UNITS OF ACCOUNT

ESSENTIAL FOR EFFECTIVE POLICY MAKING

CRITICAL TO MANAGE THE COMPLEX SOCIO-ENVIRO-ECONOMIC SYSTEM

|

FINANCIALIZATION ... THE PURSUIT OF FINANCIAL WEALTH

Money

|

Profit growth

|

GDP growth

|

Stock Prices

|

|

MONEY IS THE DOMINANT METRIC FOR PERFORMANCE

|

BUT MONEY HAS A HUGE VARIABILITY ... NOT A CONSTANT VALUE

Everyone is familiar with money, but may not appreciate how much it influences measurement and policy decisions. At its core, money serves two purposes:

- as a medium of exchange for the transaction; and

- as a store of value.

Money and double entry accounting is a very powerful system for accountability

When the population and the economy were relatively small, the impact on society and the environment could be ignored without much consequence.

But the 21st century is different. The population of the world is at record levels, and the degradation of the environment has become consequential, whether it is air pollution, water pollution, land fill, deforestation, ocean plastic or any number of other issues.

There is a need now for UNITS OF ACCOUNT that are relevent for ALL the impacts associated with economic transactions.

The money measure needs to be better understood. It is common to use a reference currency like the US dollar, but local currency also matters, and there may be funding currency as well. Besides the US$, other reference currencies might be the Euro, Japanese Yen or Chinese Yuan

|

|

IN THE ECONOMY, PROFIT IS THE DOMINANT METRIC

|

YES, PROFIT IS IMPORTANT, BUT NOT TO THE EXCLUSION OF EVERYTHING ELSE

The rules and regulations about corporate reporting behavior that emerged during the industrial revolution in the 19th century were fit for purpose at that time. Back then companies blatantly lied to investors and potential investors about their financial performance and prospects, and laws were enacted so that this lying was supressed. This is the origin of the independent financail audit and report of the auditors.

But over time things have changed substantially and the idea that all is well if profits are as big as possible is no longer a reasonable premise. The world is very differnt in the 2020s than it was the 1870s, about 150 years ago. The world's population is now around 8 billion people compared to around 1 billion 150 years ago and the scale of global economic activity has increased by something like a hundred times ... or is it perhaps a thousand times ... depending on how it gets measured.

The point is tha limits to growth

|

GDP GROWTH IS MAIN MEASURE OF NATIONAL PERFORMANCE

|

BUT MONEY HAS A HUGE VARIABILITY ... NOT A CONSTANT VALUE

TPB note: I studied engineering and economics at Cambridge in the 1950s and qualified as a Chartered Accountant in London in the ealry 1960s. It was widely recognised at that time that GDP was a poor indicator of economic performance and should be ipgraded to something that was a lot better. This idea was promulgated by Keynes and Kuznets, both of whom had had a role in the development and use of the GDP metric when nothing better existed. But why is it that it continues to be used more than a helf century after better metrics became available. My conclusion is that many of those with power and influence understand that the GDP metric serves their own interest and makes meaningful economic analysis impossible. If GDP was double entry accouning, it is like adding up all the debits and all the credits in a single column and reporting that as profit ... a stupid idea, but that is pretty much what happens with the GDP metric.

|

|

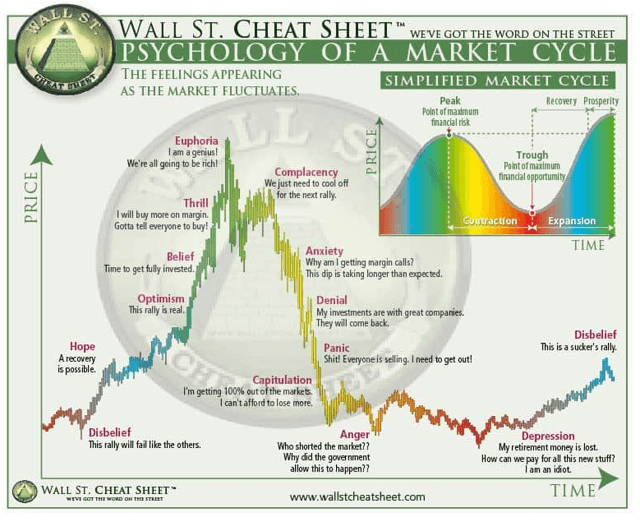

STOCK PRICES MORE IMPORTANT THAN QUALITY OF LIFE

|

IS THE STOCK MARKET REALLY A 'MARKET'?

There is no question that the stock market is an important component of the esisting economic system, but whether or not it serves the interest of society as a whole is less clear.

There was a time before high speed computers when the stock market was run at a more leisurely pace and human beings were able to think about what was happening in the 'market'. There was an appreciation that there was a role for 'speculation' as something that actually stabilized the market.

But the 'market' of the 2020s is very different from the market of the 1960s yet rather few people have much appreciation of what these changes are, and how the market is being gamed by its functionaries in ways that make a mockery of what the market is meant to be all about.

TPB note: I get annoyed every day when the evening news on TV includes a comment on the closing price for major indices on the New York Stock Exchange (NYSE), but rarely says anything about what is causing the price changes. I have heard nothing about why it is that many of the stocks on the NYSE have been at resord highs when the US and the world are facing some of the worst economic headwinds in a very long time ... why is this?

|

|