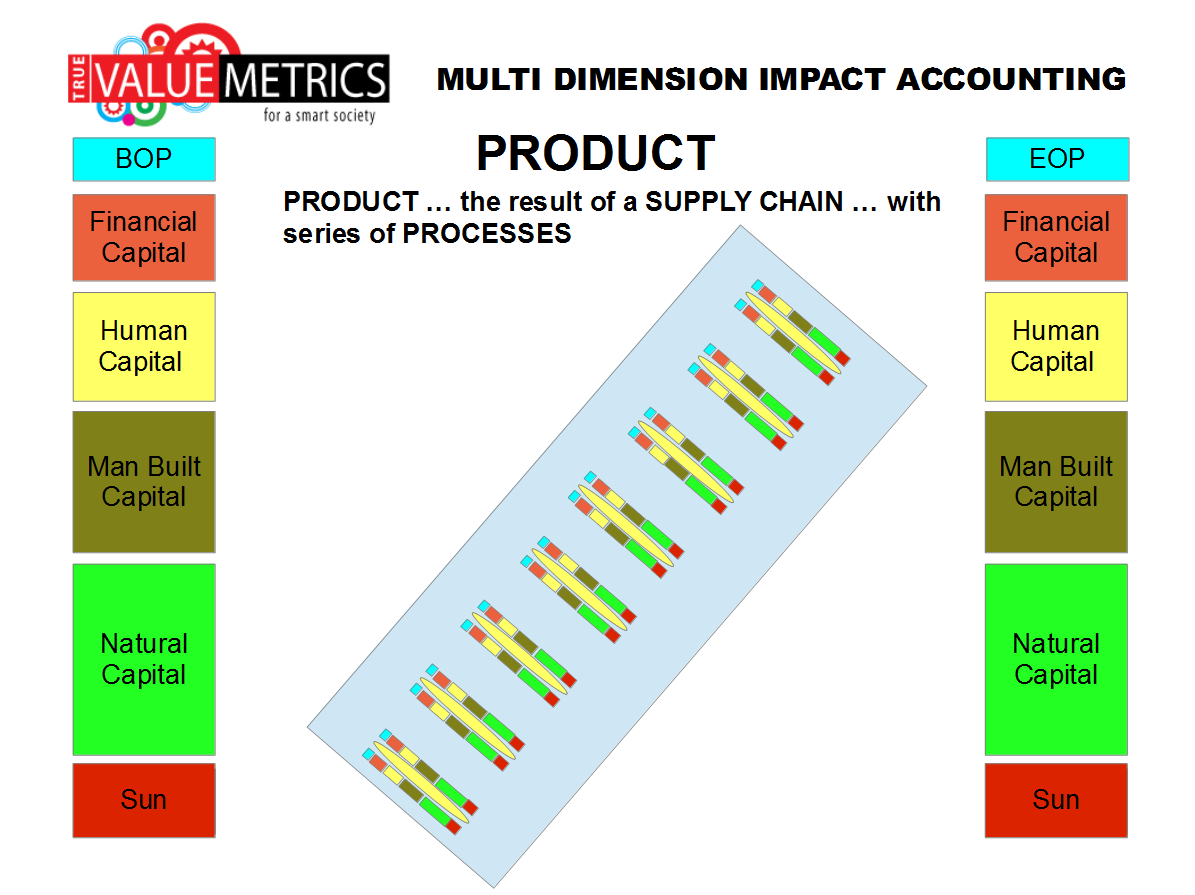

SUPPLY CHAIN

IN THE SUPPLY CHAIN A PRODUCT FLOWS THROUGH MANY STAGES

|

|

|

PRODUCT AND SUPPLY CHAIN

… The MONEY dimension of the supply chain is routine; however

… The IMPACT of the supply chain on SOCIETY (PEOPLE) and ENVIRONMENT (PLANET) are rarely implemented in a coherent manner.

… This is very big next step!

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PROCESS

THE MAIN DETERMINANT OF SOCIO-ENVIRO-ECONOMIC EFFICIENCY

|

|

|

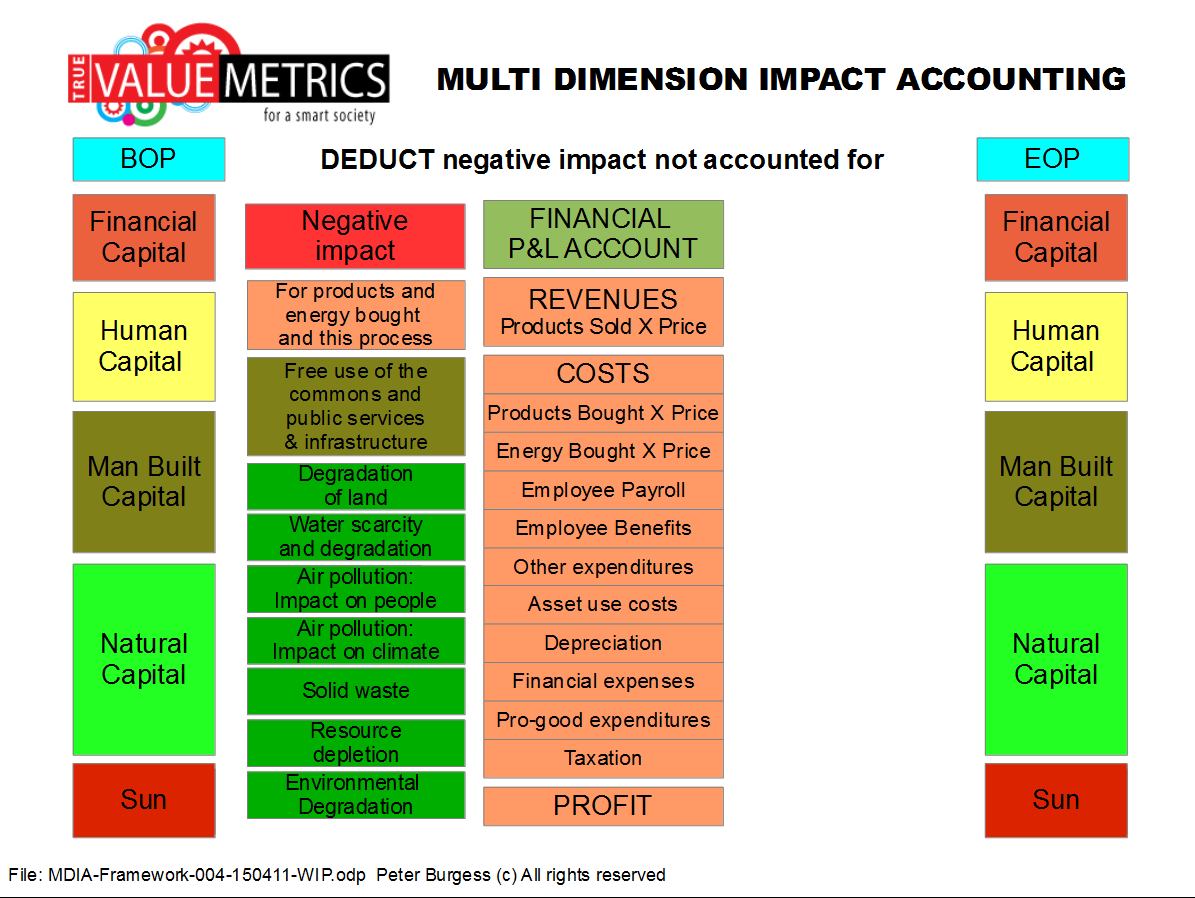

The next slide shows …

… how the money P&L report describes the impact of the money transactions on the money balance sheet of the operation …

… while the IMPACTS of the operations on society and the environment are ignored because they are outside the reporting envelope.

|

|

|

|

|

|

|

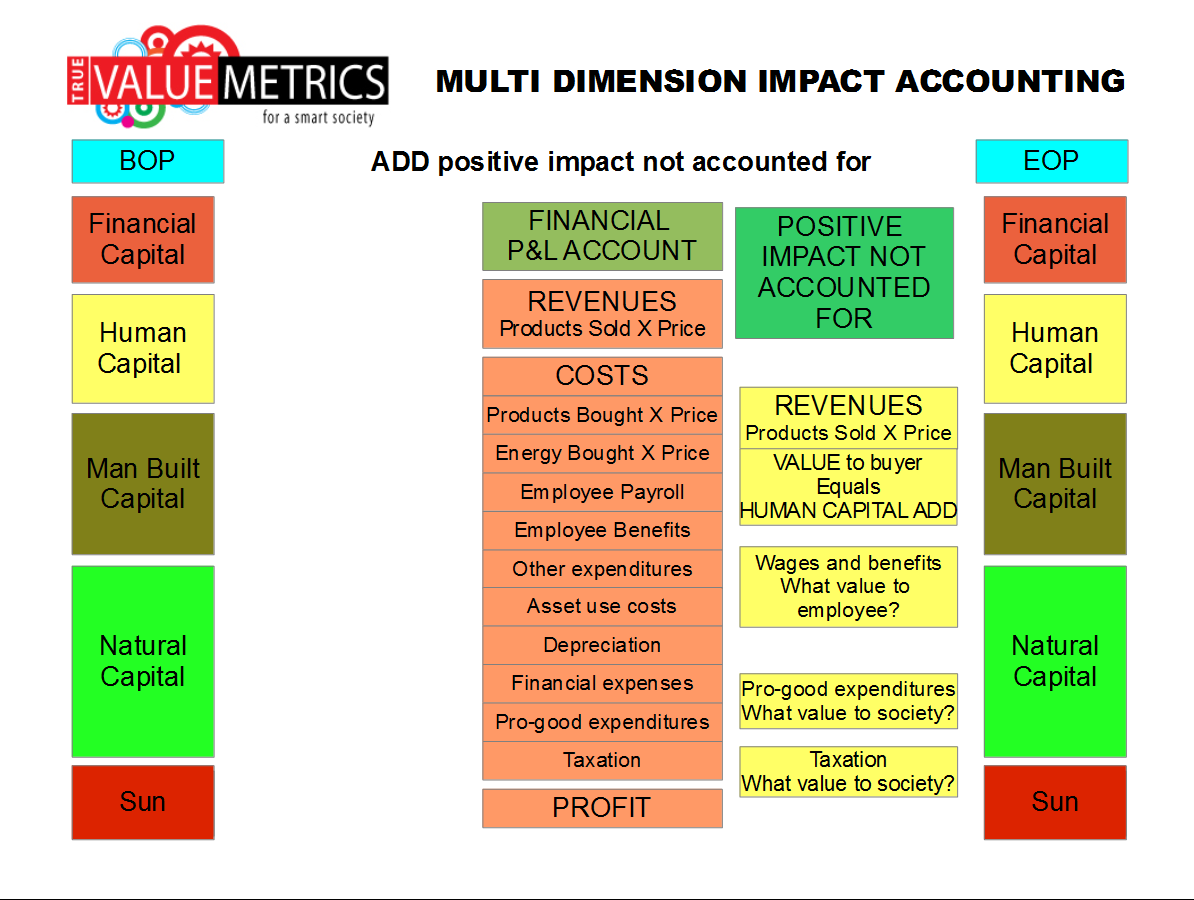

A better framework for reporting would be this …

|

|

|

|

|

|

|

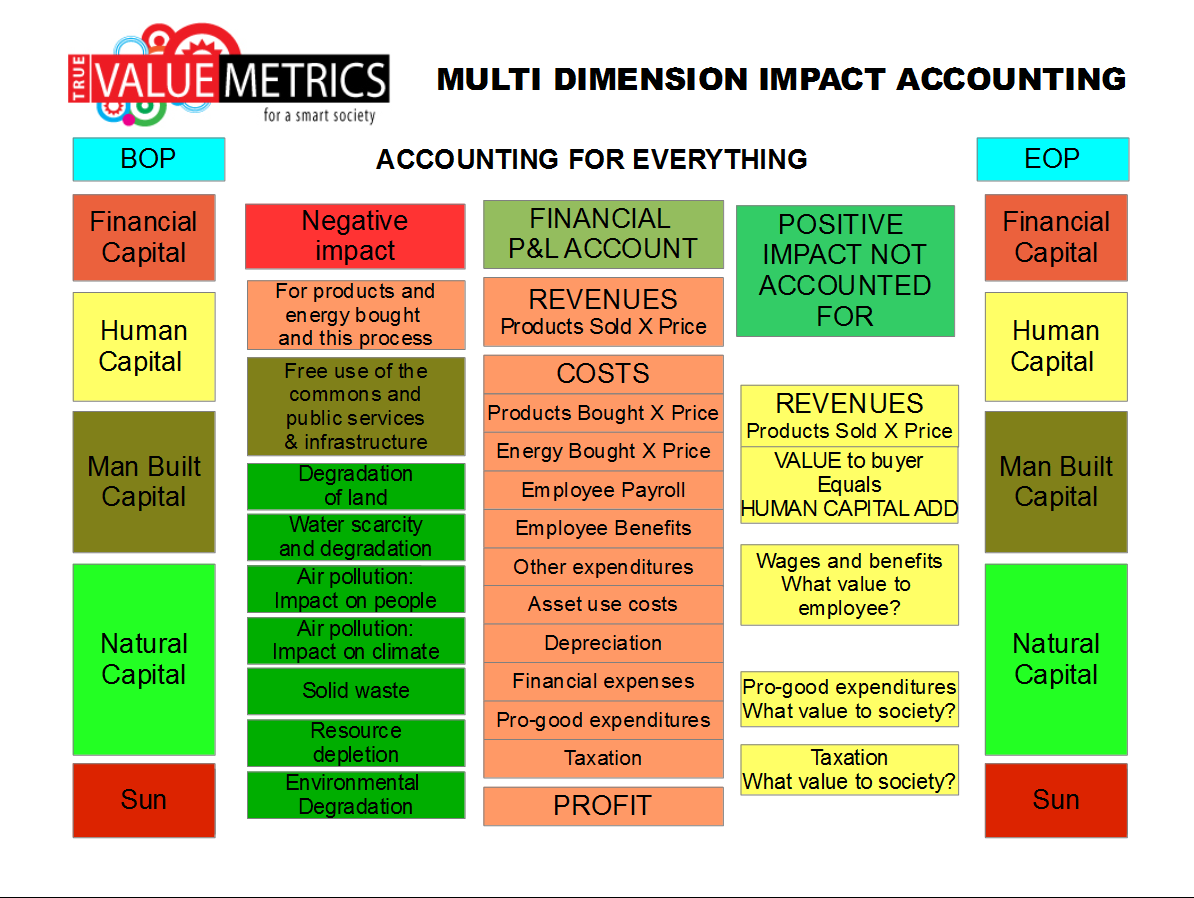

So think of all this miniaturized:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PROCESS EFFICIENCY

THE MAIN DETERMINANT OF SOCIO-ENVIRO-ECONOMIC EFFICIENCY

|

|

|

… and specifically this mean making all the PROCESSES that are used to support our QUALITY OF LIFE more efficient not only to make more PROFIT but also to have a BETTER IMPACT on SOCIETY (PEOPLE) and ENVIRONMENT (PLANET).

|

|

|

For example … OIL AND GAS ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… attention to the matter of waste water and solid matter polluting the environment;

… attention to the matter of oil pollution during production and transportation:

… and a whole lot more.

|

|

|

For example … in AGRICULTURE ...

better stewardship of WATER use;

… attention to pollution from run-off containing fertilizers, herbicides, pesticides, etc;

… more responsible use of animal medication to avoid risk of drug resistance important for human health;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

|

For example … TRANSPORTATION ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… attention to the matter of waste water and solid matter polluting the environment;

… and a whole lot more.

|

|

|

For example … OFFICE BUILDINGS ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… and a whole lot more.

|

|

|

For example … HEAVY INDUSTRY ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… attention to the matter of waste water and solid matter polluting the environment;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

|

For example … MINING ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… degradation of the land;

… attention to the matter of waste water and solid matter polluting the environment;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

|

For example … CONSTRUCTION ...

… attention to the use of ENERGY;

… attention to the matter of EMISSIONS into the atmosphere;

… attention to the matter of waste water and solid matter polluting the environment;

… the issue of worker exploitation and workplace safety;

… and a whole lot more.

|

|

|

|

CONCLUDING OBSERVATION ...

… more than anything else improving the EFFICIENCY of PROCESS will change the trajectory of global socio-enviro-economic performance;

… in the past efficiency has simply been about less COSTS and more PROFIT;

… in the future EFFICIENCY has to be about better QUALITY OF LIFE for PEOPLE with very little of no damage to the ENIRONMENT (PLANET)

INTEGRATED FINANCIAL AND IMPACT ACCOUNTING ...

… integration of financial and impact accounting will make it possible for very much better decisions to be made.

… high efficiency can be rewarded and there can be social accountability for bad practices and low efficiency.

CHIEF PERFORMANCE OFFICER

Maybe in the near future it will be possible to rename the CFO (Chief Financial Officer) to be the CPO … the Chief Performance Officer, a C-level position that integrates financial performancewith impact on society (people) and impact on the environment (planet).

|

|

|

|

|